NEWS

29 Nov 2023 - 10k Words | November 2023

|

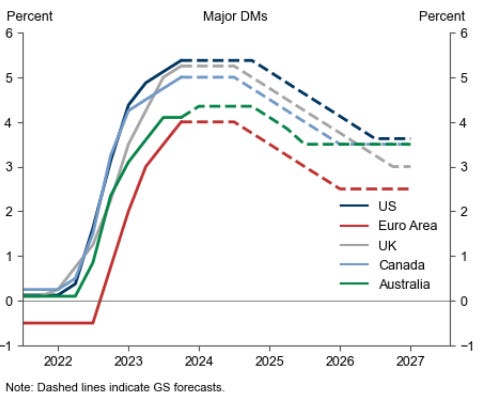

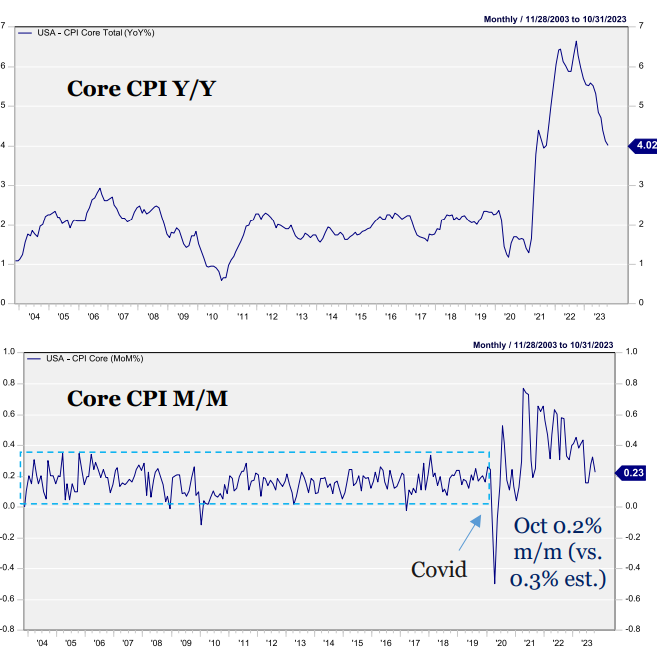

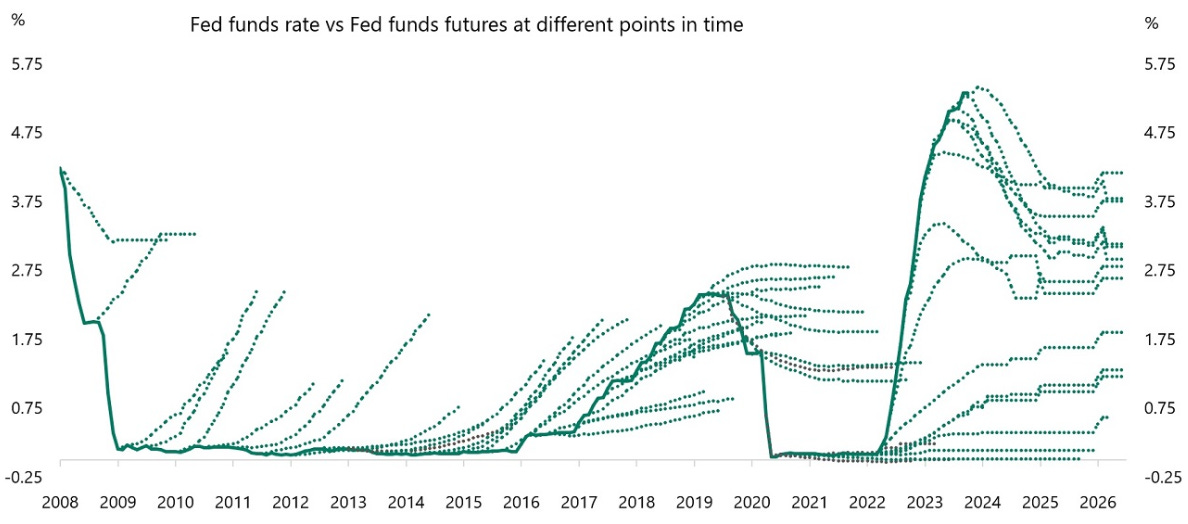

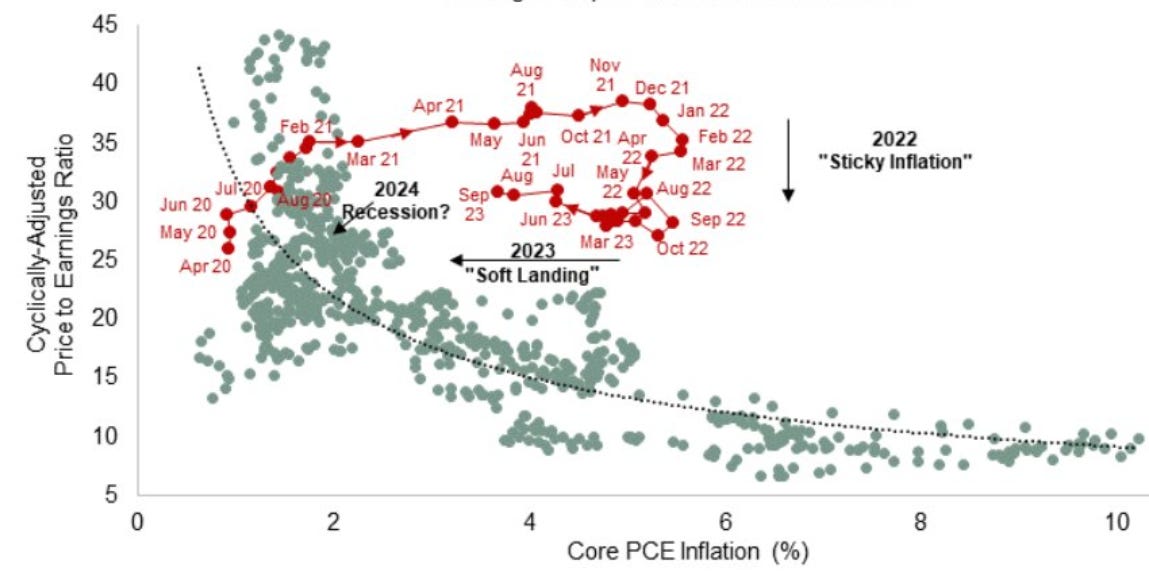

10k Words Equitable Investors November 2023 "Although we forecast that major DM central banks (aside from Japan) are finished hiking, our baseline forecast implies little incentive for them to cut interest rates in the near term," Goldman Sachs foreshadows, with Raymond James charting the cooling of core US inflation to levels still higher than seen for many years. Our favourite chart this month has Apollo showing that the market is almost always wrong about what the Fed will do next. Apollo backs up with a graphic on "weak demand". SMBC NIkko gives us a view on the relationship between inflation and valuation. Tech stocks are at record highs relative to the broader market as Bank of America charts, while Goldman shows the impact on market valuations. Equitable