NEWS

27 Feb 2024 - Australian Secure Capital Fund - Market Update

|

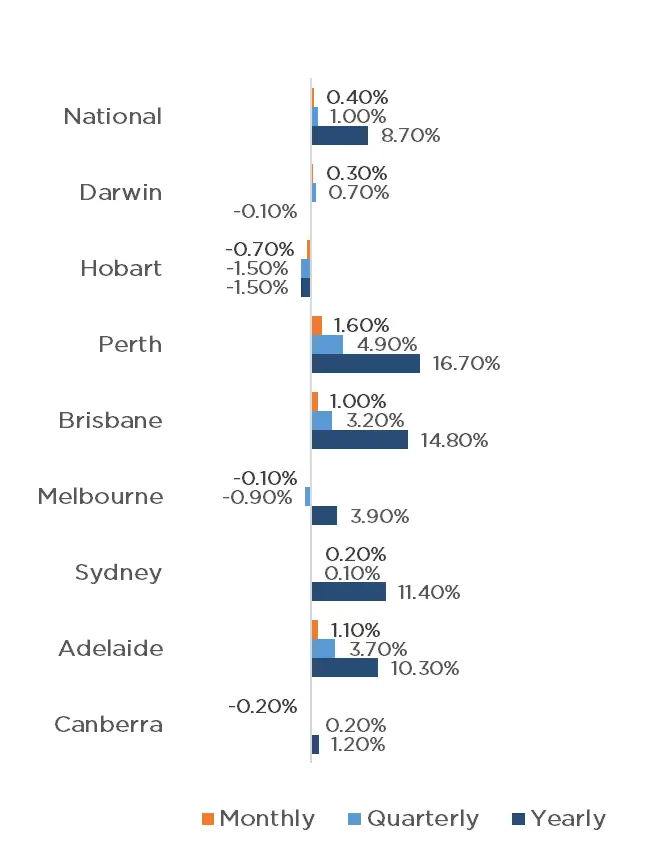

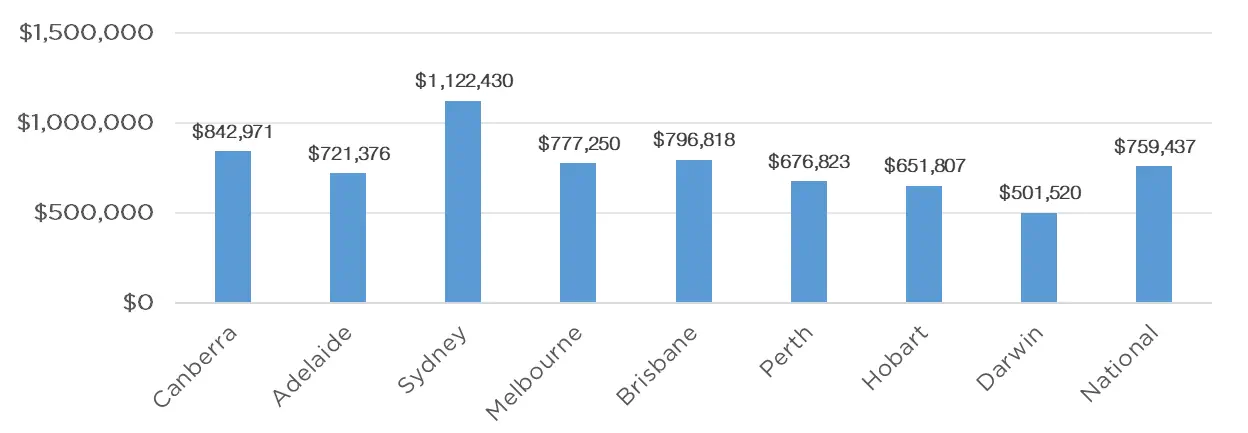

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund February 2024 The first RBA meeting of the year has taken place, with the cash rate remaining on hold at 4.35%. Recent inflation data has given economists confidence that we have reached the end of the rate hike cycle. The first weekend of February brought the start of the 2024 auction season, with a mammoth 1,671 auctions being held across the combined capitals. This is the second largest opening weekend since 2008, with only the corresponding weekend in 2022 holding more auctions, with 1,779 taking place. This result was up 26.4% on 2023 data, and was more than double than double the number of auctions held over the year so far (803). Melbourne recorded the most auctions for the weekend, with 603 taking place, followed closely by Sydney with 562. Brisbane, Adelaide and Canberra also recorded triple digit auction numbers with 203, 159 and 132 auctions taking place respectively, whilst Perth and Tasmania held just 9 and 3 auctions respectively. Preliminary clearance rates have also begun the season strongly, with a clearance rate of 73.9% across the combined capital cities, well above the 61.9% of 2023. Canberra led the way with 80.0%, followed by Adelaide, Sydney and Melbourne with 77.6%, 76.3% and 71.9% respectively. Brisbane being the only capital below 70% with a 68.5% result. The property market continues to show growth, albeit signs of cooling do exist, with a 0.4% increase across both the combined capitals and regionals. Perth continues to experience the highest rate of growth, increasing by 1.6% for January, followed by Adelaide and Brisbane with 1.1% and 1% respectively. Darwin and Sydney also experienced growth of 0.3% and 0.2% respectively, whilst prices in Melbourne, Canberra and Hobart have fallen by 0.1%, 0.2% and 0.7% respectively. The annual change remains significant with a 10% increase across the combined capitals, and 4.9% increase for regional centers, contributing to a national increase of 8.70%. This has been driven by four of the capitals experiencing double figure growth with 16.70% for Perth, 14.80% for Brisbane, 11.40% for Sydney and 10.30% for Adelaide. Melbourne and Canberra also recorded growth for the year with 3.90% and 1.20% whilst only Darwin and Hobart saw prices fall for the year with 0.1% and 0.4% respectively. This has led to Brisbane now holding the second highest median value in the country, overtaking Melbourne with a median value of $796,818 compared to Melbourne's $777,250. Whilst the property market has begun to show signs of easing, given that economists predict we are at the end of the rate hike cycle, we anticipate that property prices will still experience growth throughout 2024, as interest rates begin to subside, and the lack of housing supply continues. Clearance Rates & Auctions week of 4th of February 2024

