NEWS

Performance Report: Quay Global Real Estate Fund (Unhedged)

Since inception in January 2016, the Quay Global Real Estate Fund (Unhedged) has returned +5.41% per annum, a difference of +2.84% relative to the FTSE EPRA/ NAREIT Developed NET TR benchmark which has returned +2.57% on an annualised...

Read more...

Glenmore Asset Management - Market Commentary

Globally equity markets in September declined materially

driven by rising bond yields. In the US, the S&P 500 fell -4.9%,

whilst the Nasdaq declined -5.8%. In the UK, the FTSE 100

outperformed, rising +2.3%, due to its heavy...

Read more...

Performance Report: Kardinia Long Short Fund

The Kardinia Long Short Fund returned -1.81% in September, outperforming the ASX 200 Total Return benchmark by +1.03% . Since inception in May 2006, the fund has returned +6.99% per annum,an outperformance of +0.85% relative to the...

Read more...

Performance Report: Delft Partners Global High Conviction Strategy

Since inception in August 2011, the Delft Partners Global High Conviction Strategy has returned +14.28% per annum, an outperformance of +1.51% relative to the All Countries World (AUD) benchmark which has returned +12.77% on an annualised...

Read more...

10k Words | October 2023

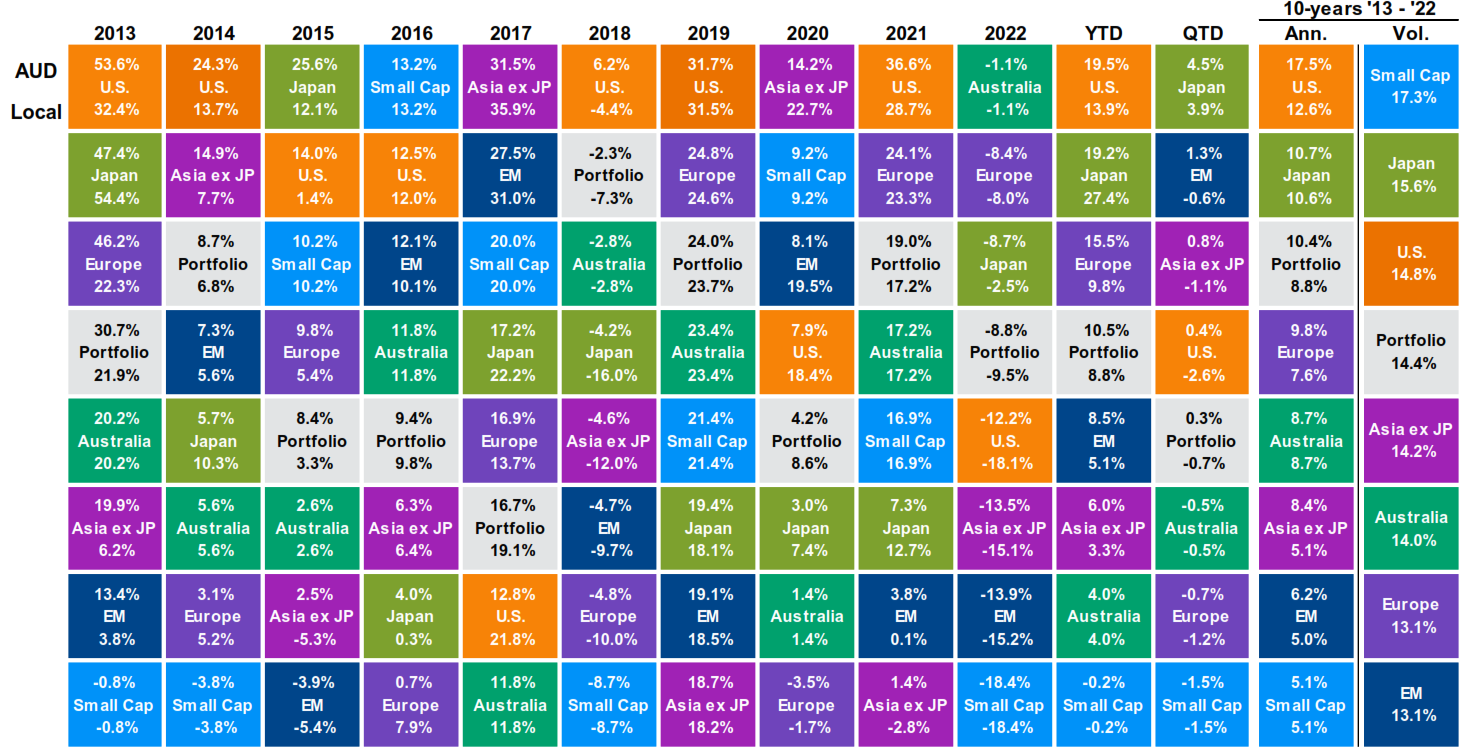

Small caps have gone through scotched earth in the US & here," Bell Potter highlights, with JP Morgan showing small caps to be the most volatile and lowest returning asset in the past ten years.

Read more...

Hedge Clippings | 13 October 2023

Has the Fed lost the (dot) plot?

Australia's RBA has its bulletin to update the rest of us to their thinking after their monthly board meeting, but they rarely spring any surprises. They basically say what they want us to hear,...

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund returned -1.97% in September, outperforming the ASX 200 Total Return benchmark by +0.87%. Since inception in June 2017, the fund has returned +18.06% per annum, a difference of +10.49% relative to the...

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund returned -0.57% in September, outperforming the ASX 200 Total Return benchmark by +2.27%. Since inception in February 2002, the fund has returned +12.34% per annum, an outperformance of +4.5% relative...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund returned -2.83% in September, performing in line with the ASX 200 Total Return. Since inception in June 2018, the fund has returned +9.61% per annum, an outperformance of +2.42% relative to the benchmark...