Investors looks at movement in the EV/EBITDA multiple on tech stocks relative to bond yields. We get another take on the surge in index concentration from Bespoke - and small v large via Bank of America. Deutsche Bank reckons AI didn't drive markets. Finally we get stuck into VC, where Crunchbase data shows significantly less unicorns being born and funding remaining subdued, with the Refinitiv Venture Capital Index remaining well of its highs despite recent gains. Goldman Sachs' policy rate forecasts for developed markets

Source: Goldman Sachs Core US CPI

Source: Raymond James The market is almost always wrong about what the Fed will do

Source: Apollo Mentions of "weak demand" during S&P 500 earnings calls

Source: Apollo Earnings multiples mapped against inflation

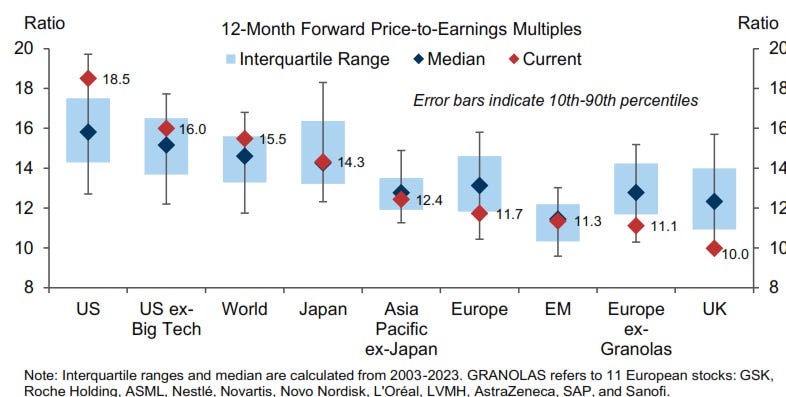

Source: SMBC NIkko via Bloomberg Tech sector at all-time high vs S&P 500

Source: Bank of America Price-to-Earnings multiples by market - tech sector elevates US multiples

