NEWS

28 Jul 2023 - ChatCB - Artificial Intelligence and Convertible Bonds

|

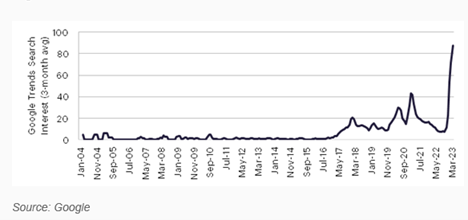

ChatCB - Artificial Intelligence and Convertible Bonds Redwheel (Channel Capital) July 2023 The concept of Artificial Intelligence (AI) has been around for a while, but is it finally ready to be the Next Big Thing? Over the last 12 months, the release of a large language model to the public (ChatGPT) and a material uplift in Q2 2023 guidance from chipmaker Nvidia based on demand from AI applications has spurred many stock prices higher. In the case of a few companies, dramatically so. The chart below shows the uptick in Google searches for the term "Artificial Intelligence" - clearly, there are many questions about the impact that AI might have on the economy and for workers, both good and bad. Could the rise of AI justify higher stock prices now, and could there be more to come - or is recent optimism unfounded?

Source: Google, as at March 31st 2023. The information shown above is for illustrative purposes. We will not claim to have all the answers to these questions, but we will explore the background of AI, some of its use cases, and how we think the convertible bond market and individual issuers have and will play a role in AI developments. What is AI?AI is a branch of computer science that uses digitised inputs (text, images, numbers) to generate outputs in a way that can simulate human intelligence, using relationships between data to program algorithms for decision-making or answers. For many, AI became familiar from the creation of structured solutions to a known application - for example, programming computers to play chess, but in the past, these efforts required a high degree of human involvement for fine-tuning. Historical advances in AI are due largely to the exponential increase in computing power with miniaturisation of chips, driven by Moore's Law and the parallel process capabilities of GPUs*. Along with gains in storage and software programming, faster computational speeds allow researchers to run statistical models on an enormous amount of data collected over the internet, including new data sets. In turn, AI programmers can now model tasks such as image recognition, natural language processing, and computer vision. More computing power also allows algorithms to automatically incorporate new data - a process referred to as 'machine learning' - for efficiency gains. The launch of Chat GPT, a natural language processing tool developed by OpenAI, which allows users to have human-like conversations, has captured worldwide imagination and the fastest ever consumer adoption, reaching 1 million users in only 5 days (source: OpenAI). ChatGPT does more than lift sections of text from a source, it creates new sentences as a response to a user's input question. While ChatGPT and other large language models are in their early stages, replication of language-based outputs using AI could have a significant effect on economic growth, especially if they can broaden task automation or enhance search capabilities. Including other use cases for AI - such as autonomous vehicles and facial or image recognition - this field could create a profound change in business models, potentially creating new winners and categories, while disrupting some existing models. For investors, being able to successfully navigate through this environment and picking the winners won't be an easy task - just ask those investing in internet stocks in the late 1990s. Most had successfully predicted the huge impact the internet would have in the future, but many companies that were market darlings and were seen as winners ultimately failed to live up to the early promise. Investing in AI - using convertiblesIn our analysis, we currently split AI beneficiaries in three broad categories. The first group includes companies directly making hardware or software ('Building Blocks') used for AI development. The second group are those companies using AI to enable change in an industry or for their customers ('Transformative Potential'). The third group consists of companies using AI to enhance customer experience and interactions ('Personalised Product Offerings'). The analysis is by no means exhaustive, but we see it as a good starting point for investors to look at the opportunity set. Our view included a look at some of the largest ETFs focused on AI and robotics, as well as reviews of individual companies and sectors. We have also included a glossary of some of the key terms needed to understand the businesses of these companies. Building Blocks