Property Values as at 1st of February 2024

Median Dwelling Values as at 1st of February 2024

Quick InsightsWill Values Fall? Unlikely.With home values in capitals such as Sydney still 2.4% lower than their peaks, many investors such as Sydney-based investor Nicholas Marangos-Gilks are more motivated than ever to increase demand in the market. Buyers are not waiting for the rate cut to occur. Tim Lawless, CoreLogic research director, has commented, "We are still seeing housing values below their record highs in Sydney, Melbourne, Hobart, Darwin and the ACT. In these cities we could see motivation from buyers looking to get into the market while values are still below their peaks." Source: Australian Financial Review Looser Planning, not Restrictive TaxesEliminating negative gearing and ditching capital gains tax discounts will not solve the worsening housing affordability crisis, but boosting supply by easing planning rules will, a new report says. Centre for Independent Studies chief economist and former Reserve Bank official Peter Tulip said restrictive planning rules have added more than 40% to house prices in Sydney and Melbourne, while property taxes boosted values by 4% at most. "There are arguments from the tax policy perspective that negative gearing and the capital gains discount should be considered, but it's not relevant to the question of housing affordibility," he said. Source: Australian Financial Review Author: Filippo Sciacca, Director - Investor Relations, Asset Management and Compliance Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

26 Feb 2024 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

26 Feb 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|||||||||||||||||||||

| Aura Core Income Fund | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

|

|

|||||||||||||||||||||

| JPMorgan Equity Premium Income Active ETF (Managed Fund) | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

| JPMorgan Equity Premium Income Active ETF (Managed Fund) (Hedged) | |||||||||||||||||||||

|

|||||||||||||||||||||

| JPMorgan US 100Q Equity Premium Income Active ETF (Managed Fund) | |||||||||||||||||||||

|

|||||||||||||||||||||

| JPMorgan US 100Q Equity Premium Income Active ETF (Managed Fund) (Hedged) | |||||||||||||||||||||

|

|||||||||||||||||||||

| View Profile | |||||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

24 Feb 2024 - Hedge Clippings | 23 February 2024

|

|

|

|

Hedge Clippings | 23 February 2024 This week for a change, Hedge Clippings is going to ignore the Reserve Bank, inflation, interest rates, and even politics, as Barnaby's retired to the bush, and Donald Trump has seemingly even gone quiet as he considers his next legal option. Instead, we're reverting to our bread and butter, the performance of markets and managed funds. It's been just over 3 months since the extraordinary rally in equities kicked off last November. At the end of October last year, the ASX200 Absolute Return Index (ARI) was negative (just) YTD since January 2023, and up only 2.95% over 12 months. By the end of December, the index was up 12.4%. Things did slow down somewhat in January, with a return of 1.19%, by which time the 12 month rolling return had fallen to 7.08% thanks to its performance in January 2023 "falling off" the 12 month's numbers. In the small cap sector, the numbers were even more extreme as risk appetite among investors, plus limited liquidity in most stocks in the sector took a toll. At the end of October '23, the ASX Small Ordinaries ARI was down 6.05% YTD, and -5.11% over 12 months. By the end of December, it had risen over 14% to finish the year up 7.82%, before dipping to a 12 month number of +2.09% by the end of January. Small caps of course are notoriously volatile: In September 2022 the index was down 22% over 12 months, but a year earlier, September 2021, the index was up 30.4%, having risen no less than 52% in the 12 months to March '21 in an amazing rebound from the initial depths of COVID in March 2020 of -21% over 12 months. Experienced investors and advisors will correctly point out that when investing in the market, and managed funds in particular, it's the long (term) game that counts. Most offer documents (and ASIC) suggest a 5-7 year term to ride out the swings and roundabouts. Taking that approach, and the long term suggests an 8-9% annualised return (including dividends) from the Australian equity market and 10-12% from global equities based on the MSCI All Countries World Index. Over the same 5-7 year period, managed funds in AFM's Equity Peer Groups - both Large and Small/Mid Cap - have on average largely provided the same returns after fees as the index: The issue of course is volatility, or standard deviation of returns, but as shown below, so is the concept of average. Many will correctly point to the fact that individual stocks and fund's performance varies dramatically and with careful selection, performance can far exceed the above (although passive investing in an index ETF doesn't provide this, but that's a discussion for another day). Of course equities aren't the only game in town, particularly in volatile markets. Over the past 2-3 years, Private & Hybrid Credit funds have proven that they can return the same as equities (8-10% plus) with a fraction (or none) of the volatility, plus a regular income stream paid monthly or quarterly. We're currently preparing our Fixed Income Private Credit Sector Review to shine a light on this emerging, and increasingly popular sector which features a surprisingly diverse range of strategies and underlying assets. News & Insights New Funds on FundMonitors.com Market Commentary - January | Glenmore Asset Management Stock Story: Charter Hall | Airlie Funds Management January 2024 Performance News Glenmore Australian Equities Fund Insync Global Capital Aware Fund Bennelong Emerging Companies Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