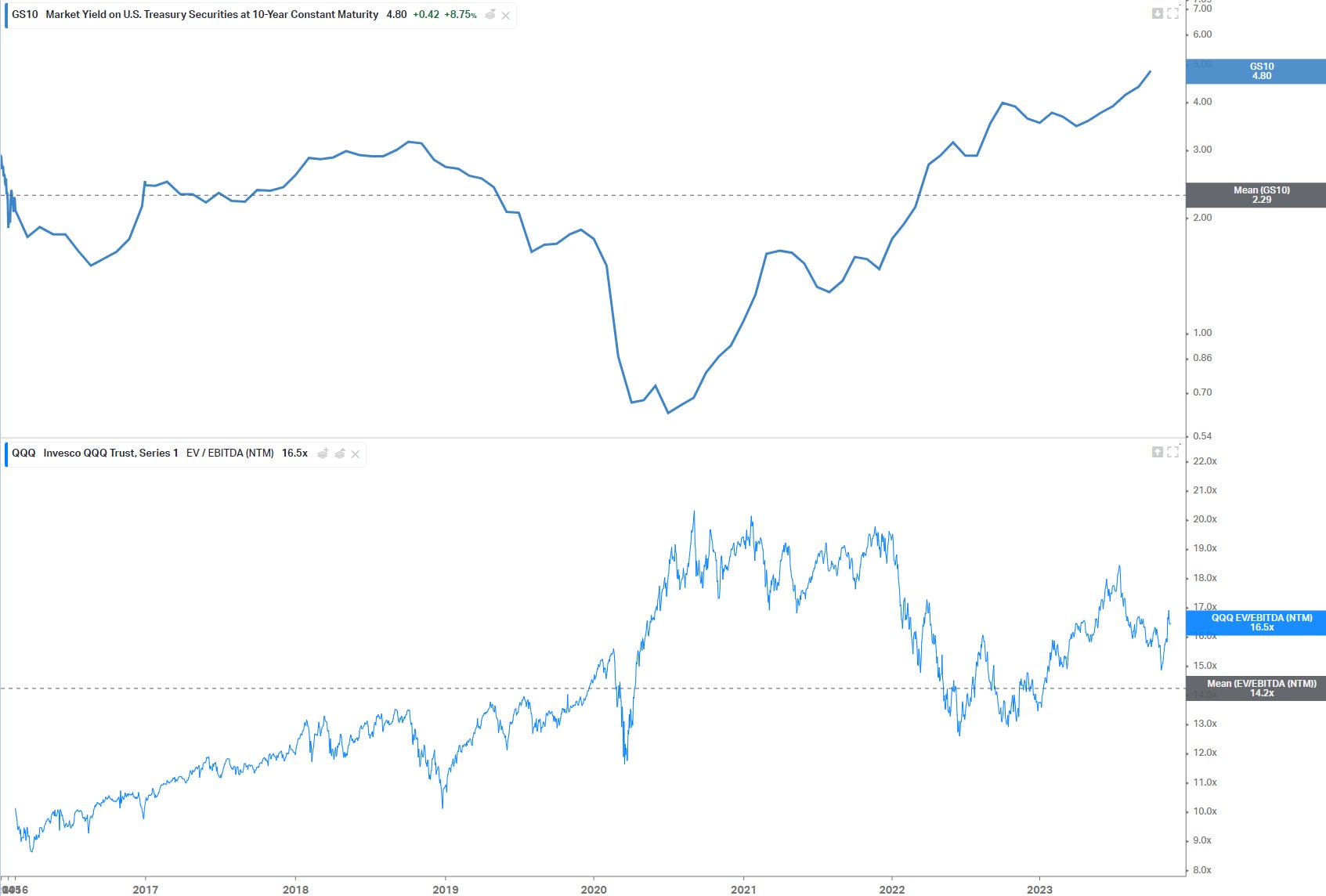

Source: Goldman Sachs US 10 year bond yield (top) mapped against US tech sector (QQQ ETF - bottom)

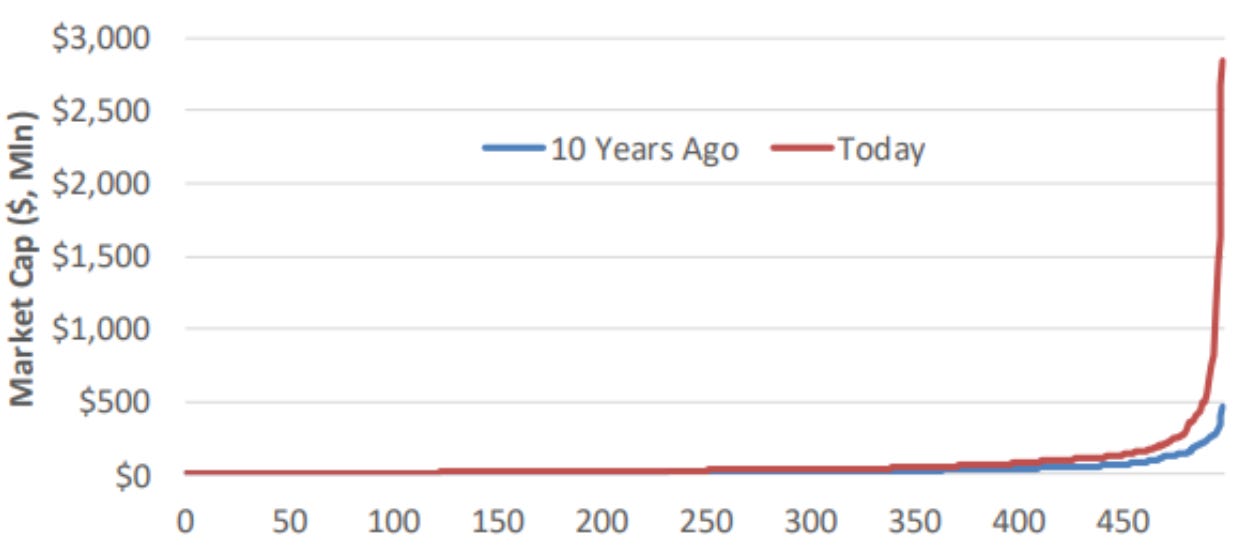

Source: Koyfin, Equitable Investors S&P 500 stocks from smallest to largest - 10 years ago v today

