NEWS

12 Dec 2023 - The real risk of wildfires to US infrastructure investors

|

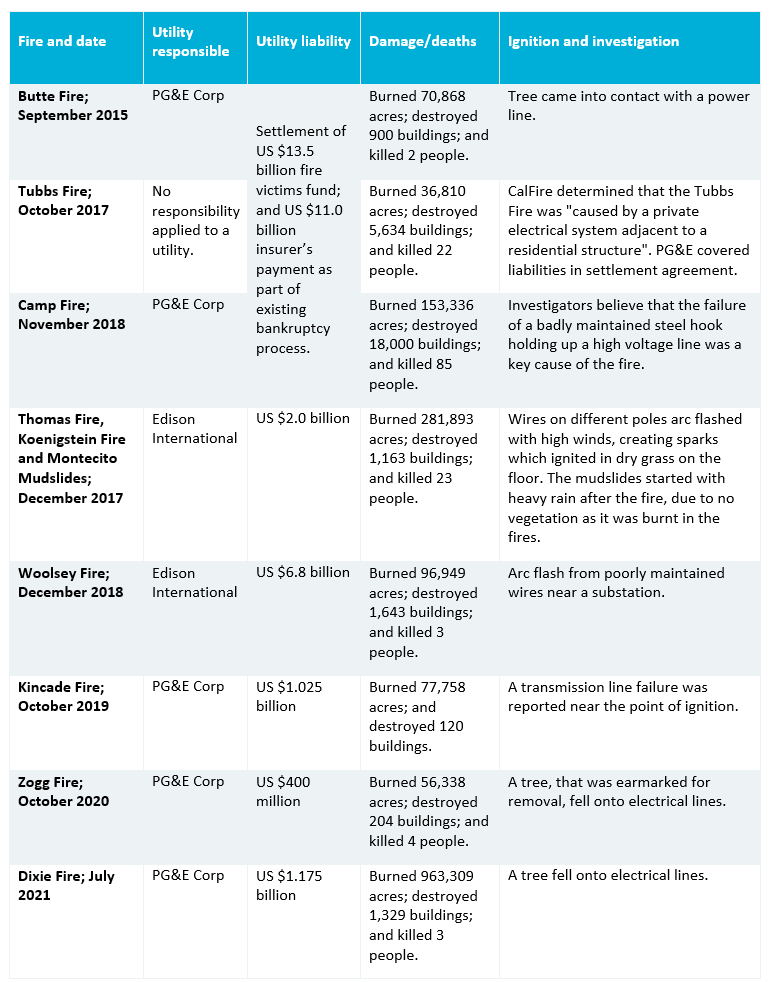

The real risk of wildfires to US infrastructure investors 4D Infrastructure November 2023 This article focuses on wildfires in the US, and their impact on utility companies in our universe. Five of the ten most destructive US wildfires since records began in the mid-to-late 1800s have occurred since 2013[1]. Climate change driven by human intervention has, through attribution analysis, been proven to be a key contributor to the increased frequency and ferocity of fires in the US. These fires are a real risk for utility companies and their investors, and with global temperatures continuing to rise, it seems the issue could intensify going forward. In our recent Global Matters article, Extreme weather risks and their impact on investors, we outlined the observed link between extreme weather events and climate change globally. Here, we'll focus specifically on wildfires and their impact on US utilities. Wildfire ignitionsWildfires are somewhat unique compared to extreme weather events - even though conditions are exacerbated by global warming, wildfire ignition is usually started by lightning strikes, human intervention (accident, negligence or intent), or electric utility equipment. There have been numerous examples in the US where electric utility company assets have ignited wildfires, which have gone on to cause significant third-party damage. The utility therefore faced billions of dollars in litigation liabilities, well in excess of their insurance protection. This has resulted in significant financial losses, cash liability payments, and increased probability of corporate financial distress, which itself has social ramifications. It started in CaliforniaThe detrimental shareholder impact of wildfire liabilities experienced by Californian utilities is well known. PG&E Corp (PCG-US) and Edison International (EIX-US) were most negatively affected by wildfires ignited by company assets over the period 2017-2021. Courts in California have adopted a unique application of the legal concept, inverse condemnation. It applies legal liability on electric utilities for all third-party damages caused by a fire which the utility's assets are found to have ignited. The courts' application of inverse condemnation removes the legal requirement to prove negligence on behalf of the utility in order to enforce third-party liabilities, which is required in other states. The courts have assumed the utility will recover these third-party property damages from customer bills, but the Californian utility regulator has been reticent to allow this. A number of fires were found to be ignited by utility assets in the state, incurring significant third-party property damages, as well as civil, regulatory and criminal penalties.