23 Feb 2024 - Performance Report: Digital Asset Fund (Digital Opportunities Class)

[Current Manager Report if available]

23 Feb 2024 - It's quality time for Global Equities

|

It's quality time for Global Equities Yarra Capital Management January 2024 In times of change, new market leaders will emergeFinancial regulators like to say that past investment performance is not a clear indicator of future performance. Yet, we investors often look to the past to gain insights into potential future market conditions. There are patterns that can be exploited or traps that may be avoided. However, as we head into 2024, the past may not offer the usual useful insights. From a macro perspective, central banks' experimentation with quantitative easing―which provided relatively benign market conditions since the Global Financial Crisis--is being unwound, and this "quantitative tightening" presents a new territory for policymakers and investors. Simultaneously, we appear to be approaching a peak in monetary tightening, and inflation appears to be in retreat, but the end game for this battle remains opaque. Recent market actions suggest a turning point is approaching, yet when it comes to timing key events, markets can often be wrong. Geopolitics also offers few signs of stability. The peace dividend that has prevailed for several decades has abruptly ended, with ongoing developments in the Middle East being the latest addition to broader uncertainty. In addition, a series of national elections in 2024--culminating with a possible second presidential term for Donald Trump in the US--will ensure further drama unfolds. With all of this in mind, investors will need to adjust their expectations, and portfolios, to account for higher for longer interest rates, the challenges of slower economic growth, stickier inflation, and a testing geopolitical environment. So, in this sea of uncertainty, where can we find a stable port in which to anchor with confidence? For us, we stand by our philosophy of Future Quality--the belief that companies which can grow, attain and sustain superior returns on invested capital, and have all the key quality pillars in place (Franchise, Management, Balance sheet and Valuation), will be the best candidates for capturing longer-term alpha. While each company will embark on its own, unique journey to Future Quality, there are also common pathways, often driven by structural requirements. Therefore, these companies are less dependent on macro cycles, which we can leverage over the long term. These include the following: AI AdoptionThe emergence of artificial intelligence (AI) was a dominant market force in 2023. We were initially hesitant about joining this party, but our subsequent research has led us to reappraise this position. While we still believe AI contains an element of hype, it has the potential to transform technology for the next generation. It is too early to define the longterm winners from the new business models and use cases being inspired by AI, but there are market leaders already benefitting from the rapid adoption of this new technology that fit our Future Quality criteria. Over recent months, we have added Synopsys, Nvidia, and Meta to the portfolio. Enablers of the energy transitionThere is a need to reduce humankind's reliance on fossil fuels and create cleaner alternatives through renewable sources of energy, but this transition is not straightforward. Increased spending is needed to sustain existing energy production at the same time as mitigating carbon missions. While there is a fruitful pool of investment opportunities on both sides of this equation, the transition is heavily reliant on fiscal spending and political support could prove to be fickle. Portfolio winners in this space have been Schneider, Linde and Chart Industries (sold in Q3 2023). Normalisation and structural growth in global travelThe travel industry is still in the process of recovering from pandemic-imposed restrictions, with countries at differing stages of normalisation. Yet, when you look at the core consumers of travel, demand remains robust. This is particularly true for younger generations, who place greater value on "experiences". Furthermore, a new travel cohort is emerging from developing countries where rising gross domestic product per capita means more people will be able to afford to travel in the future. Booking Holdings, Amadeus and Samsonite have been positive contributors to the portfolio in 2023. Providers and enablers of healthcare efficiencyWith an ageing population, providing sufficient and efficient healthcare, as well as reducing the cost of such services, will be one of the world's most important challenges going forward. In our view, this demographic test will--and has been--a great hunting ground for investment ideas as healthcare companies innovate to deliver much-needed solutions. That said, some subindustries within the healthcare sector have underperformed of late because of the pandemic pulling demand forward and creating ongoing staff shortages. We are heading into a changing world, where the more recent past can no longer be relied on to guide our path forward. There are tools we can use to provide a greater degree of certainty. Our Future Quality approach is designed to help us identify franchises that are set to endure. Some of these companies may not have been in the vanguard of market leadership over the last decade. However, in this instance, we can more reliably believe history when it tells us that in times of change, the market leaders at the start are rarely the same as the ones leading us out of it. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

