NEWS

6 Jul 2023 - Power-hungry AI a watch-out for equities investors

|

Power-hungry AI a watch-out for equities investors Pendal June 2023 |

|

Big US tech stocks are soaring on a wave of new, advanced AI applications. But similar to Bitcoin's early days, excited AI investors may be overlooking the technology's extremely high power costs and potential associated sustainability issues, argues Pendal Aussie equities analyst Elise McKay. While the remarkable progress of AI promises to revolutionise industries, the sheer cost of the electricity needed to train and run the systems puts a question mark over the long-term prospects of adoption. "There's three key components of power usage required for running a generative AI model," says McKay. "First of all, there's the power needed to simply build the equipment that it runs on. "Then there is the enormous power required to train the model. "And then every time you ask it a question it requires new computations — and that means more power." Even before generative AI became widely available, demand for data was expected to increase at a compound annual growth rate of 40 per cent per year. The data centre industry is already estimated to account for about 1 per cent of global energy demand, says McKay. "Just because it's on your phone doesn't mean it's not in a data centre somewhere — and data centres need electricity. Any new technology just increases demand for power." McKay uses the example of bitcoin mining, which rapidly increased its share of global energy consumption from next to nothing to an estimated 0.5 per cent in 2021. "Emerging technologies like bitcoin mining can see very rapid adoption and dramatic increases in demand for power," says McKay. "We are now seeing the broad take up of generative AI, which is significantly more power hungry than existing technologies." A study by Stanford found that training the popular GPT-3 generative AI system contributed almost 10 times the emissions that the average car consumes in its lifetime, says McKay. Estimates are the newer GPT-4 model was eight times more power intensive again, she says. "And you don't just do this once, you do it regularly." OpenAI — the company behind ChatGPT — says it continuously improves its AI model by "training on the conversations people have with it". "And each model can only do one search at a time," says McKay. "So, if 100,000 people search for something at the exact same time you need 100,000 copies of the model otherwise queries will be queued. "Estimates are that every time you query ChatGPT, it is 300 times more expensive than a Google search." High power usage has also raised question marks over the carbon footprint of the technology industry, with many providers shifting to renewable energy to minimise their impact on the environment. "The high cost of providing AI will hinder its adoption," says McKay. "It may mean that only companies willing to pay a high price will be able to use it. There's a good use case for companies willing to pay for it because it improves productivity, but will we see broad adoption for low-paying use cases?" Author: Elise McKay, Investment Analyst |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