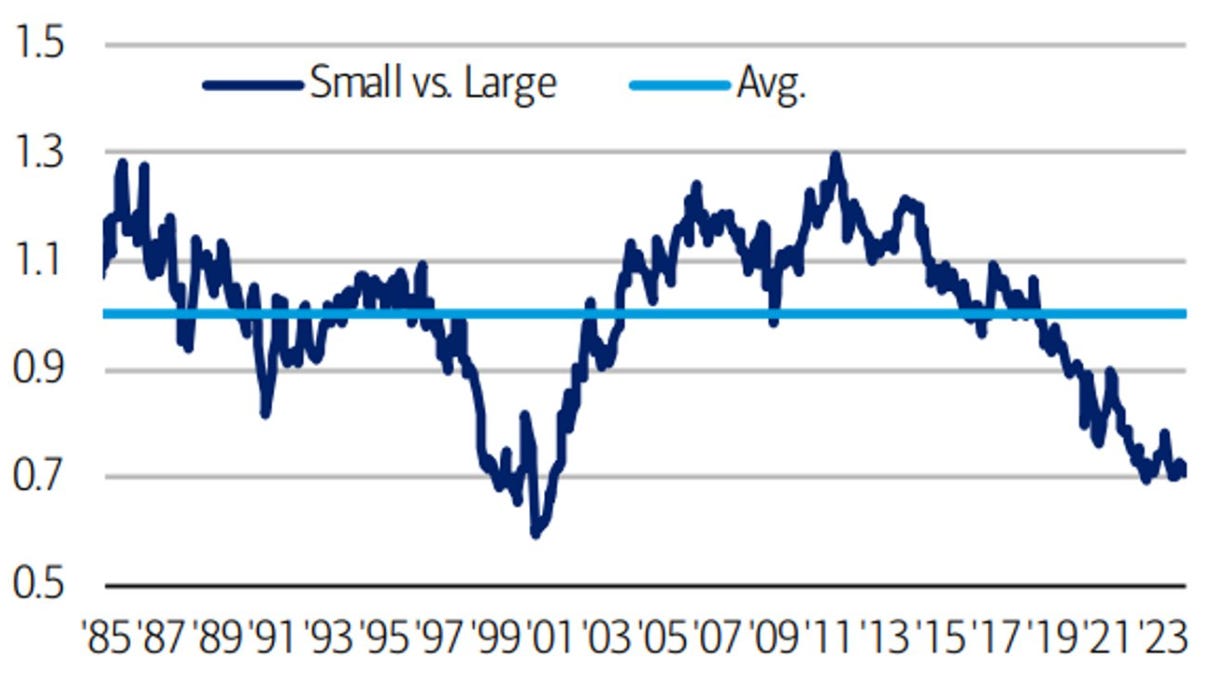

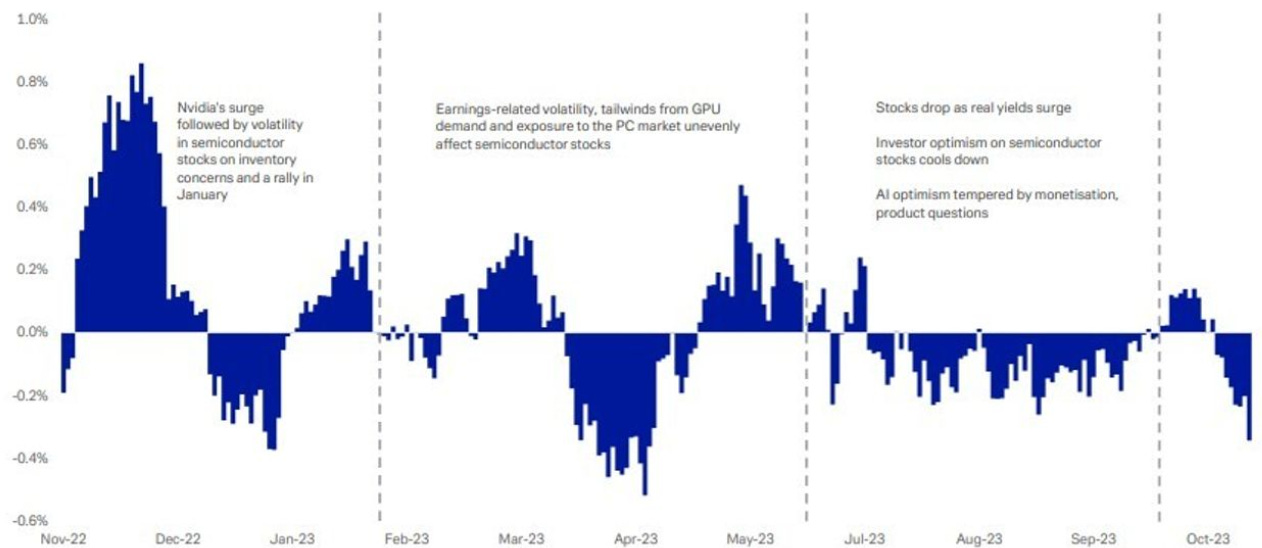

Source: Bespoke US small caps histoically cheap vs large caps (Forward PE of Russell 2000 v Russell 1000) Source: Bank of America Difference between abnormal returns for semiconductor and software firms, 20 day moving average

