NEWS

7 Aug 2023 - The three factors driving stock returns

4 Aug 2023 - Hedge Clippings | 04 August 2023

|

|

|

|

Hedge Clippings | 04 August 2023 To the surprise of very few, including the combined team at Hedge Clippings, for the second month in a row, the RBA and Philip Lowe left interest rates on hold at 4.1% this week at his penultimate board meeting. That doesn't mean we're out of the woods, or that future rises are off the table. Equally it's too early to forecast an early spring, and an associated easing, any time soon. As usual, particularly after his previous attempt of unsuccessfully predicting a date for future movements, Lowe was cautious, as the following extract from his post meeting statement shows: "Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon the data and the evolving assessment of risks." We think that's the RBA's version of having two bob each way on a two horse race, but with the inevitable over-ride to finish: "The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that." Today's RBA quarterly statement on monetary policy was also to a great degree a case of stating the obvious: Inflation is on the way down, but still too high. The labour market is still tight, unemployment at 3.5% is historically low, but both job vacancies and underemployment are showing positive signs (unless you're under-employed). Economic growth is subdued, and the outlook for the domestic economy is "subject to a range of uncertainties". Finally, "there are both upside and downside risks to the inflation outlook." There's another two bob each way bet! Ever consistent, the Statement's Overview page finished with their familiar and now favourite phrase: "The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome." We can't say we haven't been warned. Meanwhile yesterday's ABS Retail Sales figures for the June quarter confirmed just how finely balanced the economy is. The numbers showed that volumes fell (-0.5%) for the third quarter in a row, the first time since 2008 (during the GFC and the chaotic days of Kevin '07) that Australia has clocked three negative quarters on the trot. The June result takes the full fall over 12 months to 1.4%, the worst 12 month result (excluding the period during the Covid lockdown) since Keating's "recession we had to have" in 1991. Retail spending on food, takeaway, cafes and restaurants fell, as did household goods, while clothing, footwear, and "personal accessories" were the only category to go against the trend, rising 1.1%. On the face of it, those struggling cut back on food and household items, but still looked after their appearance and personal items, obviously the new "real" necessities of life. However, it does seem that Lowe will leave the RBA in mid-September with the economy still on his "narrow path". Whether Michele Bullock can carry on the task, and steer the Australian economy to its much hoped for soft landing, remains to be seen. News & Insights Stage two of the downturn - earnings downgrades | Touchstone Asset Management In Conversation with Airlie's Analysts | Airlie Funds Management June 2023 Performance News Digital Asset Fund (Digital Opportunities Class) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

4 Aug 2023 - A site visit with a difference

3 Aug 2023 - In Conversation with Airlie's Analysts

|

In Conversation with Airlie's Analysts Airlie Funds Management July 2023 |

|

Airlie Australian Share Fund Portfolio Manager, Emma Fisher, engages in a conversation with Airlie's senior analysts, Vinay Ranjan and Joe Wright. Emma discusses the performance of the Australian market during the past 12 months and asks Joe and Vinay to share insights on how some of their stocks have performed during the year within the Fund. This includes Mineral Resources, QBE Insurance and James Hardie. Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

2 Aug 2023 - Do they have your back or just your back pocket? The fun, games, and fees of equity investing

|

Do they have your back or just your back pocket? The fun, games, and fees of equity investing Collins St Asset Management July 2023 FY23 recap: ASX 200 defies the bears to end up +10% over last financial year It is often said that: When someone with money meets someone with experience, the person with the experience gets the money and the person with the money gets an experience. For equity investors, regardless of whether or not they choose their own investments or outsource some or all of that responsibility to an external manager/adviser, this remains a very real and important risk to be on top of. Many Directors and Management teams do not run companies for the benefit of shareholders despite all of the claims and promises of future gold and glory laid out in glossy annual reports. Fat salaries for start up company Directors, gifted equity to management in large established businesses and all manner of perks and parties along the way are, all too sadly, par for course. To that end, its important to understand the governance structure of a company and the way in which senior decision makers are remunerated before deciding whether or not to invest. Some key questions we at Collins St Asset Management seek to understand before deploying capital include:

Sadly, a rolling stone gathers no moss in much the same way as an upwardly mobile executive can suffer no financial pain by moving from one company to the next just before the next crisis is uncovered. Of course, Directors and senior Management are not alone in their pursuit of cushy rent-seeking corporate opportunities. Whilst many intermediaries in the funds management space are often no better, there are a variety of fee models on offer which invariably incentivise different behaviours. The table below provides an overview of some of the different ways professional fund managers may seek to charge their clients: Overview of fee structures Author: Rob Hay, Head of Distribution & Investor Relations For wholesale investors only |

|

Funds operated by this manager: |

1 Aug 2023 - Stage two of the downturn - earnings downgrades

31 Jul 2023 - Performance Report: PURE Resources Fund

[Current Manager Report if available]

31 Jul 2023 - Will service stations be stranded assets?

|

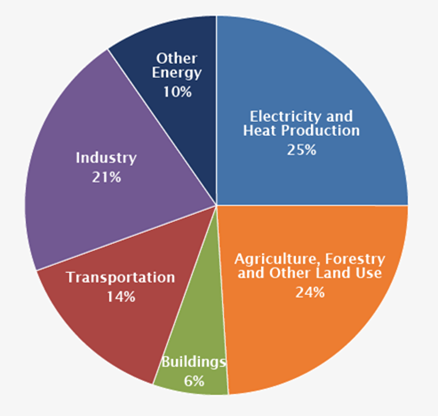

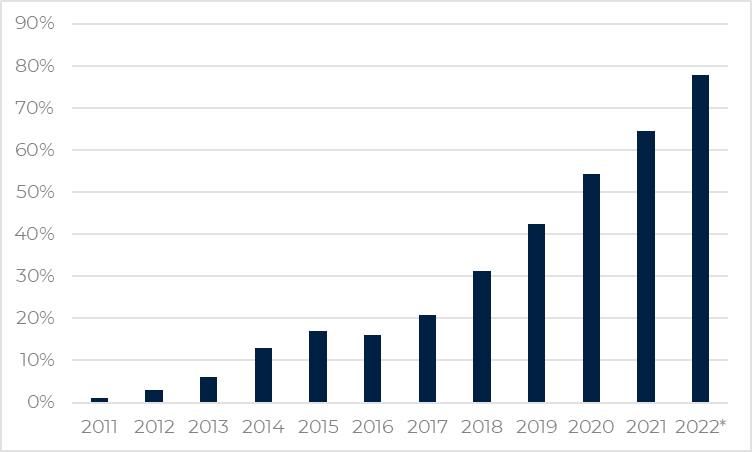

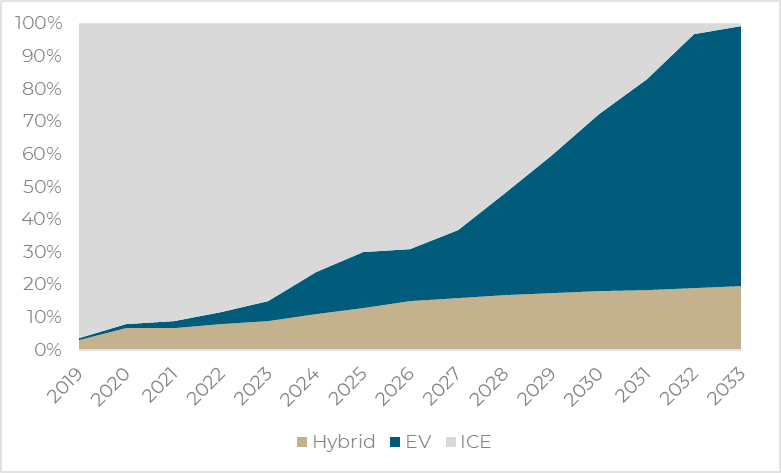

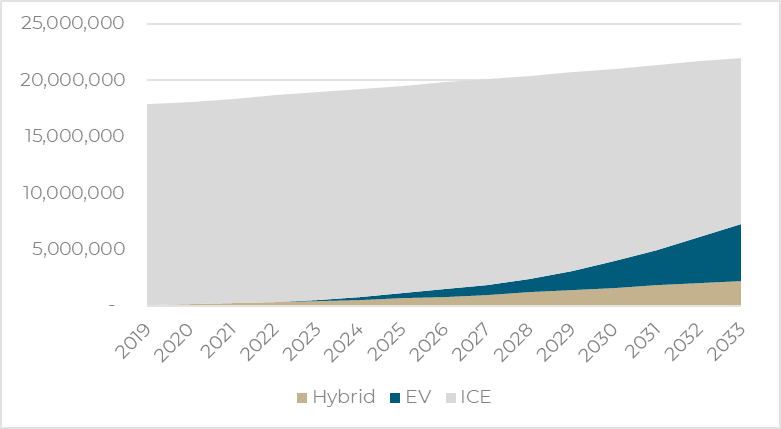

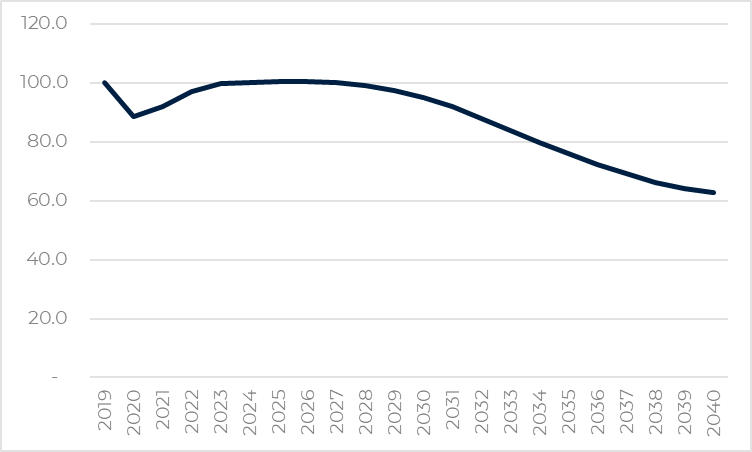

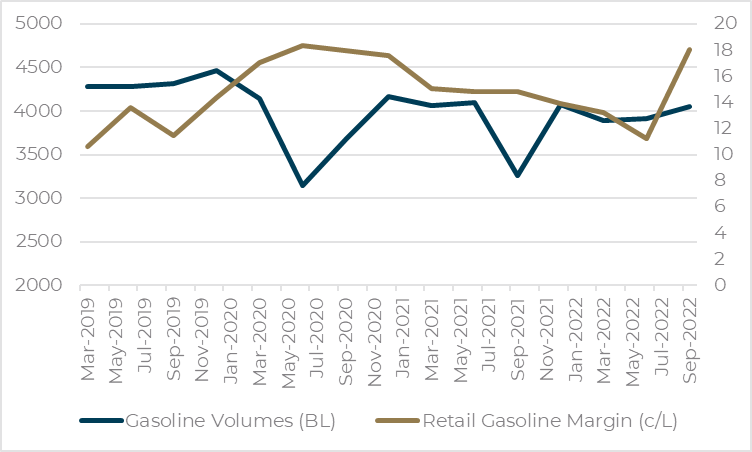

Will service stations be stranded assets? Tyndall Asset Management June 2022 At the same time as we are seeing global policy initiatives seeking to further accelerate the uptake of electric vehicles (EVs), corporate activity in the fuel and convenience retailing sector has stepped up. If the common belief that EVs will displace the need for Fuel Retailers, why are industry players increasing their capital allocation to the sector? We investigate the outlook for Fuel Retailers against the commonly held perception that they will ultimately be stranded assets. With the transport sector accounting for 14% of global carbon emissions (refer Figure 1), internal combustion engines (ICEs) are directly in the firing line of governments seeking to meet reductions targets. Further, the development of cost-competitive alternative technologies means that the transition to cleaner transport is not only achievable but now gathering significant momentum around the world. Figure 1: Global Greenhouse Gas Emissions by Economic Sector Source: US Environmental Protection Agency The consequence is that ICEs are likely to go the way of the steam engine over time. This begs the question - will service stations become stranded assets? What are the prospects for these sunset industries? Three years ago the answer to these