5 Jul 2023 - 10k Words | June Edition

|

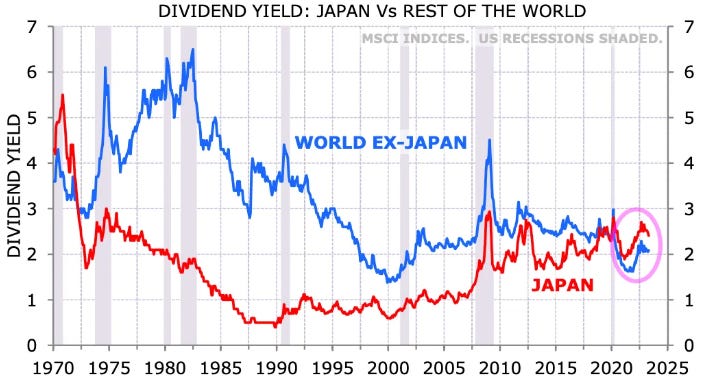

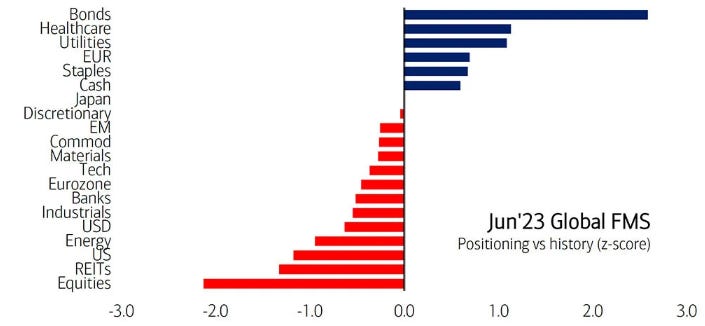

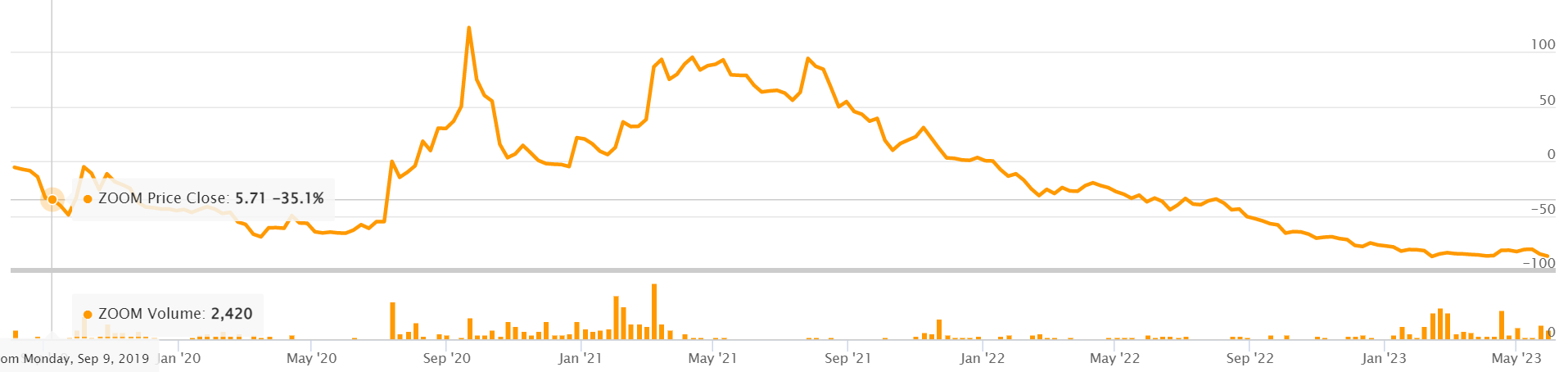

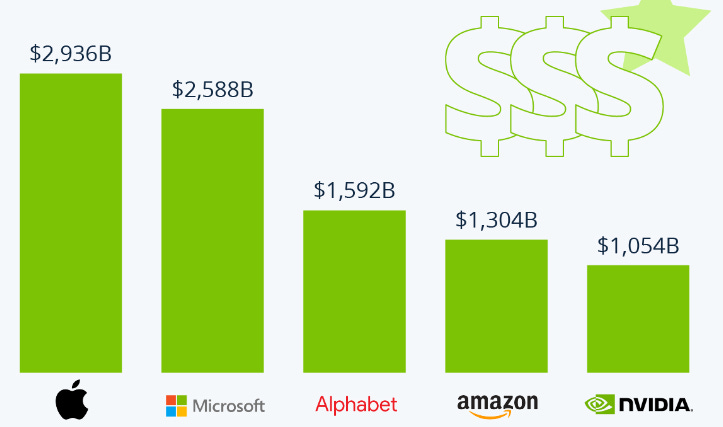

10k Words Equitable Investors May 2023 Changes in the cost of capital remain front and centre with Japan's dividend yield surpassing the rest of the world's for the first time in 50 years and asset class yields converging as fund managers express bullishnes on bonds, with 30+ countries facing inverted yield curves and the futures market still pricing a decline in the Fed Funds rate. It is amazing how even having the ticker "AI" has been enough to attract buyers. Amidst such sentiment, Nvidia has joined the trillion dollar market cap club - being in the sector that has diverged from bonds of late. Such mega caps are living in a different world from small businesses facing into tighter lending. We look at the S&P 500's trends relative to interest rates and "QE" and how large cap growth has been above other market segments over the past decade. There's still not much joy in IPO markets - especially for those who didn't sell quickly. Finally, we take a look at the decline of cash in the Australian economy and the resurgence of commercial aircraft orders. Japanese dividend yield exceeds the rest of the world for first time in 50 years