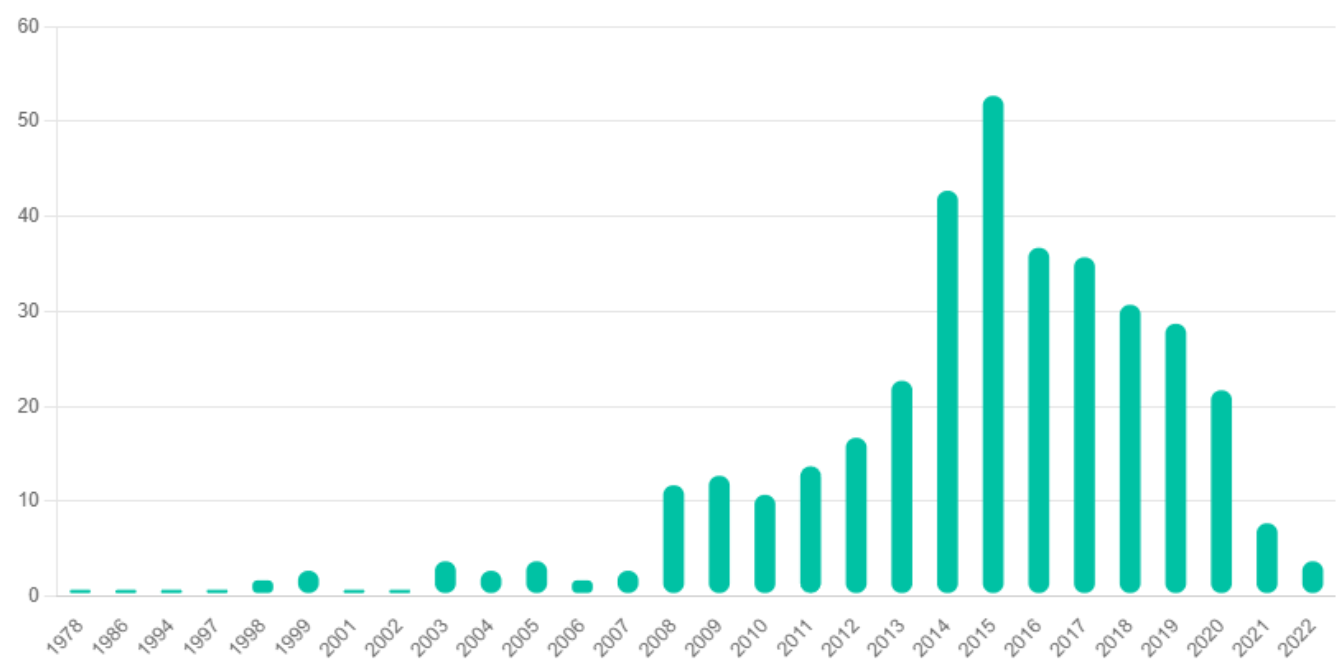

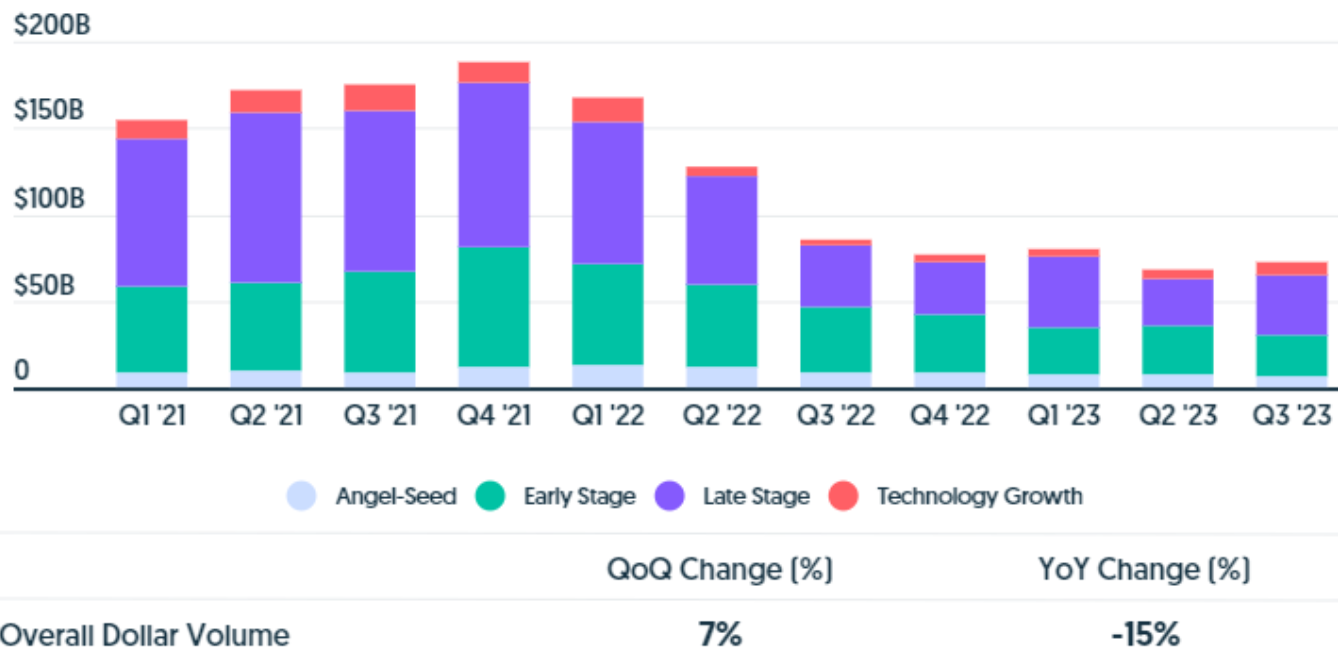

Source: Deutsche Bank Emerging unicorns by the year founded Source: Crunchbase Global venture funding (US dollar volume)

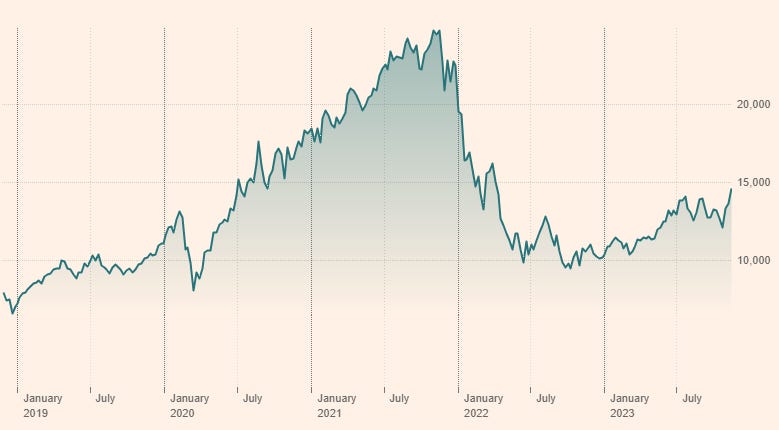

Source: Crunchbase Refinitiv Venture Capital Index Source: Financial Times November Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |

28 Nov 2023 - Performance Report: PURE Resources Fund

[Current Manager Report if available]

28 Nov 2023 - Acceleration of innovation now spells danger for investors

|

Acceleration of innovation now spells danger for investors Insync Fund Managers November 2023