22 Feb 2024 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

22 Feb 2024 - Small is beautiful

|

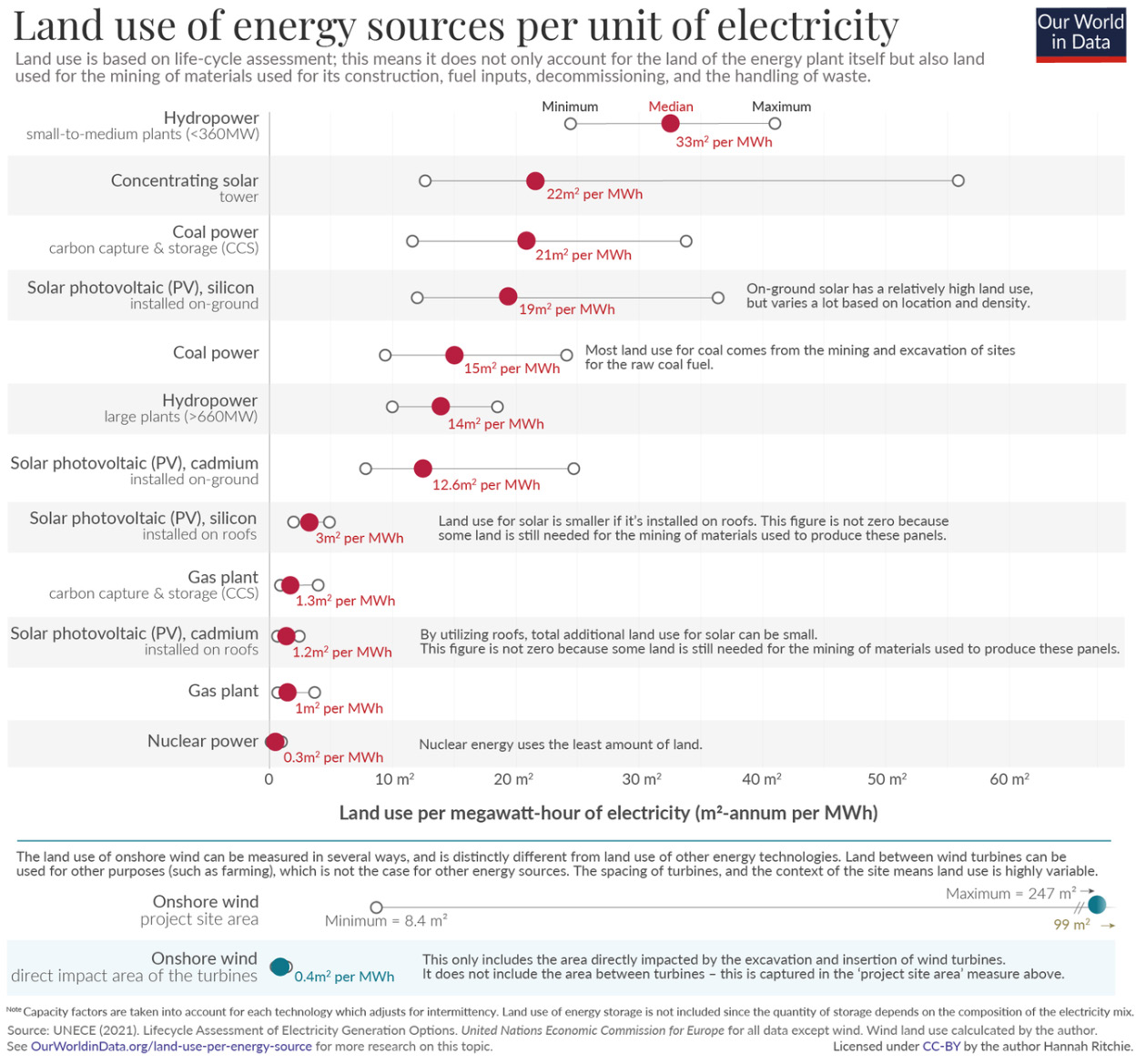

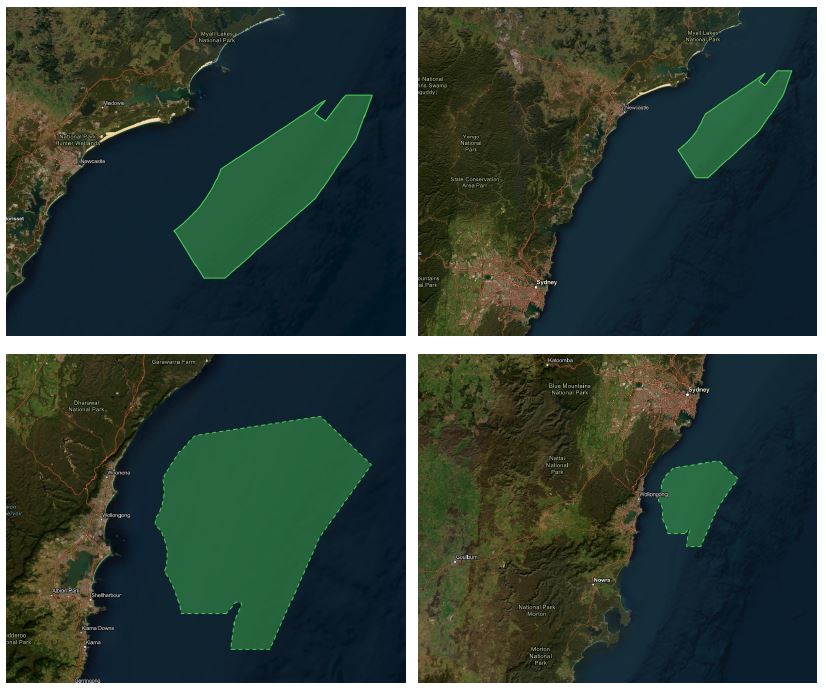

Small is beautiful Eiger Capital January 2024 As we summarized in our September quarter note, there was a time post the Fukushima disaster when it appeared that nuclear energy was too risky and would be bypassed entirely in favour of renewables. Coal was to be phased out and wind and solar, as well as more marginal technologies like biomass, would increasingly play a central role in keeping the lights on. Zero carbon will eventually disrupt the transition fuels too (a polite term for gas) so that come 2050, the energy transition will be complete. This is a neat narrative but it's looking increasingly likely that the scale of the transition may just be too great to reach net zero in less than 30 years. After all, the global population continues to grow and there is a very strong correlation between population size and energy demand - we all require energy for life's basics and per capita consumption continues to rise. The inequalities of energy consumption apparently don't matter; wealthy countries with low population growth consume far more power per capita than poorer ones. We can either try to grow a bigger pie, or be fairer with the one we have, and if it's a bigger pie we need, then the scale of transition is extremely daunting. Excessive demand can lead to many problems, and we will need to walk a fine line between environmental preservation and deprivation. The Australian Broadcasting Corporation recently featured an article entitled, "How can we support the transitions to renewables without further damaging the environment?", which highlighted the 'dark side' of the rush to electrification - pollution and degradation. An example is the controversy surrounding the Upper Burdekin Wind Farm in Queensland. Windlab, a company associated with Andrew Forrest and at one time had the support of Apple, has been criticized for the scale of land clearing and endangerment of several threatened species including koalas and rock wallabies. It's an odd circularity akin to that infamous line from the Vietnam War era, "we had to destroy that village in order to save it". Where does nuclear fit in? Besides being a low-carbon source of power, it offers several other advantages over most other renewables: long life; high reliability/efficiency; competitive life-time cost; less intensive use of raw materials; and lower physical footprint. In this piece, we focus on the small footprint that nuclear power generates relative to other power sources. Coal has been a foundation