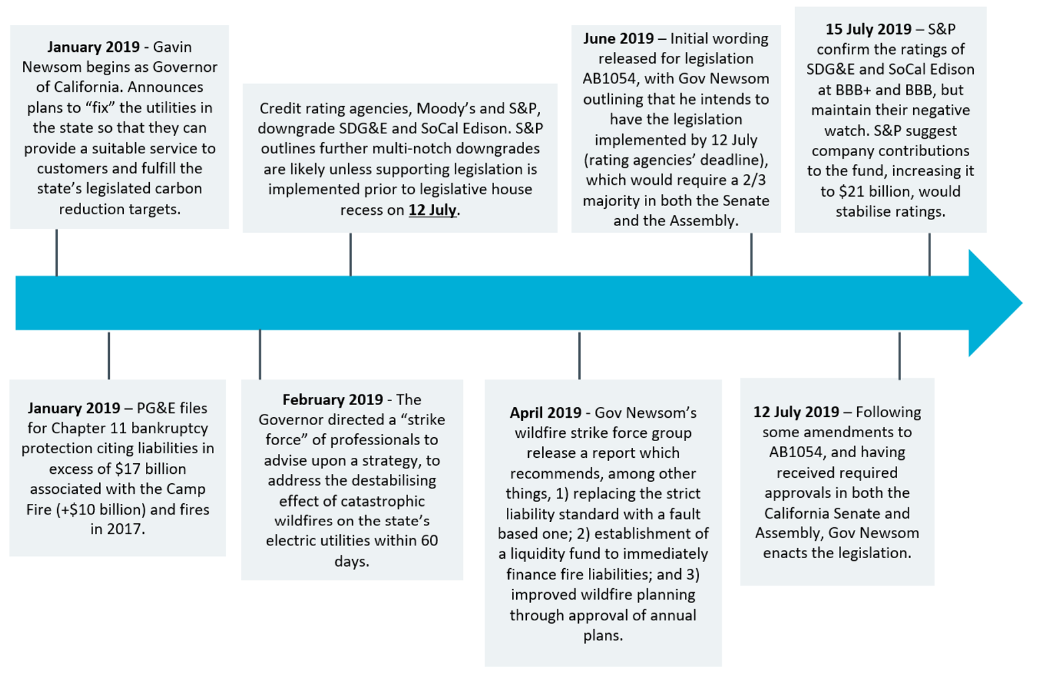

Source: California Board of Forestry and Fire Protection (CAL Fire) PG&E filed for bankruptcy protection in January 2019, due to the quantum of liabilities facing the company at the time. This process rendered the remaining equity value in the company zero. As part of PG&E coming out of bankruptcy, the company negotiated with legal representatives of uninsured wildfire victims and insurance companies of the Butte, Tubbs and Camp Fires to make payment of $24.5 billion (partially through an established fund) for property damages. However, it became clear that the situation for the utilities in the state was untenable. In 2019, Governor Newsom began his gubernatorial tenor in California. He identified wildfire risk as a key risk to the state, and understood that properly functioning and sustainably financed utilities were needed to deliver the energy prerogatives of California. He went about establishing a framework to mitigate wildfire liabilities for utilities which are prudently operated, in order to improve their credit assessment and ability to finance themselves. The below timetable summarises legislative steps taken, and the corresponding credit rating agency response.

Legislation SB 1054 not only established a wildfire liquidity fund which would finance wildfire legal liabilities sustained by the utilities, but it also established a process of ensuring that the utilities were prudently operating their electricity assets and were taking reasonable steps to mitigate the ignition of wildfires. If classified as a prudent operator under an annual certification, the utility can recover any fire liabilities in customer bills or from the established liquidity fund. Since 2018/19, companies have significantly reviewed their operational management of fires, and invested billions of dollars in 'hardening' their networks to avoid future fires. Key initiatives include:

The major electric utilities in California experienced significant share price corrections associated with the wildfires, and only recently have started to recover. The market seems to appreciate steps taken by the companies and state legislators in mitigating future fires, combined with the liquidity fund and pre-prudency test in avoiding future legal liabilities when fires do occur. But recent developments suggest wildfire risk is not specific to California... More recent experiences of wildfire riskInvestors thought that debilitating financial damages from wildfire risk was limited to Californian utilities because of the state's unique application of inverse condemnation. The requirement in other states, to prove utilities have acted negligently, was perceived as a mitigant against them incurring similar legal liabilities, unless negligent. That view may be changing. PacifiCorp litigationIn June 2023, unlisted electric utility, PacifiCorp, received an Oregon court decision relating to its alleged involvement in five major fires which burned across the state in October 2020. The fires burnt 850,000 acres of land, causing damage to around 4,000 homes, and killing at least 11 people[2]. Despite PacifiCorp not having been found responsible for ignition of the fires by any formal body at the time of writing, a jury court made a number of decisions including:

The jury found PacifiCorp negligent in failing to shut-off power to its 600,000 customers during a windstorm, despite warnings from officials. The company did not have any established power shut-off process, and argued the ramifications of cutting power would have broader and serious ramifications. The decision that PacifiCorp was liable for the fires also means that the company is likely to incur further actual and punitive damages associated with approximately 2,500 householders under a separate class action lawsuit. A very basic assessment suggests PacifiCorp could be liable for billions of dollars associated with this class action lawsuit. There is a clear risk of financial distress for the company. Maui fires of 2023The Maui fires that started on 8 August 2023 destroyed more than 2,700 structures, and killed 97 people, with 31 unaccounted for as of 18 September 2023. An investigation is ongoing into the cause of the fire, but Maui County has already filed a lawsuit against a subsidiary of the utility company, Hawaiian Electric Industries (HE-US), based on suspicions that the fire was ignited by the utility equipment (uninsulated wire contacted dry grassland when strong winds downed a wooden power pole). Hawaiian Electric has suggested that the lawsuit is imprudent in pre-empting the outcome of the formal investigation into causation. The share price of HEI fell from the closing price of $37.36 on 7 August, to $12.85 as at 17 October 2023 (a 65% decrease) based on legal risk associated with the fire. There is conjecture as to the prudent operation of the network on behalf of Hawaiian Electric, but the findings in the PacifiCorp case clearly show a high legal risk being faced by the company. Other exposed companiesA number of other companies are also exposed to wildfire risk in the US including:

4D's approach to mitigating the riskThere is no doubt that the environmental conditions for wildfires are being exacerbated by climate change. In doing nothing, utilities will be at greater risk of wildfire liabilities (physical and legal) as global temperatures increase. Many utilities are enhancing their operational preparedness and investing in 'hardening' the network to mitigate the risk of fire ignition. Governments and fire authorities are also focused on reducing the fuel for fires, being able to respond effectively to fires after ignition, and protecting prudently operated utilities from legal liabilities. At 4D, we undertake significant due diligence to understand utilities' operational preparedness and investment plans in hardening their networks against wildfires. We also keep abreast of legal and regulatory developments in utility operating jurisdictions to ensure the companies aren't exposed to risks that they cannot mitigate through prudent operation of their networks. This due diligence flows through our capex modelling and values, as well as our quality assessment of the utilities' jurisdiction, asset quality and management. We will exit a position, or rule a stock uninvestable, if there is a real risk of unquantifiable liability. |

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged), 4D Emerging Markets Infrastructure Fund For more information about 4D Infrastructure, visit https://www.4dinfra.com/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. [1] https://earth.org/worst-wildfires-in-us-history/ |

11 Dec 2023 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

11 Dec 2023 - Performance Report: Delft Partners Global High Conviction Strategy

[Current Manager Report if available]

11 Dec 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||

| DNR Capital Australian Equities Income Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

||||||||||||||||||||

| Perpetual Diversified Income Fund - Class A | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| Perpetual Dynamic Fixed Income Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| Perpetual High Grade Floating Rate Fund - Class R | ||||||||||||||||||||

|

||||||||||||||||||||

| Perpetual Income Share Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

| Perpetual Diversified Growth Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

||||||||||||||||||||

| Prime Value Enhanced Income Fund | ||||||||||||||||||||

|

||||||||||||||||||||

| View Profile | ||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||

|

Subscribe for full access to these funds and over 750 others |

8 Dec 2023 - Hedge Clippings | 08 December 2023

|

|

|

|

Hedge Clippings | 08 December 2023 There may have been a change at the head of the Reserve Bank board table, but whoever writes the Governor's statement and media release following the meeting is stuck in a groove. Apart from the absence of Philip Lowe's favourite "narrow path" term, the perils of inflation and the necessity to curb it are pretty much a copy and paste from prior months, which we suppose is inevitable. News & Insights New Funds on FundMonitors.com Investment Insights: The ups, the downs, and the future of the economic cycle | Touchstone Asset Management The weight loss drug shaping-up as a gamechanger | Magellan Asset Management November 2023 Performance News Argonaut Natural Resources Fund Bennelong Australian Equities Fund Delft Partners Global High Conviction Strategy |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

8 Dec 2023 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

8 Dec 2023 - Performance Report: Rixon Income Fund

[Current Manager Report if available]

8 Dec 2023 - The weight loss drug shaping-up as a gamechanger

|

The weight loss drug shaping-up as a gamechanger Magellan Asset Management November 2023 |

|

The world is awash with news that a drug designed to treat type 2 diabetes has also been approved to help achieve weight loss. Glucagon-like peptide 1 -- or GLP-1 -- is considered by some as a wonder drug and a new weapon in the public health battle against obesity. But what are the wider implications for the investment world? In this episode of Magellan In The Know, Portfolio Manager Nikki Thomas is joined by three Magellan Investment Analysts: Emma Henderson, Wilson Nghe and Tracey Wahlberg. Together they discuss the investment landscape surrounding GLP-1, looking at the pitfalls and potential financial benefits for sectors from healthcare, food retailing and restaurants to fashion, exploring which parts of the consumption landscape could be winners or losers. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

7 Dec 2023 - Performance Report: Argonaut Natural Resources Fund

[Current Manager Report if available]

7 Dec 2023 - Why are property prices surging as rates are rising?

|

Why are property prices surging as rates are rising? Montgomery Investment Management November 2023 In the thriving metropolises of Australia, the real estate horizon is gleaming brighter than ever. House prices have surpassed previous highs, putting a final nail in the coffin of those pessimistic forecasters who predicted 25-30 per cent declines. The latest figures show a surprising twist in Australia's property market, as the largest and costliest city shatters its previous real estate records. Across the nation, we're seeing a similar trend, with the PropTrack home price index indicating a national median home value increase of 0.36 per cent in October, achieving a new high. Sydney, once the face of declining values due to higher interest rates, has made a dramatic comeback. Home prices in the city are at an all-time high, with the median dwelling value reaching $1.07 million, marking a steady 11-month rise and a commendable annual rise of about 7.5 per cent. Other capitals like Brisbane, Perth, and Adelaide have also hit record values, defying earlier expectations. Even as interest rates have climbed, these cities have witnessed robust growth, thanks to a mix of factors, including renewed migration, a limited supply of stock and tight rental markets. Though Melbourne's and Hobart's prices are yet to surpass their previous highs, they're on an upward trajectory, while Perth boasts the most vigorous annual price surge, and Adelaide impressive growth year-on-year. Brisbane shares the spotlight with Sydney, with home values at all-time highs. A month ago, in a blog post entitled Don't Sell! House Prices Must Go Up, I wrote; "At the same time the population is surging (thanks to government policy), a downturn in housing construction has gripped the country. Australia is witnessing a steep decline in new home sales, and ...the Housing Industry Association was recently reported to be predicting a slump in construction activity by 2024, intensifying existing housing shortages and making homeownership unattainable for many Australians." One month in since that blog was written, and prices are fast reflecting those circumstances. And while there's no shortage of real estate agents willing to predict what property prices will do next, you can put them all away. A year 11 business studies student can tell you property prices have to rise, or at least remain elevated if they have already risen. And that's because when demand rises (immigration) and supply falls (construction has slumped) prices can only go one way. So, what's ahead for home prices? While the threat of inflation could prompt further rate rises, the ongoing housing shortage is likely to offset keeping property prices resilient. In essence, the sustained rise in property values across most of Australia's cities prompts a reflection: were the property bears too quick to predict doom? Current trends suggest they might have underestimated the market's resilience. Author: Roger Montgomery Funds operated by this manager: Montgomery (Private) Fund, Montgomery Small Companies Fund, The Montgomery Fund |