A new app, 'Threads' built by Instagram, which enables the sharing of text updates and joining public conversations, recently reached 100 million users within an astonishing five days. 'This is a powerful demonstration of the lightning speed at which innovation is accelerating,' says Insync Funds Management (Insync)'s Head of Strategy and Distribution, Grant Pearson. 'Make no mistake, the frantic pace of change now spells danger for investors.' For context, Facebook took 4.5 years to reach 100 million users, Instagram took 2.5 years, TikTok achieved it in nine months, and Chat GPT took two months. 'The reason this means big trouble for investors is that they could be in the right company today and, as little as weeks later, be in the wrong company,' Mr Pearson says. The pace of innovation does not just affect pure technology plays. 'All companies could be affected as they all rely on technology of some sort,' he says. 'If their competition embraces new technology better and faster, a dominant company today may find its revenues and profits under immediate threat. And let's not forget brand new competitors for firms that technology has opened the gates to.' Mr Pearson says that while in the past investors had months or even years to discover an emerging technological breakthrough, assess it, seek views, and then act; now they have next to no time and the skills required to do it are often outside the investment industry. 'In fact, the average life span of successful businesses is being compressed into less than 10 years duration,' he went on to say. 'This is disruption accelerating at the same time that time frames are compressing.' Annual increases in computing processing power are now many hundreds of times faster than previous computers which are themselves under five years old. 'Look out further, say six years, and it's even more profound,' he says. 'Google's latest Sycamore Quantum Computer, testing now with operational status by 2029, is an astonishing 241 million times more powerful than today's fastest supercomputers!' In other words, Sycamore can solve in seconds a problem that takes today's fastest supercomputer 47 years. 'This first iteration of Sycamore is only the 'Model T' of what is to come,' Mr Pearson says. 'The alarming thing for the investment community is that we are only at the very beginning of this acceleration. It is akin to sitting in a roller coaster as it has just tipped into its near vertical first run.' Couple this extraordinary increase in power with the advances in AI and Mr Pearson says gargantuan change is afoot, change that will revolutionise our world and turn most industries upside down, along with investor returns. 'Fund managers and researchers need to quickly create robust means to assess and counter the acceleration of technological change and shrinking time frames, to reduce the threats to returns, as well as better understand which companies will deliver the decent performances of tomorrow,' he says. 'Our industry has a reputation for being slow to change, with egos routinely getting in the way of adapting. Investors need to check carefully that their fund managers are very clear as to how these factors impact their investment processes if they are not to be blindsided and saddled with disappointing returns.' Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

27 Nov 2023 - Performance Report: Emit Capital Climate Finance Equity Fund

[Current Manager Report if available]

27 Nov 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||

| EQT Tax Aware Australian Share Fund (Retail) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Tax Aware Australian Share Fund (Wholesale) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Tax Aware Diversified Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| EQT Diversified Fixed Income Fund (Retail) | ||||||||||||||||||||

|

||||||||||||||||||||

| EQT Diversified Fixed Income Fund (Wholesale) | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

||||||||||||||||||||

| Maple-Brown Abbott Australian Sustainable Future Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||

|

Subscribe for full access to these funds and over 750 others |

24 Nov 2023 - Hedge Clippings | 24 November 2023

|

|

|

|

Hedge Clippings | 24 November 2023 As much as we'd like to move on from discussing inflation in Hedge Clippings each week, the reality is that while lower than it was, it will be some time before the genie is safely back in the bottle. And while that's the case, there's little chance of interest rates falling, either locally or offshore in the US, UK or Europe. In the US there were hopes that they might consider easing sooner rather than later, but more recent minutes from the Federal Reserve's November meeting indicate a distinct unwillingness to do so, fearing that pivoting to a downward trend in rates too soon would potentially waste the hard won success to date. If anything the Fed warned rates could still rise if required, and meanwhile they'd "proceed carefully" before moving. In the UK - where inflation has been as high as 11% and is now back down to 4.6% - the message is the same. The UK kept rates steady at 5.25% for the second time following 14 consecutive hikes, but BoE governor Andrew Bailey was clear that he wasn't going to be rushed into cuts, saying the fear of persistent inflation was too great to risk doing so. Equally ECB president Christine Lagarde echoed those thoughts. Meanwhile at home freshly appointed RBA governor Michele Bullock scotched any thoughts that the fight had been won, even singling out dentists and hairdressers as jumping on the price rise bandwagon and pushing up inflation in the services sector. While unlikely that there'll be a further rate rise in December, and with no RBA meeting in January, it doesn't rule out yet another move upward in February or March. If anything Bullock is sounding more hawkish than Philip Lowe, possibly because she doesn't have his legacy of saying rates wouldn't rise until 2024. As Bullock noted in her speech to economists during the week, interest rates are a "blunt instrument" when it comes to taming inflation, but it's also pretty much the only instrument she has. And as we've noted before, that instrument strikes those least able to cope, assuming they have a mortgage. What hasn't happened yet - and we don't believe it will - is that increased mortgage rates will lead to an increase in arrears, and subsequently forced sales and falling house prices. That scenario would only be predicated on a full scale recession, which we also think unlikely. Even without a mortgage, rental rates are also increasing as investors strive to offset increased repayments, added to which the overall housing shortage is being magnified by short terms rentals via the likes of Airbnb, and high levels of immigration. So the outlook remains for inflation to remain front and centre, and therefore on our weekly agenda, for some time to come. Meanwhile, this week marked a few milestones and anniversaries - the most poignant one probably being the assassination of President Kennedy in Dallas 60 years ago last Wednesday. Once known by all those old enough to remember where they were when they heard the news, there's now a whole generation for whom the death of JFK is just a page in the history books. More up to date, and still on the subject of US presidents, three years ago today the formal transition to Joe Biden's administration began - so that's three years of Donald Trump claiming he didn't lose the election. You can't say he isn't persistent! News & Insights New Funds on FundMonitors.com Investment Perspectives: What does 'higher for longer' mean for real estate? | Quay Global Investors Stock Story: ResMed | Airlie Funds Management Events & Webinars October 2023 Performance News Bennelong Long Short Equity Fund Bennelong Twenty20 Australian Equities Fund Digital Asset Fund (Digital Opportunities Class) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

24 Nov 2023 - Performance Report: PURE Income & Growth Fund

[Current Manager Report if available]