Transformative Potential

Personalised Product Offerings

Source: Redwheel, as at 31st May. No investment strategy or risk management technique can guarantee returns or eliminate risks. Of course, there is no reward without risk, and stock prices today may not reflect the reality of tomorrow. We think that convertible bonds can help by allowing for upside participation in the theme but with downside protection from volatility and uncertainty. The asset class has long been favoured by technology companies as the vehicle of choice to raise capital to make productive investments or re-investments. We also see that demands for investment in AI development can be well-suited for financing with a convertible bond, given a multi-year payoff period and the possibility of high future growth and cash flow from an investment today. Convertible bonds give these issuers flexibility with a financing tool that can be converted into equity, but at a premium to its stock price at issuance. Convertible investors accept lower coupons than if the bond were a straight corporate bond because they hold a valuable longer-term option to convert; in turn, these lower coupons provide flexibility to the issuer. In case the company's stock price does not rise during the life of the convertible bond, convertible investors still consider the credit of the issuer and its ability to repay or refinance its debt. Where these two groups meet in the middle is that convertible investors want issuers to reinvest profitably over the life of the convertible and drive value for their share price, rather than simply to repay this debt while earning a coupon. For each of the three categories, we present a review of one specific convertible bond issuer that we see as being a good representative of the potential impact of AI. We also note other convertible bond issuers within each of the categories. Building BlocksHynix is a DRAM* manufacturer, which along with peers Samsung and Micron, operates in an oligopolistic industry consisting of these three main suppliers, whom have significant scale benefits compared with smaller operators. Hynix should be a key beneficiary from AI because Hyperscalers* require DRAM; the company is also a key supplier of high bandwidth memory to Nvidia. DRAM is at the heart of AI servers, and we see the AI boom driving a large multi-year demand cycle for memory. Other notable issuers include: Lenovo (computers and peripheral devices), Microchip (microcontrollers and integrated circuits), STM Micro (semiconductors), SOITEC (semiconductors), Lumentum (opticals for semiconductor manufacturing). Transformative PotentialMicrosoft - the firm needs little introduction: under CEO Satya Nadella, the company has successfully transformed itself into a leader in AI across various parallel uses. Three of its largest segments stand to benefit from emergence of AI. Azure, Microsoft's data centre product, is playing a fundamental role as a building block with AI, as the percentage of cloud spend is expected to pick up meaningfully in the next three years. The company has started integrating AI into its productivity suite such as Office 365, allowing Microsoft to add a premium tier to its current offering. Finally, Microsoft's 50% stake in OpenAI offers transformative potential in the search business. Other notable issuers include: SaaS vendors, Kingsoft (AI in products), Tesla (Electric Vehicles and autonomous driving), and Ford (Electric Vehicles and autonomous driving). Personalised Product OfferingsAirbnb - one of the most popular platforms for offering and booking homestays worldwide.[1] In a recent interview, company founder and CEO Brian Chesky laid out his vision of AI integration becoming central to how the company's app works. The company envisions the app becoming almost like the ultimate host, the ultimate concierge. This means leveraging the power of AI to offer a personalised experience for its customers, driving recommendations based on their preferences, choices, and data. Customer services is another area where the company expects AI to drive large efficiency gains by augmenting traditional customer services with AI. For example, customer service agents will be assisted by AI to gain quick access to the relevant sections of one of the 72 user policies: each 100 pages long, helping them resolve queries faster and cutting down training times. Other notable issuers include: Booking.com, Expedia, Uber, Block, Etsy, Zillow. ConclusionWe believe that AI is here to stay and many of the companies at the forefront have used the convertibles market for financing, both in the past and now. Because there is no return without risk, convertibles can provide exposure to AI and relevant technologies, with structures which allow for upside capture but with protection on the downside from volatility and uncertainty. |

|

Funds operated by this manager: CC Redwheel Global Emerging Markets Fund, CC Redwheel China Equity Fund Sources: *See glossary for definitions [1] Skift, 3rd May 2023, https://skift.com/2023/05/03/interview-airbnb-ceo-on-how-its-service-will-radically-change-with-ai-by-next-year/ GlossaryCPU (Central Processing Unit) The key processor in a computer that runs most functions, such as logic and arithmetic. GPU (Graphics Processing Unit) Enables graphics, visual effects, and video in a computer to be run in parallel with other functions. Hyperscaler An extremely large-scale cloud-based data and service provider. Foundry Fabricates semiconductors using silicon wafers and integrated circuits. Some foundries are owned by semiconductor companies, others manufacture semiconductors to customised designs by semiconductor designers that are using a "fabless" operating model. SaaS (Software as a Service) Typically, a subscription-based business model where users connect to and use cloud-based applications via the Internet, often accessed through web browsers. DRAM (Dynamic Random Access Memory) Dynamic RAM is one of the most typical types of semiconductor memory. DRAM generally uses a capacitator to store electrical energy and a transistor to regulate voltage to store data in a memory cell. Using DRAM involves a trade-off between the low cost of units versus the need to recharge the capacitators, which also involves re-writing data to the memory cells ('memory refresh'). More DRAM available to a computer allows it to run a greater number of computations and processes; advances in power management help to reduce the electricity requires for operation and the memory refresh process. Key information: No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor's investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only. |