Source: Minack Advisors, Asian Century Stocks Compression of yields across assets

Source: Financial Times Fund Managers' bullish bonds, negative equities, relative to historical levels (June 2023 survey)

Source: Bank of America, [email protected] 33 countries have an inverted yield curves

Source: worldgovernmentbonds.com Market expectations for Fed Funds Rate (as per futures)

Source: @CharlieBilello Recent surge in price of C3.ai (Ticker "AI")

Source: TIKR Stock code "ZOOM" took off when Zoom Video Communications (ZM) surged in 2020

Source: TIKR Nvidia joins "Trillion Dollar" Market Cap Club

Source: Statista Divergence between tech valuations & bond yields

Source: Bloomberg, Koyfin Loan availability compared to three months ago

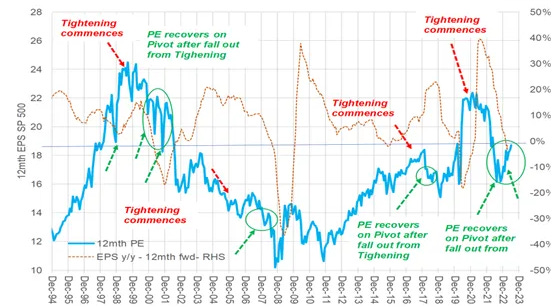

Source: NFIB Small Business Economic Trends May 2023 Fed tightening, EPS growth & PE multiple expansion/contraction

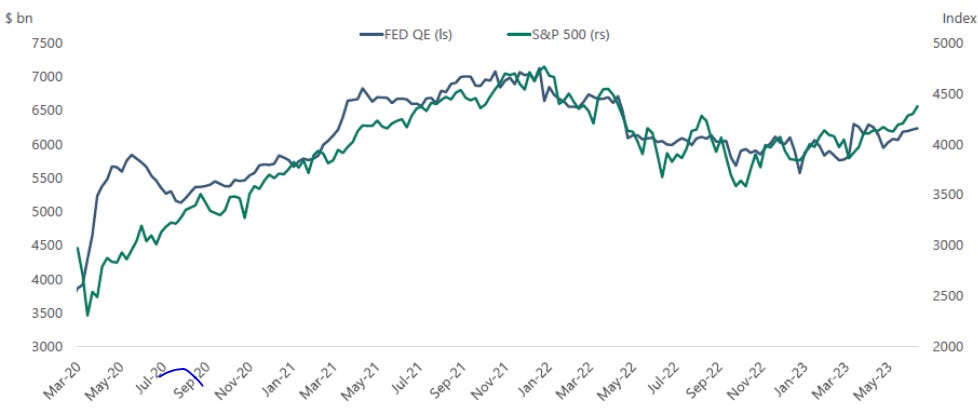

Source: @EquitOrr S&P 500 performance and Federal Reserve net Quantitative Easing (QE)

