NEWS

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose by +6.54% in February, outperforming the All Countries World (AUD) benchmark by +1.22%. Over the past 12 months, the fund has risen by +33.93% compared with the benchmark which has returned...

Read more...

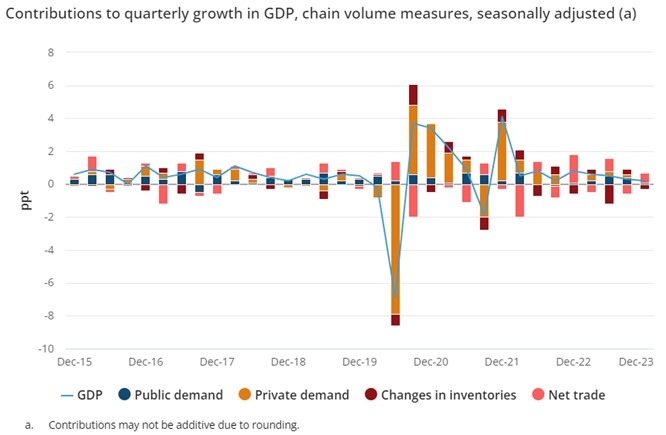

Tim Hext: What we learned from the latest GDP data

The December-quarter GDP numbers just stopped short of the "no-growth" scenario we were slowly sliding towards last year. Pendal's head of government bond strategies Tim Hext explains what it means for markets.

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +1.24% in February. Since inception in November 2009, the fund has returned +9.79% per annum, an outperformance of +1.74% relative to the ASX 200 Total Return benchmark which has...

Read more...

Performance Report: Delft Partners Global High Conviction Strategy

The Delft Partners Global High Conviction Strategy rose by +5.14% in February. Since inception in August 2011, the strategy has returned +14.99% per annum, an outperformance of +1.58% relative to the All Countries World (AUD) benchmark...

Read more...

Glenmore Asset Management - Market Commentary

Globally equity markets performed strongly in February. In the US, the S&P 500 was up +5.2%, the Nasdaq increased +6.1%, whilst in the UK, the FTSE 100 was flat.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +2.48% in February, outperforming the ASX 200 Total Return benchmark by +1.69%. Since inception in June 2017, the fund has returned +19.35% per annum, an outperformance of +10.66% relative to...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +2.71% in February, outperforming the ASX 200 Total Return benchmark by +1.92%. Since inception in January 2013, the fund has returned +12.91% per annum, an outperformance of +3.87% relative to the...

Read more...

New Funds on Fundmonitors.com

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research,...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +6.34% in February, outperforming the ASX 200 Total Return benchmark by +5.55%. Since inception in November 2017, the fund has returned +18.28% per annum, an outperformance of +9.82% relative...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +1.6% in February. Since inception in June 2018, the fund has returned +11.18% per annum, an outperformance of +2.66% relative to the ASX 200 Total Return benchmark which has returned +8.52% on an...

Read more...