24 Nov 2023 - Where nature meets business: The TNFD framework.

|

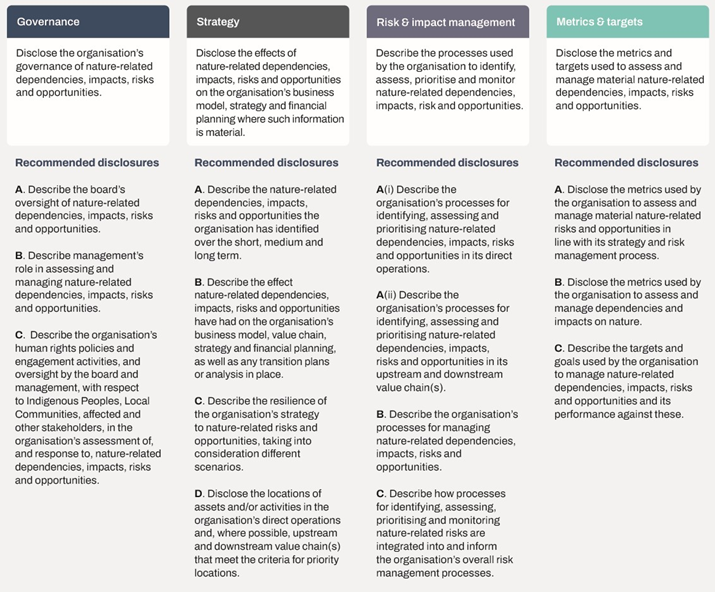

Where nature meets business: The TNFD framework. Tyndall Asset Management October 2022 The Taskforce on Nature-related Financial Disclosures (TNFD) is an international initiative that is developing a framework for companies and financial institutions to disclose their nature-related risks and opportunities. Climate and net-zero commitments are well understood, with corporations relying on the Taskforce for Climate-related Financial Disclosures that released a set of recommendations in 2017. The idea of TNFD is not entirely new. It has built upon the foundational success of the Task Force on Climate-Related Financial Disclosures (TCFD), which focuses on the financial implications of climate change for companies. However, as the global dialogue evolved, it became clear that climate was only a part of the broader environmental narrative. Biodiversity loss, land degradation, and ecosystem collapse pose significant risks to economies and businesses around the globe. The TNFD first came into existence in June 2021 to address this gap and ensure a holistic environmental approach in corporate disclosures. Importance of a nature-positive economyA 'nature-positive economy' is essential for a sustainable future and is a key concept that drives the TNFD framework. A nature-positive economy is an economy that has a net positive impact on nature, an economy that restores and regenerates nature rather than depleting it. Nature provides us with essential ecosystem services, such as clean air and water, food, and climate regulation. Without a healthy natural environment, our economy and society cannot thrive. The transition to a nature-positive economy is essential for a sustainable future. However, it is a transition that will require a concerted effort from all stakeholders, including governments, businesses, and individuals. The sectors that have the most impact on biodiversity are the logical companies that will be the early adopters of the TNFD recommendations. These sectors include materials, energy, agriculture and food & beverage. A framework for nature-based solutionsThe TNFD's final framework was published in mid-September 2023. It includes 14 recommended disclosures covering nature-related issues, impacts, risks and opportunities that are structured around four pillars (refer Figure 1). Figure 1: TNFD's recommended disclosures

Source: TNFD, Sept 2023. It is hoped that the TNFD provides a clear, structured framework that help corporates understand the implications of biodiversity and natural capital for their activities. The framework is intended to assist corporates and financial institutions manage their nature-related risks and opportunities, and to support the transition to a nature-positive economy. While it is largely based on the TCFD framework, it also considers the specific risks and opportunities associated with nature.

The TNFD framework is expected to be a valuable tool for companies and financial institutions to manage nature-related risks and opportunities. It will also help to promote the transition to a nature-positive economy. Some of the benefits of the TNFD framework include:

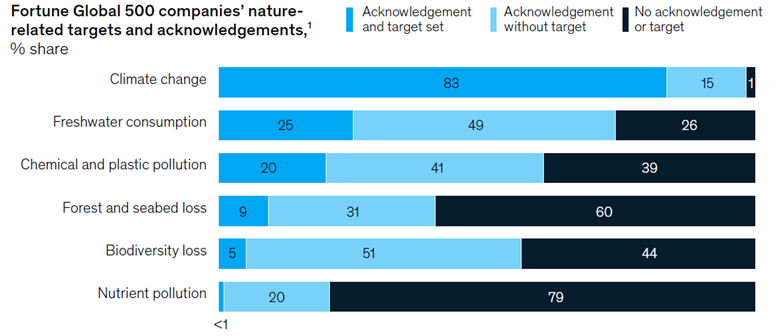

Global progressAlthough the TNFD framework has only recently been settled; governments and intergovernmental organisations have increasingly called attention to the impact on nature. Pleasingly, a rising number of businesses have made pledges relating to biodiversity. Figure 2: Corporate targets are less common for other dimensions of nature compares to climate change