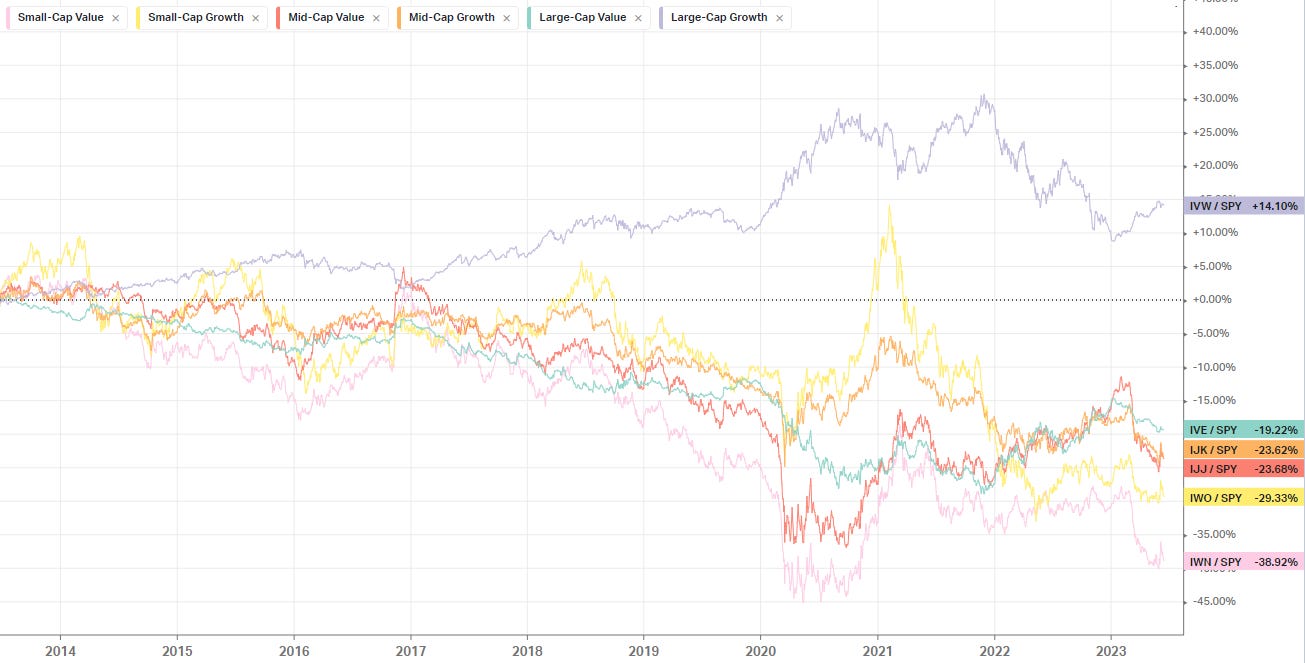

Source: Bloomberg US equities - growth v value over the past 10 years

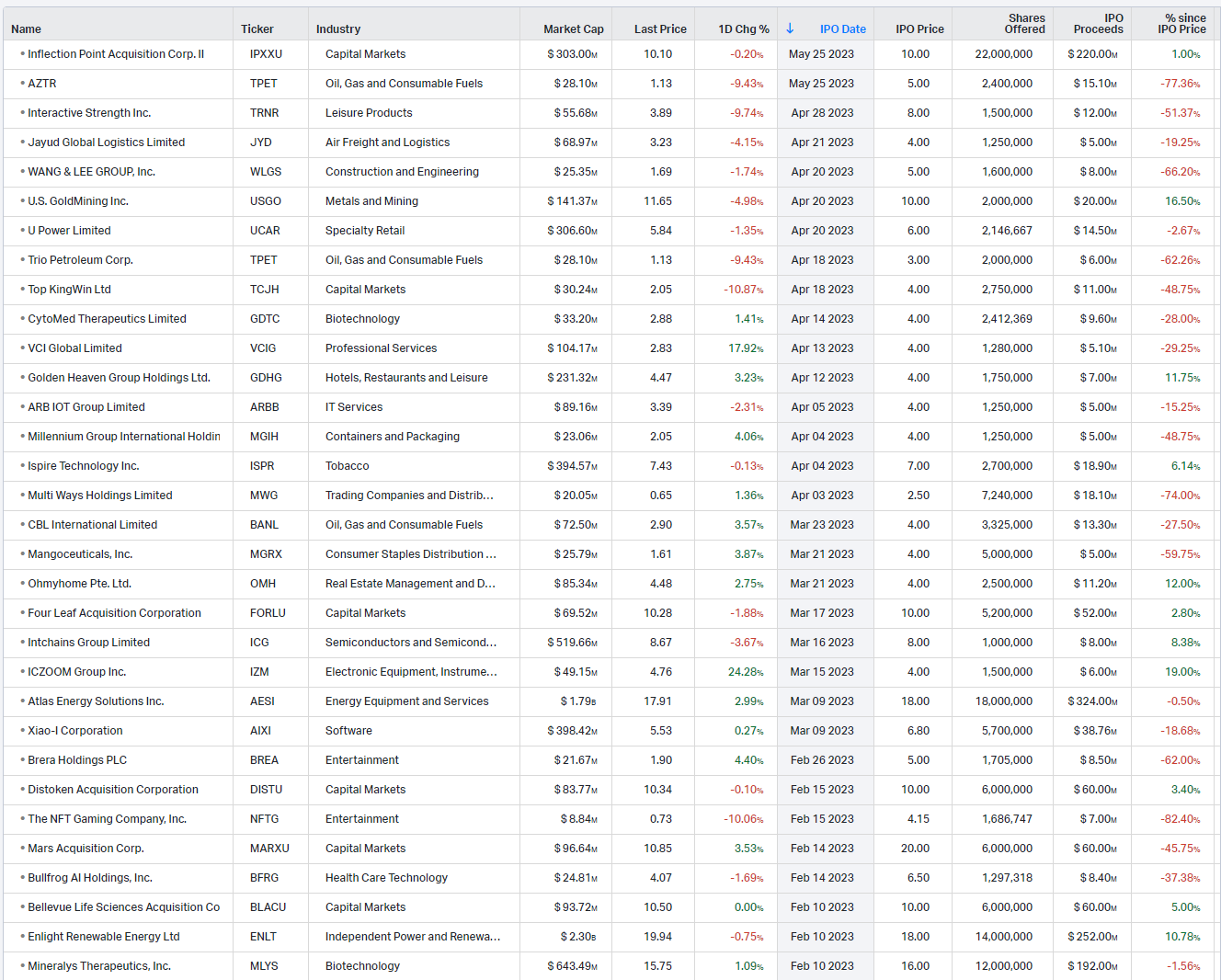

Source: Equitable Investors, Koyfin Recent US IPOs

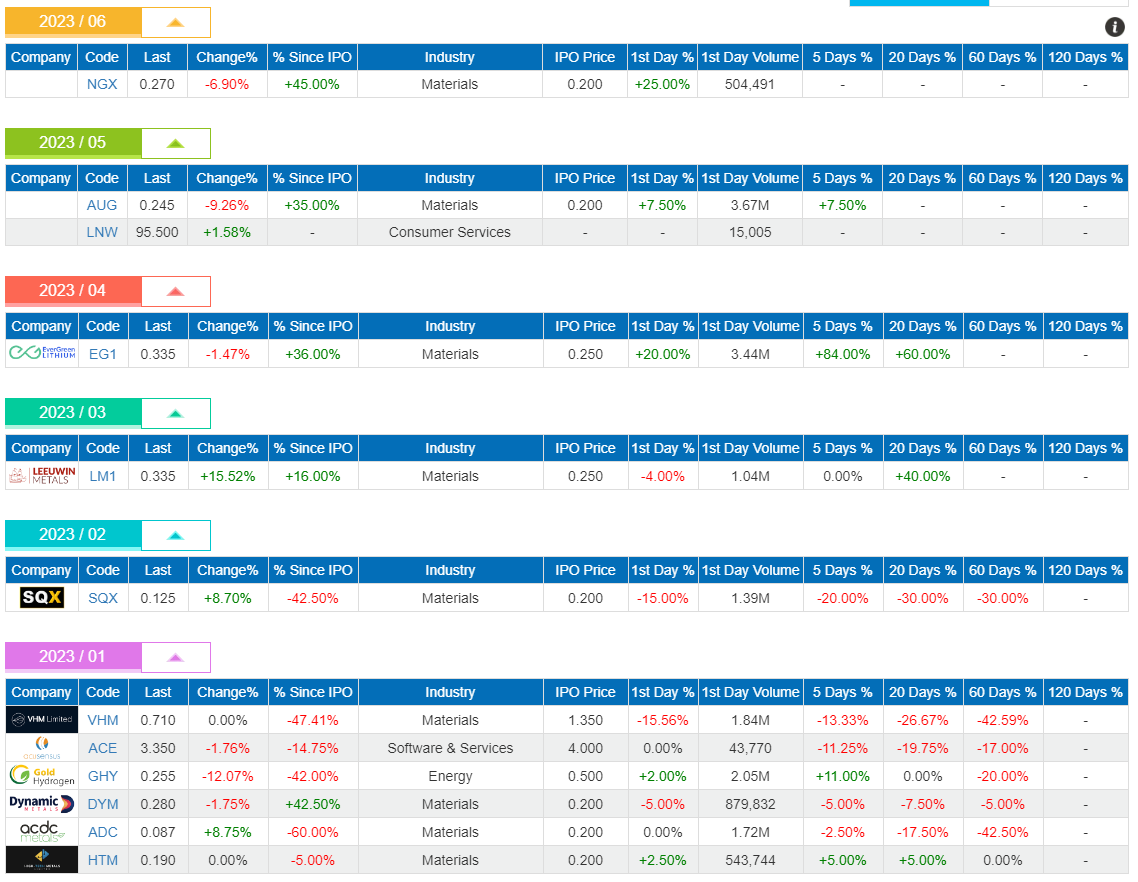

Source: Koyfin ASX IPOs in CY2023

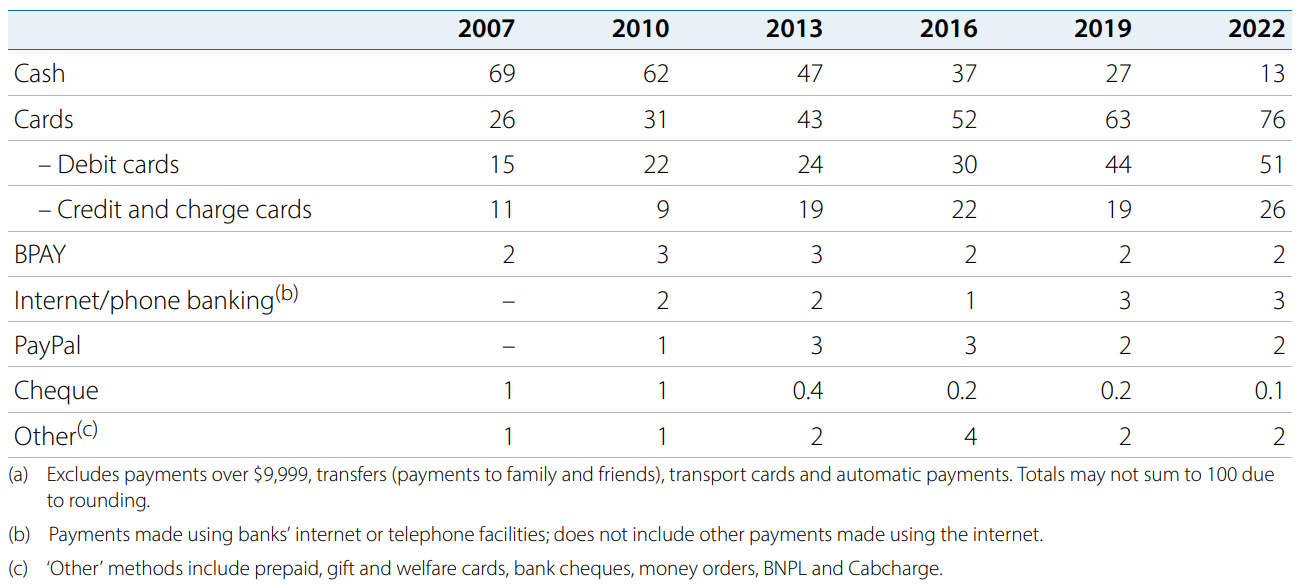

Source: 61Financial Sharp decline of cash's share of Australian payments

Source: RBA Net orders for commercial aircraft

Source: The Economist June Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

4 Jul 2023 - Global Matters: The importance of emerging markets to the infrastructure opportunity

3 Jul 2023 - Webinar Recording 27 June 2023 | Resource Funds - Analysing the Opportunities and Risks

|

Webinar Recording | Resource Funds - Analysing the Opportunities and Risks FundMonitors.com 27 June 2023 |

|

Resource funds can offer a unique avenue for capitalising on the growing demand for natural resources and the global shift towards sustainable energy and materials. In this webinar, we looked at the strategies and approaches employed by three successful resource fund managers and learn how they navigate the opportunities and risks associated with this asset class. Watch the recording of our manager round table webinar, where we were joined by Dan Porter from Pure Asset Management, David Franklyn from Argonaut Funds Management, and Matthew Langsford from Terra Capital. They shared their views on this interesting and diverse market sector. |