Read more...

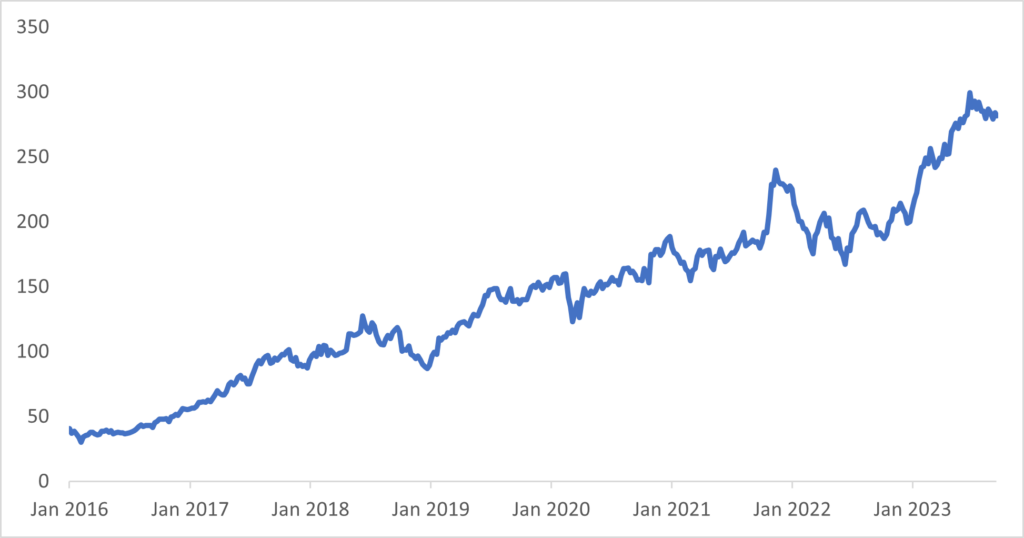

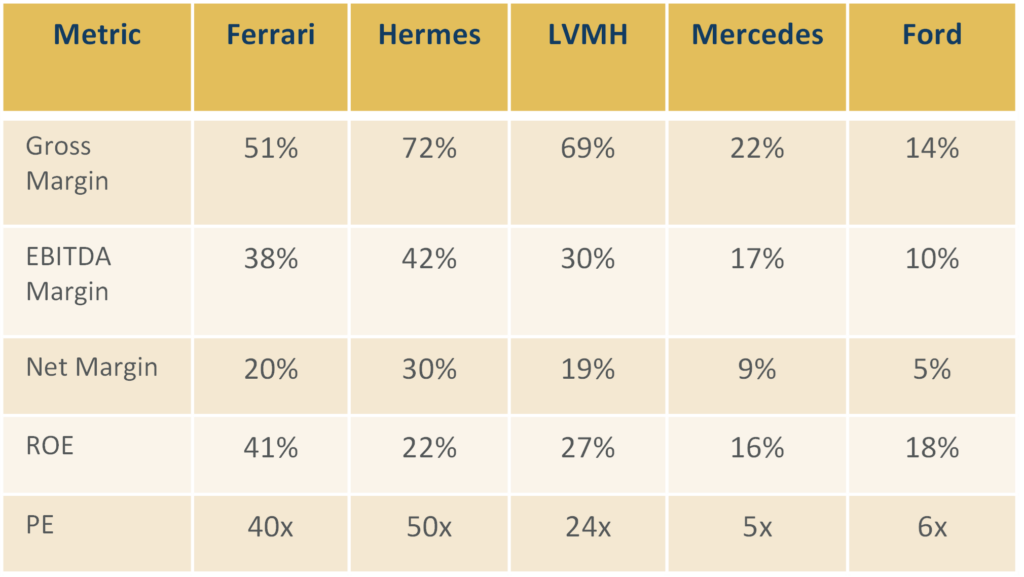

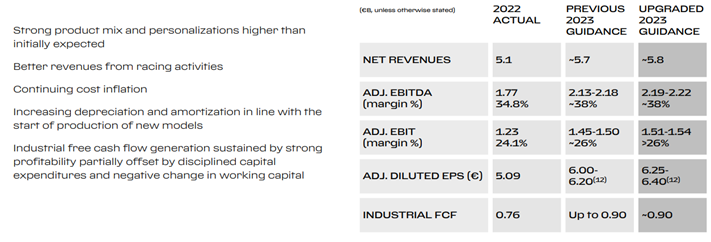

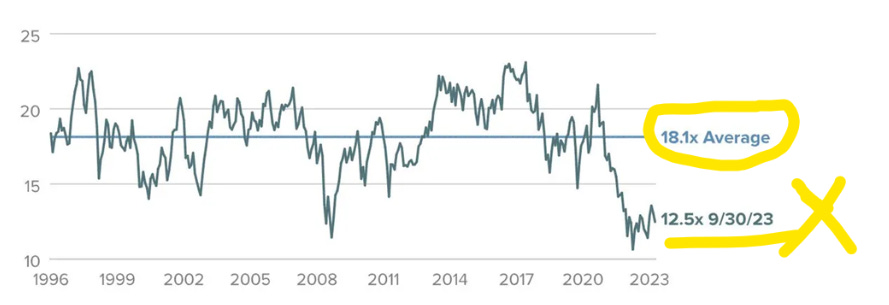

Ferrari: The case for RACE (RACE IM)

Ferrari is one of the world's most iconic brands. It's also an amazing stock. Ferrari was founded in Italy in the 1940s and was spun off from Stellantis in 2016 under the ticker RACE IM.

Read more...