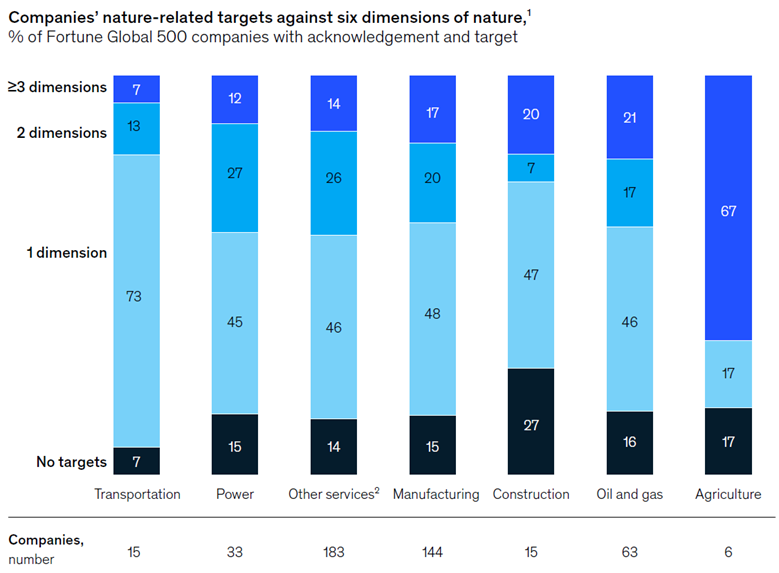

Source: McKinsey McKinsey has calculated that ~47% of Fortune Global 500 companies have set nature-related targets against one dimension of nature - generally this is against climate (refer Figure 2). Approximately 16% have set targets against three or more dimensions of nature and no companies have targets against all six dimensions that were looked at in this analysis. The Science-Based Targets for Nature (SBTN) initiative suggests that companies are more likely to focus on the key issues that directly impact their activities which could explain why no company has set targets against all six dimensions. Cutting the data based on a sector level reveals that the sectors that have a higher exposure to biodiversity risk are leading the charge on target setting. Figure 3: Fortune Global 500 Companies' nature-related targets by sector

Source: McKinsey Implementation of TNFDImplementing TNFD is not without its challenges. In particular, there's a need for:

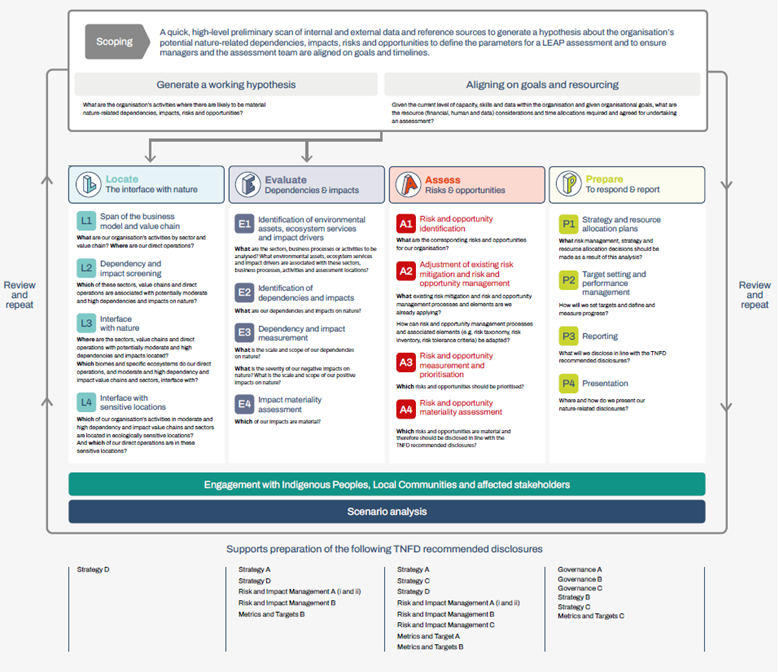

The framework is consistent with the recommended standards of the TCFD, ISSB (International Sustainability Standards Board) and GRI (Global Reporting Initiative). The recommendations have an intention to provide a practical solution for corporates to start their journey to increase the scope and disclosures over the coming years. The expectation is that, as with climate-related reporting, TNFD disclosures will improve over time. The LEAP approach - Locate, Evaluate, Assess and Prepare - has been developed by the TNFD to help organisations to identify, assess and manage nature-related risks and opportunities. While the approach is not a requirement, it is designed to help with identification and assessment. Figure 4 provides an overview of LEAP and its elements, which covers:

Figure 4: The TNFD approach for identification and assessment of nature-related

Source: TNFD, Sept 2023 Conclusion While the challenges are significant, the TNFD offers a critical pathway for integrating nature into financial decision-making and improving outcomes for our environment. The success of the TCFD suggests that with global cooperation and commitment, the TNFD can become an influential tool in driving sustainable business practices. Governments, financial institutions, environmental organizations, and businesses all have important roles to play. By implementing frameworks such as the TNFD, the global community takes a step closer to ensuring that the economic activities of today do not compromise the planet's well-being tomorrow. The shift from merely profit-driven strategies to those that also account for nature-related impacts signifies an evolution in global business practices. It is an evolution that is not just commendable but essential for the longevity and prosperity of both businesses and the planet. Tyndall will be increasingly engaging with corporates around biodiversity and promoting the implementation of the TNFD framework, as we have been with TCFD. According to work by Jarden, only 12 (24%) of ASX50 companies have nature-related targets. It was noted that BHP, Woolworths, South 32 and Origin Energy had undertaken TNFD pilots, and only Brambles and South 32 have linked nature to remuneration. Clearly, there is plenty of improvement required. We expect that those companies in sectors more exposed to nature-related risks such as agriculture, food and beverage, and mining, are likely to lead the charge. Author: Brad Potter, Head of Australian Equities Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

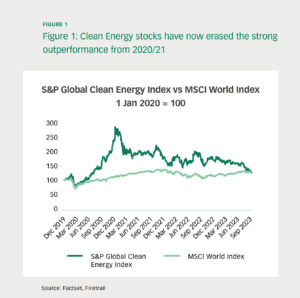

23 Nov 2023 - Renewable energy stocks: changing winds?

|

Renewable energy stocks: changing winds? Firetrail Investments October 2023 Decarbonisation is one of the most important challenges of our time, but it is also often one of the most difficult to successfully invest in. Renewable energy stocks have been among the most popular and talked about investments in recent years, thanks to low interest rates, government subsidies, and strong demand from consumers and investors who want to support a greener future. However, valuations of these stocks became very expensive, reflecting their current leadership rather than their future potential. In this article, we will explain why we have been cautious about investing in renewable energy stocks and where we see better opportunities in the energy sector. |

22 Nov 2023 - Performance Report: Digital Asset Fund (Digital Opportunities Class)

[Current Manager Report if available]