27 Jul 2023 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

27 Jul 2023 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

27 Jul 2023 - Forever Chemicals - PFAS

|

Forever Chemicals - PFAS PURE Asset Management July 2023 The jungle drums are beating louder as the calls for increased regulation of Per- and polyfluoroalkyl substances (PFAS) become clamorous, and class action lawyers gear-up for their next big opportunity. This comes more than two decades after internal documents revealed that DuPont had known of a link between PFAS and cancer in 1997, and was aware of the potential health risks as far back as the 1960s. Corporate settlements, regulatory changes and journalist investigations are proliferating, broadening public awareness of the risks associated with PFAS. Suggestions that these chemicals are the 'asbestos' of the current generation, are a clarion call for strengthened regulation, and the Environmental Protection Agency (EPA) in the US has responded aggressively. What are PFAS?PFAS are man-made chemicals that have been used extensively in industry and household products since the 1940's. Non-stick cookware, food packaging, cosmetics, water repellents and fire retardants illustrate the proliferation of these forever chemicals, which don't break down and can accumulate over time. Exposure is difficult to avoid, with ingestion the primary transmission mechanism. What are the risks of PFAS?While scientists continue to learn about the human impacts of PFAS, recent studies have suggested that exposures may lead to the following health effects:

What is being done about it? In short, plenty. Over the past five years, corporate America has been under attack for its historical negligent use of these chemicals. This ranges from products sold, to how waste has been disposed, and the downstream consequences presented to humans as a result. While the pun is ironic, the 'downstream' issue facing society today is the prevalence of PFAS in municipal drinking water. Corporate litigation has been building momentum, with Dupont the first to settle a class action in 2015, made infamous by the Dark Water movie - a must watch for anyone interested in the subject. Together with two other defendants, Dupont also recently settled another US$1.2bn claim with water utilities, and in recent weeks, US conglomerate 3M agreed to a US$10.3bn structured payout to water utilities. Analysts at Morningstar, a research firm, estimate that 3M's total liabilities could grow to as much as $30bn as state, foreign and personal injury claims are factored in. Source: https://news.bloomberglaw.com/pfas-project/companies-face-billions-in-damages-as-pfas-lawsuits-flood-courts The scale of the 3M settlement is likely to set a dangerous precedent for this US$28bn revenue industry, with the company just one of 12 major participants, including Merck, Bayer, BASF and Honeywell. Like Dupont, 3M appears to have known and covered up the risks for decades. Litigation cases have heightened awareness, and regulatory bodies are rapidly responding. Given its importance to society, initial focus has centred on municipal drinking water. Many US states, predominantly those on the east and west coasts, have independently moved to regulate acceptable levels of PFAS in drinking water. While a step in the right direction, the Environmental Protection Agency (EPA), with a Federal mandate, has now become engaged, embarking on a radical change to regulations. The EPA has proposed a revised US national drinking water standard. With formal implementation expected in late 2023, these stringent measures target six common PFAS, with tolerable limits all but eliminating any trace in drinking water. "The previous guideline, set in 2016, set a limit of 70 parts per trillion (ppt) for both PFOS and PFOA in drinking water. The new advisories decrease that by more than a thousandfold. The new limit for PFOS is 0.02 ppt; for PFOA, it's 0.004 ppt. Essentially, the EPA wants the limits to be as close as possible to zero as a growing body of research has shown how toxic these compounds are." Source: https://www.hsph.harvard.edu/news/features/stricter-federal-guidelines-on-forever-chemicals-in-drinking-water-pose-challenges/ Coupled with the availability of US$2bn in Bipartisan Infrastructure Law Funding, all municipal water utilities in the USA must now adopt measures which ensure compliance. The proposed rules require public water systems to:

In meeting the levels proposed, the EPA has previously provided guidance on how best to achieve compliance. This has focussed on three measures, namely:

The most commonly used method, and primary recommendation of the EPA as a solution to combat liquid-phase chemical removal, is through filtering using Granular Activated Carbon (GAC). Investment opportunity Unlike asbestos, where profits were derived from shorting companies selling asbestos products, activated carbon appears to offer a profitable long thesis. Pricing has moved aggressively in recent periods, with industry leader Calgon Carbon announcing price rises of 15-40% across its product range in December 2022. At PURE, we are investing in this thematic via an exposure to ASX listed company, Carbonxt (CG1.ASX). CG1 has historically focussed on air-phase solutions through powdered and pelletised products. A recent 50/50 joint venture agreement with Kentucky Carbon Processing (KCP) is facilitating the Company's entry into the liquid-phase market. Carbonxt's aim is to meet demand from water utilities via the production of GAC, or a superior pelletised product. The Company can produce GAC but also has aspirations to introduce a specialised pellet product that achieves the same results with less pressure drop. In simple terms, this decreases electricity consumption for water utilities, lowering their cost of production. Not only is market demand underpinned by regulatory change, but new supply is both long-dated and costly. Calgon Carbon announced a 25ktpa expansion at its Mississippi plant in 2020 at a cost of US$185m. We understand this came online in 2022. Carbonxt is expecting saleable product from the JV facility in 1H2024, with an initial 10ktpa delivered at a capital cost of just US$20m. The JV parties believe this can be doubled to 20ktpa for a modest additional outlay. Carbonxt's entry into the liquid-phase market appears well timed. The Company estimates that the current Activated Carbon market for the liquid phase is c.US$600m per annum, but the American Waterworks Association estimates the annual cost to comply with the regulations in its current form is US$3.8bn. Source: https://www.awwa.org/Portals/0/AWWA/Government/2023030756BVFinalTechnicalMemoradum.pdf?ver=2023-03-14-102450-257 Funds operated by this manager: |

26 Jul 2023 - Performance Report: PURE Income & Growth Fund

[Current Manager Report if available]

S&P 500 rose +6.5%, the Nasdaq was up +6.6%, whilst in the

UK, the FTSE 100 appreciated +1.2%.

26 Jul 2023 - Glenmore Asset Management - Market Commentary

|

Market Commentary - June Glenmore Asset Management June 2023 Globally equity markets were positive in June. In the US, the S&P 500 rose +6.5%, the Nasdaq was up +6.6%, whilst in the UK, the FTSE 100 appreciated +1.2%. The strength in the US indices was again driven by mega cap technology stocks. In Australia, the All Ordinaries Accumulation Index rose +1.94%. Materials and Financials were the top performing sectors, whilst Healthcare underperformed (driven by a negative earnings update from index heavyweight CSL). On the ASX, large cap stocks outperformed small caps, continuing a trend that has been in place for the last 18 months. We believe this trend will reverse once there is more clarity over the number of interest rate hikes required by the RBA to reduce inflation to its targeted 2-3% range, which should see small/mid caps on the ASX perform strongly vs large caps. Bond yields in both Australia and the US increased, with the Australian 10 year bond rate rising +42bp to close at 4.02%, whilst its US counterpart rose +22bp to 3.88%. In both cases, increased investor expectations of "higher inflation for longer" was the driver, with inflation proving more difficult to reduce to targeted levels than central banks would like. Consumer spending in particular, continues to be more resilient than expected despite ongoing headwinds from cost of living pressures. Whilst investor sentiment remains very cautious towards small/mid cap stocks, we continue to see numerous examples of mis priced stocks, which are well positioned to outperform once the current interest rate hiking cycle is complete. At this stage, our view is that the RBA will increase rates 2-3 more times to bring inflation to acceptable levels. Given the lagged impact of monetary policy, we expect inflation to continue to fall over the next 6-12 months. Funds operated by this manager: |

25 Jul 2023 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

25 Jul 2023 - Investment Perspectives: Why best-in-class mall rents are recession resilient

24 Jul 2023 - Performance Report: Digital Asset Fund (Digital Opportunities Class)

[Current Manager Report if available]

24 Jul 2023 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]