for modern economies, providing 'safe', stable baseload power. Nuclear has the same ability and can do so in a uniquely small area for its potential. In an article published on OurWorldInData.org in 2022, author Hannah Ritchie detailed the relative land use intensity of different methods of power generation.1 The lifecycle assessment, i.e., complete land use including mining, found that nuclear power at 0.3m2/MWh is the most efficient form of power, including renewables (Figure 1). Onshore wind is almost as efficient at 0.4m2/MWh if only the land used by the windmill is counted and not the entire wind farm. This is because land in between windmills can have other uses, such as agricultural production or grazing. The total area needed can be very large and may require the clearing of vegetation, hence the large range. As the Burdekin project shows, this can disturb the natural state of a large area although it would be hard to argue that the land is completely sterilised. As turbines grow in size and technology advances, there is likely to be some improvement in m2/MWh though vary through a wide range. Figure 1: Relative efficiency of power generation relative to land use

Offshore wind offers several advantages over onshore installations, namely an ability to install larger and more efficient turbines, and land use ceases to be an issue (ex the need for raw materials). The limiting factors for offshore wind tend to centre on finding suitable wind resources, seabed condition, locations near population centres, visual impacts, access to fisheries and impediments to marine navigation and aircraft. There has been some controversy regarding the potential impact on whales, and while this issue has recently been a hot topic in the US, to date there is no evidence that connects offshore wind farms to the injury or death of whales. Nevertheless, these utilities are enormous, sprawling structures, where for example, the proposed Illawarra (4.2GW) and Hunter (5GW) projects offshore NSW cover areas of 1,461km2 and 1,854km2, respectively (Department of Climate Change, Energy, the Environment & Water, DCCEEW). To give some context, that is roughly the same size as Fraser Island (K'gari), the world's largest sand island. Another way to look at the scale is to consider that the Illawarra project would stretch over about 50km of the coast and the Hunter up to 90km, or a combined 6.5% of the state's coastline (Figure 2). The windmills themselves will be around 270m high and at 15MW each, around 600 would be needed to meet the stated capacity of the combined area. Figure 2: Proposed area for the Hunter (top) Illawarra (bottom) offshore wind projects