30 Jun 2023 - Hedge Clippings | 30 June 2023

|

|

|

|

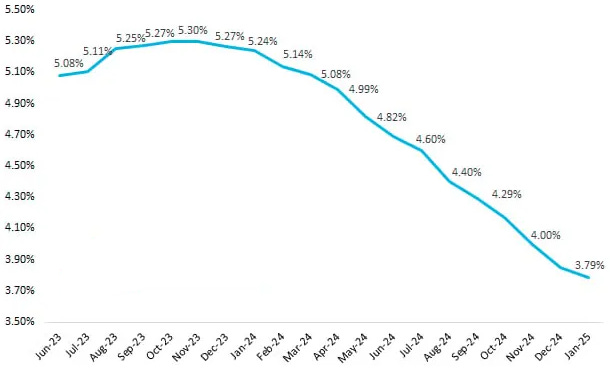

Hedge Clippings | 30 June 2023 CPI and Retail Sales Numbers throw doubt on Tuesday's RBA decision May's CPI and Retail Sales numbers released by the ABS this week gave economists reason to reconsider where inflation really sits. However, looking through headlines to the details, the question remains: Will the numbers be sufficient to convince the RBA to hit the "pause" button next Tuesday? Even if they do hold off, it's likely to only be temporary, and in the longer term, there's little chance there'll be any meaningful relief for stressed mortgage holders for at least another year, and possibly two. Taking a look at the Monthly CPI results first, which seasonally adjusted at 5.6% for the 12 months to May, and down from 6.8% in April, were, on the face of it, a cause for optimism. Stripping out volatile items (fruit and vegetables, fuel, holiday travel, and accommodation) the number was less encouraging at 6.4%, but still a marginal improvement on April's rise of 6.5%. Annual Trimmed Mean inflation (i.e. stripping out the extremes) was 6.1%, also down from April's figure of 6.7%. The first issue is fuel, which was the only negative number, falling 8% for the month, but as anyone who owns a motor vehicle (or at least pays at the bowser) would know, IS volatile, having risen 9.5% in the 12 months to April, and fallen 8.2% in the 12 months to March. Of the items which significantly offset fuel's negative number, the largest increases were in every day (and therefore largely unavoidable) items, such as Bread and Cereals (+12.8%), Dairy (+15%), Food Products (11.5%), and Electricity (+14.1%), and all of which had been elevated at or around those levels for April and March. Leaving aside the question of whether suppliers and retailers of these categories are taking advantage because A) they're staples and therefore largely unavoidable purchases, or B) they can lay the blame for price rise on their suppliers or the overall consumer expectation of inflation, are the above numbers in part responsible (in conjunction with mortgage and housing) for consumer confidence and financial concerns as a whole? Hedge Clippings rather selfishly notes that Alcohol is running below the inflationary average at 5.0%, down somewhat from the April and March numbers, but let's not go there. Against this, Retail turnover (as reported by the ABS) for May rose 0.7%, following a flat result in April, and a rise of 0.4% in March, supported by a rise in spending on food and eating out, combined with a boost in spending on discretionary goods, as consumers took advantage of larger than usual promotional activity and sales in May, along with Mother's Day. As the ABS noted, "Food retailing has recorded a monthly rise for 16 or the last 18 months," and continued by saying that "most of the growth in food-related spending this year has been driven by rising prices." Back to Tuesday's meeting and decision, the RBA will obviously be looking behind the headline numbers that the average consumer recalls, particularly the ongoing strength in the employment statistics, and the National Wage Case Decision increasing the minimum wage by 5.75% handed down in June, but yet to impact the numbers. As we noted at