NEWS

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +5.14% in November, outperforming the ASX 200 Total Return benchmark by +1.35%. Since inception in June 2017, the fund has returned +19.91% per annum, an outperformance of +10.38% relative to...

Read more...

Proprietary Data - Strategic AI Advantage

Proprietary data sets provide businesses with competitive advantages due to their uniqueness, quality and relevance. They are often more specific, accurate, and tailored to a company's particular needs or industry, providing a rich data...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +6.43% in November, outperforming the ASX 200 Total Return benchmark by +2.64%. Since inception in November 2017, the fund has returned +20.04% per annum, an outperformance of +10.66% relative...

Read more...

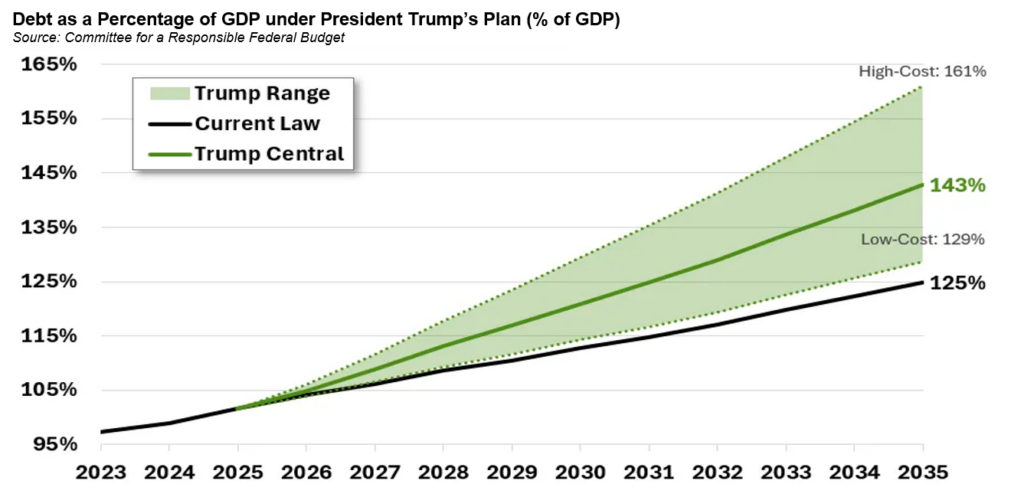

Investment Perspectives: Why a Trump presidency could be deflationary

Last month, US voters re-elected Donald Trump for a second term as US president. As a result, market enthusiasm and expectations are high. An immediate rally in US equities (and a selloff in bonds) pointed to renewed optimism for both...

Read more...

Hedge Clippings | 13 December 2024

As soon as Governor Michele Bullock had given the first indications of a softening of the RBA Board's stance on inflation, and with it the possibility of a rate cut, markets responded by factoring in 2 cuts prior to the election. Of course...

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +8.1% over the past 12 months. Since inception in March 2016, the fund has returned +9.03% per annum, a difference of -0.98% relative to the S&P Global Infrastructure TR (AUD) benchmark...

Read more...

Performance Report: Argonaut Natural Resources Fund

The Argonaut Natural Resources Fund returned -2.7% in November, outperforming the S&P/ASX 300 Resources TR benchmark by +0.71%. Since inception in January 2020, the fund has returned +25.76% per annum, an outperformance of +18.14% relative...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +4.49% in November, outperforming the ASX 200 Total Return benchmark by +0.7%. Since inception in November 2009, the fund has returned +10.03% per annum, an outperformance of +1.53%...

Read more...

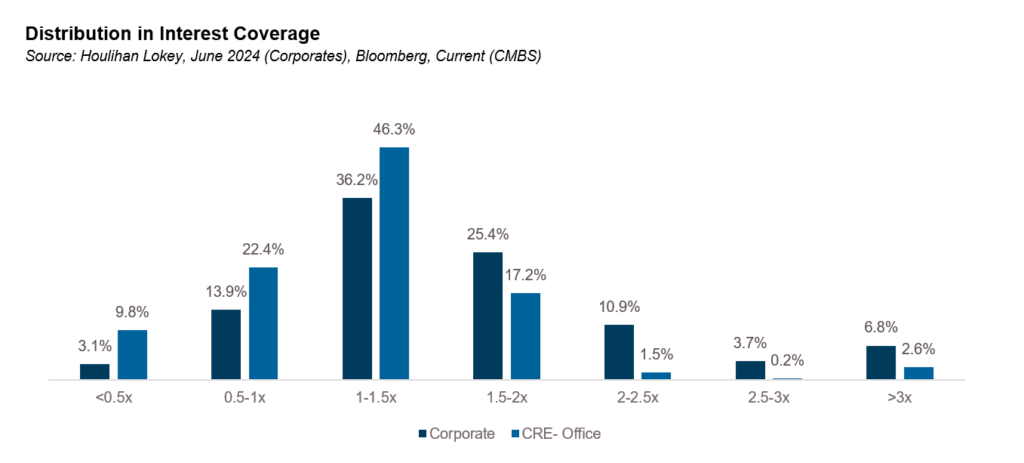

Risks & Issues in 2025 - Part 2

Part 2 of Risks & Issues in 2025 considers the implications of the global backdrop discussed in Part 1 for Australia - as well as some home-grown influences.

Read more...

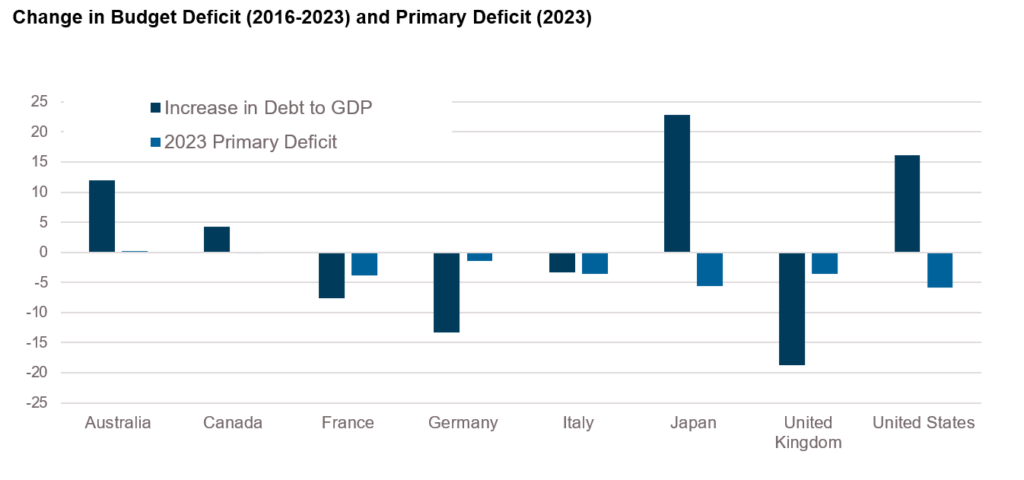

Trump trade 2.0 - Who is going to buy all this stuff?

In 2016 the election of Donald Trump as president of the United States caused an initial panic in markets with S&P500 futures plunging over 5% as his shock win became more likely. Wall Street had favoured Clinton, fearing Trump's positions...

Read more...