Solar PV's great advantage is that for the most part, it uses existing infrastructure (rooftops). The Australian PV Institute states that there are over 3.6m PV installations in Australia totalling more than 32.9GW of capacity with most systems between 6.5kW and 9.5kW, i.e., suburban roof tops. Our basic analysis indicates that the area used by all PV solar in the country is only about 146km2 and 2m2/MWh assuming a somewhat generous average of 400W panels and no secondary impacts from mining. On a life-cycle basis, Ritchie estimates that number to be 3m2/MWh for rooftops but 19m2/MWh for on-ground commercial facilities. On-ground commercial solar arrays don't piggyback on existing structures, so their land-use is real. Hence, they are amongst the least efficient forms of power generation in terms of their footprint. The largest proposed solar PV facility in Australia is Sun Cable in the Northern Territory. At 20GW, it would cover 120km2, almost as much area as all other PV installations in Australia, but be located on pastural leases used to graze cattle. Large as it is, Sun Cable is remote and is almost meaningless in a country the size of Australia. The area of installed solar PV in Australia is just one-tenth that of the Illawarra wind project yet has almost 8 times the installed capacity. Naturally there are other things to consider, such as the higher capacity factor of offshore wind (e.g., ability to generate at night) that make installed capacity an overly simplistic measure. Using average global capacity factors for offshore wind of 40% (35-45% range over 2010-2022) and 12% for rooftop solar in Australia (i.e., non-commercial), solar PV would still have 2 times the capacity of the Illawarra project - 4GW vs 2GW - for the same operational life. At the other end of the spectrum are hydro systems, mainly due to the mining footprint and the flooding of valleys for water storage. A slightly unusual system is solar that uses mirrors to concentrate solar energy on a tower to create heat. Land use is very intense, averaging 22m2/MWh, which suggest that these systems are somewhat extravagant and that better alternatives exist. Nuclear suffers from very few of the problems discussed above. Firstly, the raw size of the nuclear power plant itself is relatively small and the move to Small Modular Reactors should enhance this feature. A 1GW nuclear power plant covers approximately 3.5km2 while a coal plant of the same size is almost twice that. Neither can compete with gas, however, at 0.5km2. Pity about the CO2. There is a case to make that the sites of shuttered coal-fired power plants would make good sites for new nuclear ones in that grid infrastructure is in place and further land clearing is unnecessary. Secondly, the mining of uranium does not take much space relative to the output of a nuclear power plant and hence m2/MWh is miniscule. Land disturbance for coal mining is famously large and ash disposal contributes to land use. The scale of coal consumption depends on plant design, efficiency and the rated calorific value of the target fuel, so there is no rule of thumb. However, the World Coal Institute estimates that at 38% efficiency and 75% availability, a 1GW coal plant would burn 2.5Mtpa bituminous coal and 6.5Mtpa brown coal. Compare this to a nuclear power plant of the same size, which uses about 27tpa uranium, requiring perhaps 0.5Mlbs U308 and ore input of maybe 400ktpa depending on grade and recovery. Mining for silica, aluminium, copper and zinc contribute negatively to solar and wind. Thirdly, nuclear power plants are highly efficient, with plant availability of more than 90% over long life spans. These are key factors in life cycle analysis because they result in nuclear power plants producing many more TWh of power over time than other power plants, i.e., a bigger denominator. All this is underscored by the COP28 meeting held in the UAE at beginning of December, which again highlighted the role nuclear power could play in the drive to decarbonize. More than 20 countries signed a declaration to triple nuclear capacity by 2050. It included major economies such as the US, Japan, South Korea, France and the UK, though not Germany (nor Australia for that matter). This represents a stunning turnaround for the nuclear industry and is reflected in the surging uranium spot price, which is now US$87/lb. We continue to believe that nuclear energy will play an increasingly important role in providing the world with clean power and maintain significant positions in near-term uranium producers, Boss Energy and Paladin Energy. Author: David Haddad, Principal and Portfolio Manager Funds operated by this manager: |

21 Feb 2024 - Performance Report: Kardinia Long Short Fund

[Current Manager Report if available]

21 Feb 2024 - Stock Story: Charter Hall

|

Stock Story: Charter Hall Airlie Funds Management January 2024 |

|

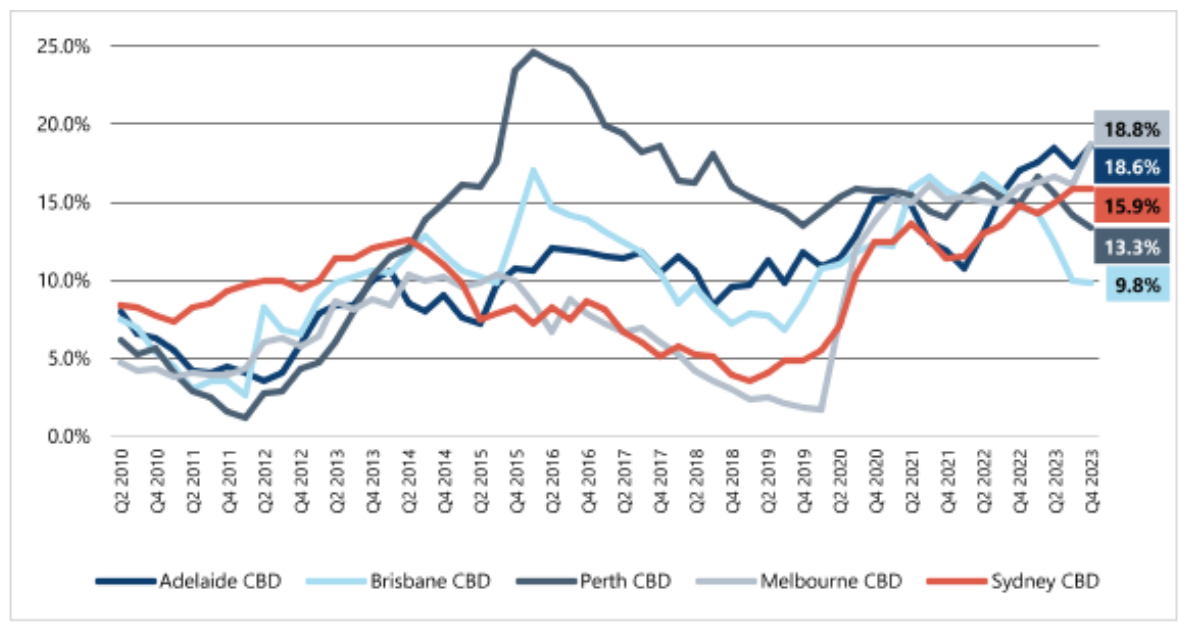

Underappreciated quality. Business Quality is a key factor in the Airlie investment process, and we typically define a high-quality business as one that can earn a decent return on its capital. The Real Estate Investment Trust (REIT) sector is not typically thought of as a high total return sector due to the low-yielding nature of real estate and high capital intensity to just 'stay in business'. That said, it may come as a surprise that CHC has delivered a total return of ~11.5% p.a. since its IPO in 2006. This performance has been driven largely by CHC's transition from a traditional REIT to a fund manager, which generates fees on client capital with minimal amounts of incremental investment required. Now, I know you are probably thinking, "Why would I want to invest in an office fund manager, particularly in the current interest rate environment?" We believe these risks are more than captured in CHC's current price and have provided the opportunity to invest in a high-quality business at an attractive valuation. But Office is Dead?We don't disagree that the 'Work From Home' trend has created meaningful challenges for the Office sector. Corporates have quite reasonably concluded they can achieve substantial rent savings while providing their workforce with increased flexibility. This has resulted in an increase in market vacancy and placed pressure on rents. Prime CBD Office Vacancy Rates