the outset, will the seasonally adjusted result of 5.6%, down from 6.8% be enough for the pause button to be pressed? Even if it is, we would expect it is far too early to budget for any reduction. As much as the RBA is expecting inflation to improve in 2024/2025, there's no way they will risk letting persist at current levels (or worse) by acting too soon. That's assuming they can get the inflation genie back in the bottle by then, without triggering a recession. While everyone is aware of inflation, and few can avoid it, it is evident that it is only impacting the shopping habits of certain (although increasing) consumer demographics. Unfortunately, interest rates are the bluntest of instruments (and the only one) in the RBA's tool kit. This week we held the last of our regular Webinars, with our COO Damen Purcell interviewing three guest fund managers, namely Matthew Langsford from Terra Capital, Dan Porter, from Pure Asset Management, and David Franklyn, from Argonaut Resources who discussed their approach to the opportunities and risks in the Resources Sector. Click here to view a recording (45 minutes) of the Webinar, and here to view each of the Fund's Profiles on www.fundmonitors.com. |

|

|

News & Insights Risk-adjusting small-cap upside | PURE Asset Management Investment Perspectives: Do developers offer the best exposure to a recovering residential property | Quay Global Investors May 2023 Performance News Bennelong Concentrated Australian Equities Fund Skerryvore Global Emerging Markets All-Cap Equity Fund Bennelong Twenty20 Australian Equities Fund Insync Global Capital Aware Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

30 Jun 2023 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

30 Jun 2023 - AI Revolution

|

AI Revolution Insync Fund Managers June 2023

Adobe has established itself as the indisputable standard in creative software. Commanding both recognition and reliance by professionals in graphic design, photography, videography, web design, and publishing. It is well positioned to benefit from AI. Adobe has been leveraging its AI engine - Adobe Sensei, to power new AI features across its various product lines. Many of these new AI features, especially for Creative Cloud products, represent a potential paradigm shift in the day-to-day workflow and content creation of their users. The realm of Generative AI has Adobe Firefly competing with current industry giants (DALL-E and Mid-Journey). Adobe however gains an edge utilizing licensed and out-of-copyright content, making it highly appealing to corporate markets. Large companies, constrained in content creation, can now profit from Generative AI, while trusting Adobe's reputation for reliability.

As the AI revolution unfolds Adobe stands as the unrivalled leader in content creation. It is already transforming the creative landscape and propelling content creators into limitless realms of possibility. Importantly it's an extremely profitable business with compounding sustainable earnings. Precisely the kind of business Insync loves to own. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

29 Jun 2023 - Performance Report: Digital Asset Fund (Digital Opportunities Class)

[Current Manager Report if available]

29 Jun 2023 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]