questions was largely speculative. However, the COVID-19 period has created an ideal test environment in which the impact of a reduction in fuel volumes can be readily examined. This paper reviews the data and the risk that service stations become stranded assets. It is beyond debate that over the next two decades the vast majority of Australia's passenger vehicle fleet will transition to cleaner fuels. Car manufacturers are moving rapidly towards EVs, recognising the mega trend and the cost comparability. Governments around the world have varying incentives to assist in the transition, with adoption of EVs having increased rapidly as price-competitive and range issues have been overcome. Australia lags but won't foreverWhile adoption of EV's in Australia has been relatively slow to date, it would be naïve to consider that this will remain the case. Norway is the country most advanced in electric vehicle penetration of new car sales. This has come on the back of significant government incentives for the electric vehicles and support for infrastructure development. While EVs were only 1% of new car sales in 2011, the Norwegian Office of Vehicle Statistics reports that in the nine months to September 2022, EVs represented 77.8% of new car sales (refer Figure 2). Figure 2: Electric Vehicle Share of New Car Sales - Norway Source: Road Traffic Information Council (OFV); Electric Vehicle Association (Elbil). *Year to date September 2022. What would this adoption rate mean for Australian fuel volumes?We have modelled the implications of an adoption rate as rapid as Norway's for the Australian market, allowing us to map out the potential impact on retail fuel demand as the energy transition proceeds. We have also assumed that the uptake of hybrid vehicles accelerates from recent trend rates, as more models become available. Combined these assumptions indicate that ICE vehicles will be a rapidly declining proportion of new car sales, to the point that they are all but eliminated by 2033. Notably this is faster than the proposed legislated goal of ending ICE vehicle sales in the UK and EU by 2035 and close to the recent Biden Administration proposal to phase out ICE vehicles by 2032. Figure 3: Composition of New Car Sales (Australia) Source: VFACTS, Tyndall estimates While the composition of new car sales changes rapidly in a decade, the impact on the vehicle fleet (refer Figure 4) is a much slower process. Under this scenario, hybrids and electric vehicles will represent only one-third of the total fleet by 2033. Figure 4: Australia's Vehicle Fleet Mix Source: VFACTS, Tyndall estimates What is evident from this analysis is that the impact on volumes from the transition to electric vehicles is extraordinarily protracted (Refer Figure 5). Retail volumes are not forecast to decline from 2019 levels until 2029. And even then, the decline is only 1.3ppts. The impact does accelerate quite significantly during the following decade, with 2040 volumes forecast to be c33.5% lower than 2019 levels. Figure 5: Fuel Volumes (Indexed to 2019) Source: ABS, Tyndall estimates A longer-term volume contraction is only half the storyWhile significant and at face value perhaps alarming, a significant decline in fuel volume is only half the story. The other relevant variable of course is price, and the COVID-19 experience has demonstrated the ability of the fuel retailing industry to maintain dollar gross margin in the face of falling volumes. This rational industry response perhaps benefited from the recent memory of unprofitable discounting that occurred during calendar 2018. Chart 6 shows the trends in gasoline volumes and retail gasoline margins over the recent past - capturing the period of COVID disruption. As the chart shows, Fuel Retailers responded to lower volumes with price increases, such that dollar gross margins expanded. Figure 6: Retail Gasoline Margins and Volumes Source: Australian Petroleum Statistics, Department of Energy; Australia Institute of Petroleum; Tyndall In the June 2020 quarter, which includes the early part of the pandemic and national lockdowns, fuel volumes fell ~45%. Retail margins in that period averaged 18.3 cents/litre, ~46% above the 2019 average. Preparing for the futureAs highlighted above, the medium-term outlook for Fuel Retailers is sound, with the impacts of the fleet conversion to electric vehicles a very slow burn that will not materially impact volumes for a decade. That said, the longer-term outlook does point to significant erosion of fuel volumes. While pricing offsets to combat this have been proven possible through the COVID experience and at face value are not unaffordable, the very long-term scenario is that retail fuel volumes go to zero. We are watching this area closely and observing how the listed participants are progressing their strategies. Both Viva Energy and Ampol have de-risked their businesses by selling service station properties but with long-term options that provide ongoing control over the site. Author: Tim Johnston, Portfolio Manager Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