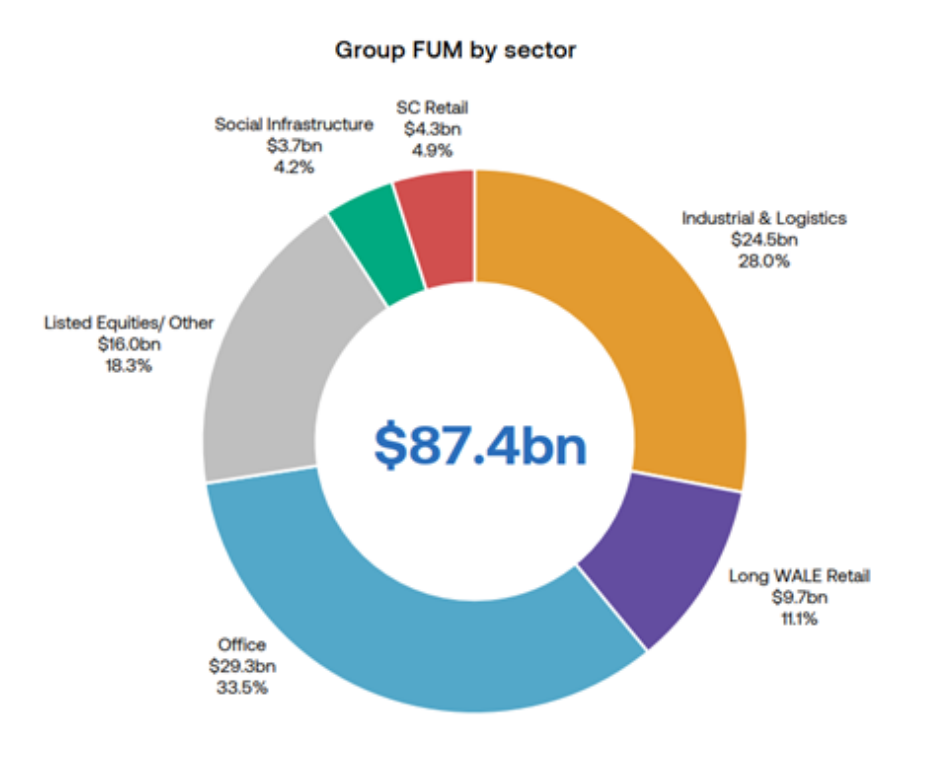

This has understandably weighed on Charter Hall, with the share price down 48% since its peak of $21.83 in 2021. While Charter Hall will undoubtedly be affected by weakness in Office, we believe the criticism is not entirely fair given roughly two-thirds of its Funds Under Management (FUM) is in 'non-office' sectors, including Industrial and Logistics (28%), Equities (18%), Retail (16%) and Social Infrastructure (4%).

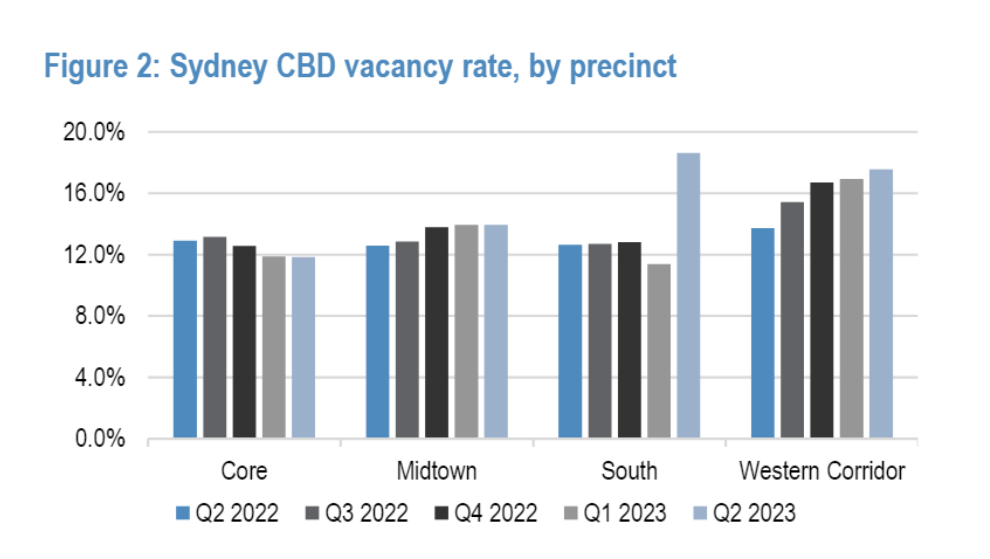

Further, the real estate cliché "location, location, location" remains as relevant as ever. The fundamentals for well-located, new and environmentally friendly buildings are markedly different from those that do not have these characteristics. The figure below highlights the divergent vacancy trends seen between core and non-core regions of Sydney CBD. Equally, the vacancy rate for buildings in Sydney that are less than 10 years old is ~6% versus ~13% for those over 10 years old (source: JLL and Charter Hall Research).

