NEWS

A few charts from our Micro Caps CY2024 Overview

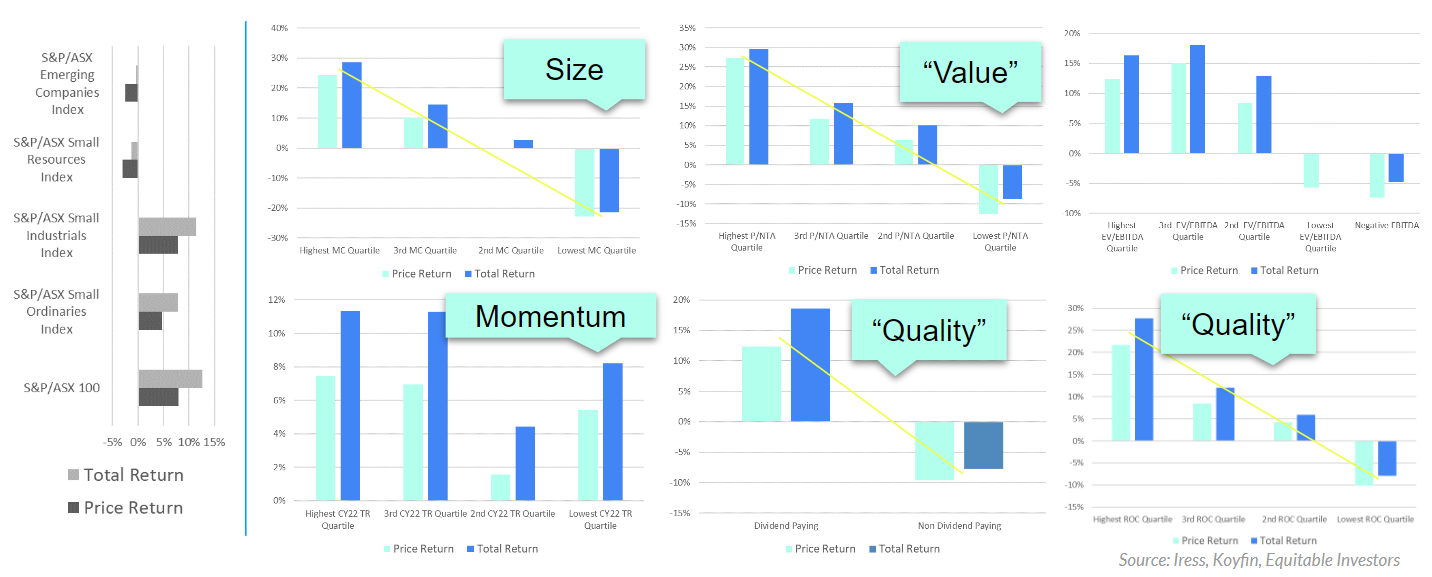

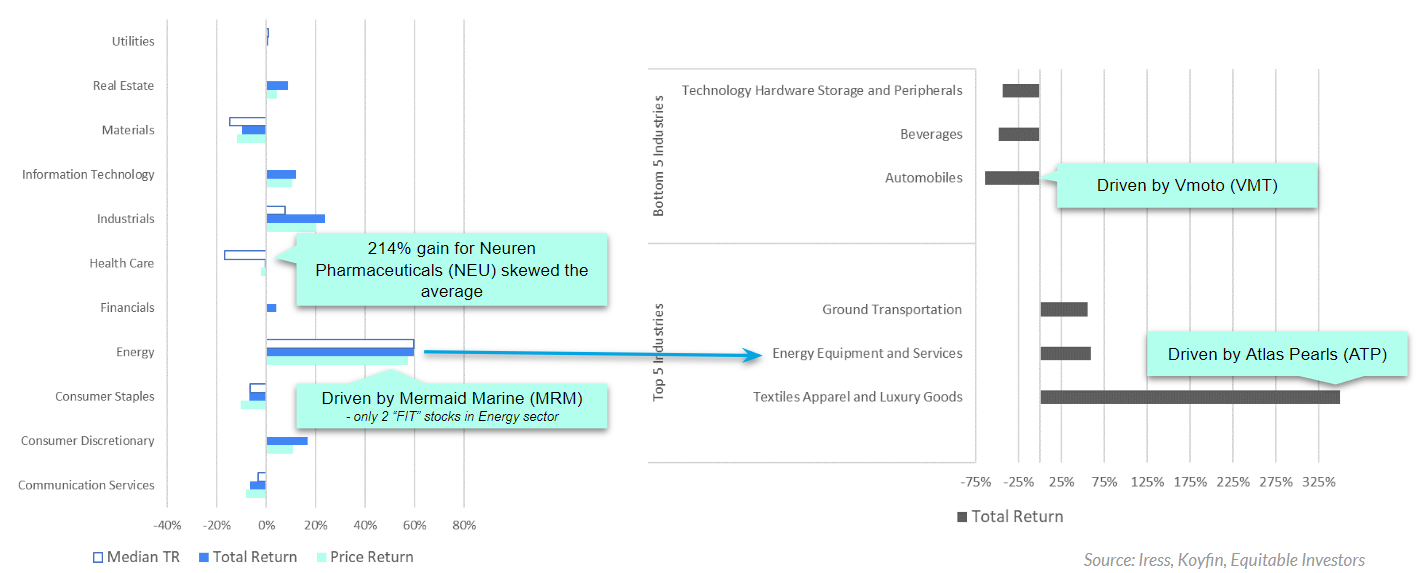

Stocks on higher multiples did better than those in "value" territory as investors chased "quality" (if you define that as top quartile return on capital or companies paying dividends) but the most clear cut divide in ASX listings in...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +1.25% in January. Since inception in February 2009, the fund has returned +13.43% per annum, an outperformance of +3.56% relative to the ASX 200 Total Return benchmark which has...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +1.79% in January. Since inception in January 2013, the fund has returned +12.74% per annum, an outperformance of +3.71% relative to the ASX 200 Total Return benchmark which has returned +9.03% on an...

Read more...

Performance Report: Collins St Value Fund

The Collins St Value Fund has risen by +11.13% over the past 12 months, an outperformance of +4.04% compared with the ASX 200 Total Return benchmark which has returned +7.09%. Since inception in February 2016, the fund has returned +14.04%...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +1.88% in January. Since inception in June 2018, the fund has returned +11.04% per annum, an outperformance of +2.54% relative to the ASX 200 Total Return benchmark which has returned +8.5% on an...

Read more...

Investment Perspectives: Global real estate - the outlook and themes for 2024

In the aftermath of a volatile macroeconomic year, this article delves into the global real estate outlook for 2024, highlighting some interesting themes across senior housing, retail, industrial, Japan and data centres.

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund rose by +1.73% in January, outperforming the ASX 200 Total Return benchmark by +0.54%. Since inception in February 2002, the fund has returned +12.28% per annum, an outperformance of +4.11% relative to...

Read more...

Performance Report: Quay Global Real Estate Fund (Unhedged)

The Quay Global Real Estate Fund (Unhedged) returned -0.84% in January, outperforming the FTSE EPRA/ NAREIT Developed NET TR benchmark by +0.08%. Since inception in January 2016, the fund has returned +6.7% per annum, an outperformance of...

Read more...

New Funds on Fundmonitors.com

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research,...

Read more...

Hedge Clippings | 09 February 2024

Last week's Hedge Clippings didn't linger too long on the potential outcome of Tuesday's RBA Board meeting - the first to be held under the new two-day format - so it wasn't difficult to forecast "there's little chance of a rate rise when...

Read more...