28 Jul 2023 - Hedge Clippings | 28 July 2023

|

|

|

|

Hedge Clippings | 28 July 2023 One of the difficulties of including the topics of inflation and interest rates in a weekly commentary is that in recent times it has been difficult to avoid the subject, even if it does end up becoming a tad tedious - quite possibly for both the author and recipients! This week therefore we'll cover it briefly before moving onto managed funds and peer group performances. True to our previous expectations, this week's June CPI figures (+0.8% for the quarter, and 6.0% over 12 months), provided some positive indications for inflation, and thus for next week's decision on interest rates. Wednesday's figures at least justified the RBA's July pause, and should herald a further pause next Tuesday. It's too early to claim the inflation battle has been won, and further "stickiness" could well trigger calls for another rise, but the June quarter figure of just 0.8% (annualised at 3.6%) is the lowest since, or equal to, the quarterly result for the June quarter of 2021. All this with historically low unemployment, and a strong labour market. The RBA's current cash rate of 4.1% (assuming it doesn't rise next week) is well below US rates, which rose again by 0.25% to 5.25 to 5.5% this week, as did European rates, while the UK's rate is at 5%, and is expected to touch 6%. The previously much maligned Philip Lowe looks to have been vindicated for his "narrow path" approach, balancing the fight against inflation with the need to keep the economy running, and with as close to full employment as possible. However, don't expect the RBA to take their foot off the pedal too quickly, and certainly don't expect any forecasts when that may happen from incoming RBA governor Michele Bullock. While overseas central banks are still increasing rates in an attempt to put the final nail in their inflationary coffin, Australia may have to accept 4.1% for a while longer yet to ensure the RBA's 2-3% target is secure. Moving right along... to fund performance: Inevitably, at the individual fund level the results over the past year or so have been varied. Over the six months to June, 58% of equity based funds outperformed the ASX200, while over twelve months that number dropped to just 8.1%, indicating how difficult many managers found 2022 as central banks grappled with unexpected inflation, and Russia invaded Ukraine. However, all but one of the 17 Peer Groups that make up the Fund Monitors database of 700+ managed funds recorded a positive result in June, and also over the previous three and six months. The exceptions were Fixed Income - Bonds (-0.48% in June, and -0.50% for three months) and Property (-0.32% over six months). However, over one year to the end of June, all Peer Groups (averages) were in positive territory, with Equity Long, both Large and Small Cap, and Australian and Global, all returning 10% or more. Digital Assets topped the twelve month list at 32.64%, having recovered from their (very) average 12 month return of -48.68% to December 2022. Looking at comparative Peer Group performances on a broad consistency basis (in other words, no drawdowns over both the short or longer term), the standouts have been Equity Alternatives, Alternatives, Fixed Income, and Hybrid Credit. Full details (registration required) can be found here. Finally, next Tuesday at 4.15 PM AEST we are running the latest of our webinar series, featuring three managers investing in Infrastructure assets. Register here or below to join AFM's COO Damen Purcell, as he delves into the opportunities and risks of infrastructure investing with Sarah Shaw from Bennelong's 4D Infrastructure, Ben McVicar from Magellan's Infrastructure Fund, and Matt Lorback from Atlas Infrastructure. Upcoming Events Infrastructure Funds - Analysing the Opportunities and Risks Webinar | FundMonitors.com Altor AltFi Income Fund - June 2023 Quarterly Webinar Update | Altor Capital News & Insights Market Commentary | Glenmore Asset Management Forever Chemicals - PFAS | PURE Asset Management June 2023 Performance News Skerryvore Global Emerging Markets All-Cap Equity Fund Bennelong Concentrated Australian Equities Fund Insync Global Quality Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

28 Jul 2023 - Performance Report: Insync Global Capital Aware Fund

[Current Manager Report if available]