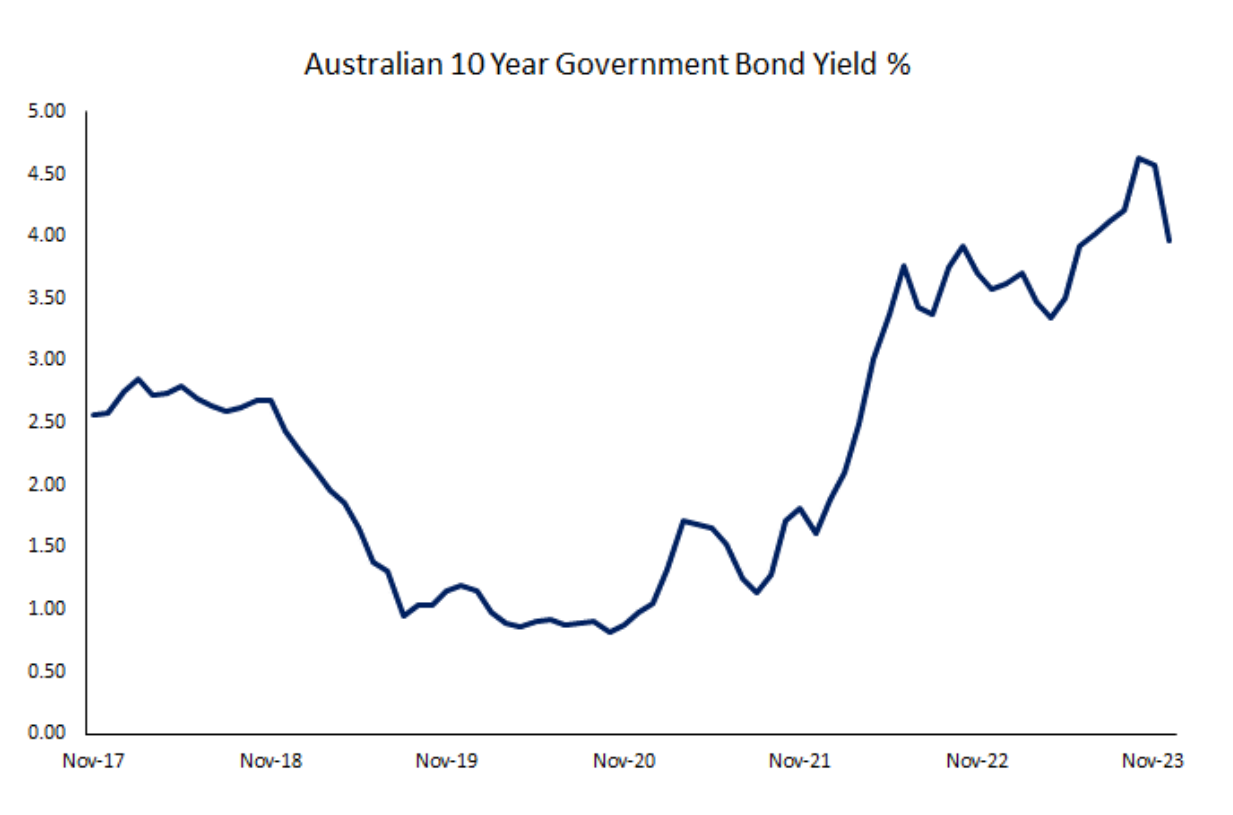

High Interest Rates?It wouldn't be an investor communication without a quote from Warren Buffett, who said, "Interest rates are to the prices of assets like gravity is to the function of earth". As such, it's no surprise that the 10 Year Australian Government Bond Yield rising from <1% during the pandemic to almost 5% weighed on an asset manager like CHC. Most obviously, it has reduced the value of the assets that it manages and charges fees on.

Second, the rapid increase in interest rates has frozen transaction activity in the sector with investors unwilling to make long-term, illiquid investments for fear the price of the asset could fall in the near term. This is not ideal for Charter Hall where transaction activity allows it to acquire new assets, increase its FUM and thereby grow earnings. While we don't claim to be economic forecasters, we'd argue that with interest rates at 10-year highs and inflation measures falling, it seems more likely than not that interest rates have peaked. We believe this peaking of interest rates is likely to see transaction activity begin to return and allow CHC to mitigate devaluations in its FUM. From FY19 - FY23 CHC added $5.7b per year to FUM from acquisitions and $2.0b p.a. from developments. Therefore, a return to average transaction and development activity would sufficiently offset a 10% decline in current Property FUM of $71b due to devaluations. Underappreciated Business QualityCHC trades at ~15x FY24 EPS guidance, which is a large discount to the ASX 200 of ~22x (excluding financials and resources) despite a track record of growing EPS at 15.1% p.a. over the last 10 years.

We believe CHC is a higher-quality business than it is given credit for, with several factors often overlooked:

Attractive ValuationDespite CHC's rising margins, decreasing capital requirements, proven earnings growth and business quality, it still trades at ~14x 1-year forward EPS which is well below the ASX 200 multiple of ~22x (excluding commodities and banks). Furthermore, we view the company's FY24 guidance of 75 cents per share as 'trough' earnings given it implies virtually no performance or transaction fees. If we normalise FY24 performance and transaction fees to a level that is in line with historical averages, CHC would be trading at ~10x FY24 EPS. We believe that if inflation continues to fall, interest rates stabilise and there is discussion of rate cuts - as we have seen in recent months - CHC's multiple should re-rate to account for the cyclically low earnings and depressed multiple. By Jack McNally, Investment Analyst Funds operated by this manager: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |