NEWS

27 Mar 2024 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

27 Mar 2024 - How to Handle a Correction

|

How to Handle a Correction Marcus Today March 2024 |

|

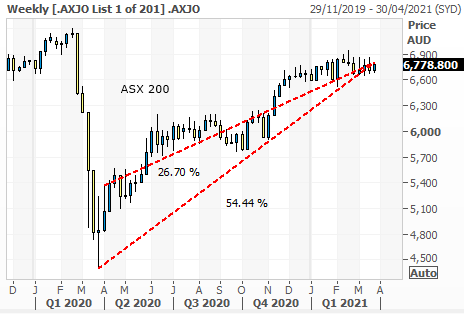

It has been one year since the bottom of the market on March 23, 2020. Since then, the ASX 200 is up 65.5%... if you bought at the absolute low and sold a year later.

For any fund manager getting abused for not achieving 54.44% in the post-pandemic recovery year, you might point out to your complaining client that the 54.44% was from the lowest low, which existed for a micro-instant on March 23rd 2020 in the most volatile week in decades. That week the market had a range of 18.9%. To have achieved 54%, you would have needed not just the the presence of mind (balls) to buy the market at that micro instant low, but you would have had to have done it amidst unprecedented volatility, and you would have had to go in 100% (no cash). And you only had an instant to do it. If you had waited a week and had caught the top in that second week, then the market has only gone up 26.7% in the last 51 weeks, not 54.44%. Half the 51.59%. Basically, if you missed the bottom of the market by a week and if you had inched in, or pyramided in, not gone all in, you would have lost even more of the gains. There is no one that went in 100% at the bottom. So just in case you get trolled about your performance, you can ask your investor if they really expected you to go all-in at exactly the right micro-instant. Truth is, the convenience of hindsight makes it very easy to complain about fund manager performance, and charts extremes are the most fabulous data points for those complaints. 15 Golden Rules From The PandemicHere are some of the lessons from the last year. Observations about sharp market corrections and their recovery.

At the end of the day, the pandemic year has been great for us as investors. It has been a year of fabulous opportunities. Hopefully you played the game. Look forward to the next great correction. Hopefully we'll all have the vigilance, experience and courage to exploit it, not run from it. Author: Marcus Padley |

|

Funds operated by this manager: |

26 Mar 2024 - Australian Secure Capital Fund - Market Update

|

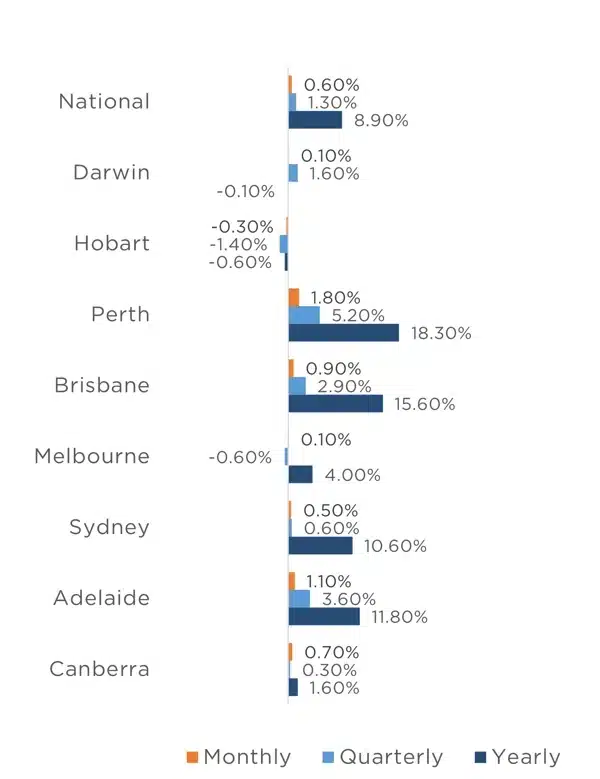

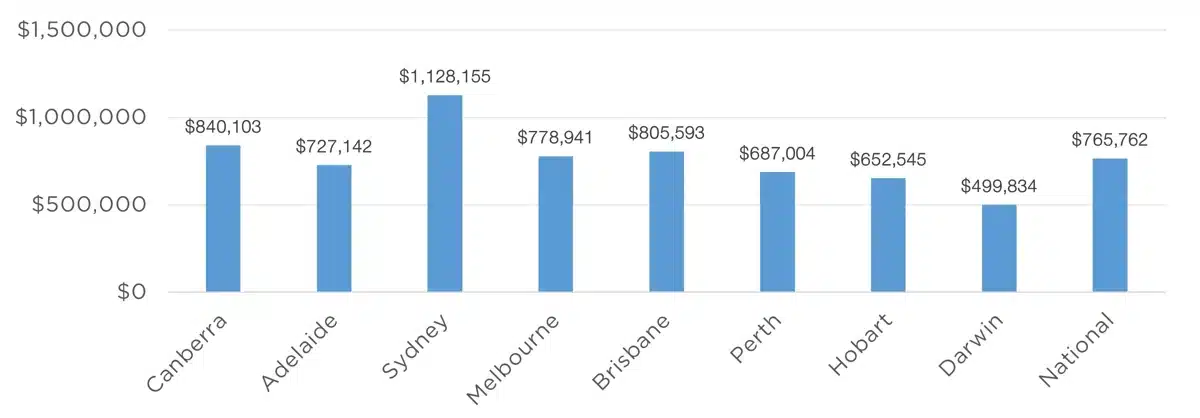

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund March 2024 The first weekend of March saw 2,019 auctions take place across the combined capital cities, down slightly on the previous year's 2,054, however clearance rates were up, 71.8% in comparison to 66.3% in 2023. Melbourne once again led the way, with 1,038 auctions taking place, followed by Sydney with 721, well above that of the other capitals, with Brisbane, Adelaide, Canberra and Perth recording 103, 85, 69 and 3 auctions respectively. The preliminary clearance rate of 71.8% for the weekend indicates that buyers and sellers are on the same page for the most part, particularly in Sydney where a clearance rate of 76.8% was achieved, well above the 68.7% of the same weekend last year. Melbourne, Adelaide, Brisbane and Canberra all managed to achieve clearance rates of above 60% for the weekend, with 70.1%, 69.4%, 65.0% and 63.8% respectively. It is interesting to note that all capital cities achieved a greater clearance rate than the same weekend in 2023, other than Adelaide, where a 72.9% clearance rate was achieved on the same weekend last year. February brought yet another strong month for property prices, with CoreLogic's Home Value Index showing a 0.6% increase across the combined capitals and combined regionals, with all capital cities experiencing growth except for Hobart, where prices fell by 0.3% for the month. Once again, Perth experienced the greatest level of growth, increasing by a mammoth 1.8% for the month, contributing to a 5.2% quarterly growth and an increase of 18.3% annually. Adelaide also experienced strong monthly growth of 1.1%, followed by Brisbane with a further 0.9% increase, bringing the median property value of Brisbane above $800,000 for the first time, with a median value of $805,593, the second highest median value nationally, behind only Sydney with $1,128,155. Canberra, Sydney and Melbourne also experienced growth for the month of 0.7%, 0.5% and 0.1% respectively, with all cities except for Hobart (-0.6%) and Darwin (-0.1%) experiencing an annual increase. Whilst there was no RBA meeting this month, economists continue to believe we are at the end of the rate hike cycle, with many expecting interest rate reductions before the end of 2024. Should interest rates ease, we expect that there will be a bump in property prices. Clearance Rates & Auctions week of 4th of March 2024

Property Values as at 1st of March 2024

Median Dwelling Values as at 1st of March 2024

Quick InsightsValues to OutperformTwo-fifths of valuers surveyed by CBRE have predicted house prices to outperform by up to 10% in Adelaide, Perth, and Sydney. Valuers were also relatively bullish on the apartment sector with 44 per cent predicting prices to increase over the next 12 months. The survey also highlighted a high level of demand from upgraders and downsizers, buyer segments who were less sensitive to interest rate movements. Source: Australian Financial Review Build-to-Rent Builds SteamSalta Properties, is now surging into the build-to-rent sector, with ambitions to create a $3 billion platform and with its first project in inner-city Melbourne close to completion. "We could see that we were heading into a fairly significant housing shortage in Melbourne, and more broadly across Australia," said Sam Tarascio, manager of the firm. The first block is a 94-unit project in trendy Fitzroy North at 249 Queens Parade. To be known as Fitzroy & Co, the building has topped out and is on track to welcome first residents from July into their one, two and three-bedroom apartments. Those tenants can expect a range of resident services, access to shared spaces and a variety of amenities. Source: Australian Financial Review Author: Filippo Sciacca, Director - Investor Relations, Asset Management and Compliance Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

26 Mar 2024 - Performance Report: Digital Asset Fund (Digital Opportunities Class)

[Current Manager Report if available]

25 Mar 2024 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

25 Mar 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Perpetual Smaller Companies Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Perpetual Strategic Capital Fund - Class A | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Altius Sustainable Bond Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| GCQ Flagship Fund (Class P) | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

22 Mar 2024 - Hedge Clippings | 22 March 2024

|

|

|

|

Hedge Clippings | 22 March 2024 While everyone (or nearly everyone) is comfortable that the direction of the next interest rate move is downwards, anyone hoping for clarity on the timing of a cut in Australia would have been disappointed by the RBA's post meeting statement this week. Just take the final paragraph of Michele Bullock's media statement: "While recent data indicates that inflation is easing, it remains high ... it will be some time yet before inflation is sustainably in the target range. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain, and the Board is not ruling anything in or out ... and will rely upon the data and the evolving assessment of risks. In other words, we a) either don't believe the numbers, or b) don't want to fall into the trap that Philip Lore did, and make any prediction. Over in the US Jerome Powell wasn't much more helpful: While noting that inflation has cooled considerably from its peak, he added, "inflation is still too high, ongoing progress in bringing it down is not assured and the path forward is uncertain." "The risks are really two-sided here," Powell said. "We're in a situation where if we ease too much or too soon, we could see inflation come back. And if we ease too late, we could see unnecessary harm to employment." In spite of Powell's two-bob-each-way comments, the market took notice of the US Fed's "dot plot" that there would be three movements of 0.25% later in the year. To be fair to the RBA, there are still some known knowns and resulting known unknowns clouding the issue. In July the Stage lll tax cuts take effect, last week aged care workers were (deservedly, in our opinion) awarded wage rises of up to 28%, and there's a risk of flow ons to other sectors as a result. On top of that unemployment unexpectedly fell to 3.7%, in spite of Australia's population growing by 2.5% to September 2023, 83% of which came from net overseas migration totalling 548,800 people. Given housing starts have been inadequate for the past 10 years to cater for the increase in population, that's likely to keep the cost of buying - or renting - a home higher, adding to the inflation pressure. Hedge Clippings has been saying for a while that inflation's "last mile" down from 3.4% to a sustainable 2.5% is going to be a slow process, and the RBA's comments above would seem to bear that out. Meanwhile back to one of our regular, and we have to admit favourite subjects on a Friday afternoon, "The Donald." Trump, who along with his adult sons, is facing somewhat of a liquidity crisis as he battles multiple court cases, ranging from fraud over the value of his New York property empire (bond required of US$355 million, plus interest), through to damages and defamation of E. Jean Carroll following a finding of sexual assault. To give an Australian flavour to the Donald's news feed, this week he gave a little slap to another of our old favourites, ex PM and now ambassador to the US, none other than Kevin '07 Rudd. It turns out that like us, Rudd has been less than complimentary in the past when referring to Trump, who in turn has added our Kevin to his "List" of those he thinks poorly of. The only hope for Kevin is that while Trump is quick to add names to his list, he is equally quick to remove them if it suits the moment. Hedge Clippings has an old (nameless) friend who has also been known to add the names of those who have displeased him over the years to his own list, but unlike Trump, once on, the names very rarely, if ever, are taken off! News & Insights New Funds on FundMonitors.com Fund Monitors | Custom Statistics February 2024 Performance News Emit Capital Climate Finance Equity Fund Skerryvore Global Emerging Markets All-Cap Equity Fund 4D Global Infrastructure Fund (Unhedged) Argonaut Natural Resources Fund Insync Global Quality Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

22 Mar 2024 - Performance Report: Cyan C3G Fund

[Current Manager Report if available]

22 Mar 2024 - Future Quality Insights: Navigating the AI arms race

|

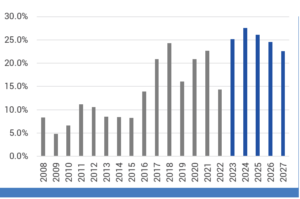

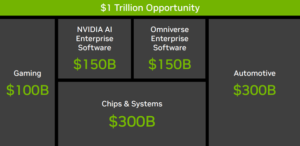

Future Quality Insights: Navigating the AI arms race Yarra Capital Management February 2024 As investment managers, one of the most important - but also one of the hardest - things to do is knowing when to admit you've made a mistake. And errors of judgment can happen frequently in investment - in-depth research, strictly applied investment philosophies and disciplined portfolio execution are all critical tools that can help minimise risk and create robust investment portfolios capable of generating strong long-term returns, but they can't predict the future. So, recognising the need to revisit an investment thesis, or when to reverse a trade entirely, is a lesson all investment managers need to learn. For us, that time came midway through last year. AI: a technology game changer We started 2023 being wary of the technology sector. Many firms within the sector had benefited from the prior cycle of cheap money, leading us to have concerns that such firms would suffer in a tighter spending environment compounded by higher capital costs. What we hadn't anticipated was the rapid emergence of a new form of technology that would structurally change the prospects not only for the tech sector itself, but could also have much wider economic and social implications. AI is not new a technology. In fact, its history can be traced back to the 1950s. But what changed on 30 November 2022, with the launch of ChatGPT, was the emergence of usable generative AI and machine-learning tools that have the potential to completely transform the business world in the decades ahead. Suddenly, the future pathway for the technology sector shifted dramatically. AI will likely define a new era of technology adoption, making it a secular driver of growth that is independent of broader economic trends. Businesses and governments will need to invest in AI or risk being left behind. AI has become the new arms race. Applying a Future Quality lens to AI Having discerned that there's more to AI than hype, we conducted rational and focused research to ascertain the extent to which AI overlaps with the principles of our Future Quality philosophy. Not only did we conclude that AI is a tangible, long-term trend, but we were also able to identify a host of reasons for why capital expenditure on AI should grow rapidly. The cost of undertaking machine learning and AI is massive; leading-edge computers are required to handle these models and datacentres will need to be scaled up. The tech titans are leading this AI spending, dipping into their deep pockets as they perceive AI as a way to deepen the moats around their franchises. Similarly, governments are also allocating funds to capture the military capabilities of AI and its utilisation in modern warfare. This deep dive into AI clearly established that the sector would benefit from a very real and tangible tailwind that would likely endure for the next decade or longer. While our bottom-up, stock-picking investment approach centres around finding Future Quality companies - those which are able to grow, attain and sustain superior returns on invested capital and have key quality pillars in place (Franchise, Management, Balance Sheet and Valuation) - we are not averse to harnessing long-term structural themes that will help drive that growth. AI undoubtedly represents one such driver, but we also track several other so-called 'mega themes' in order to identify other investment prospects and ensure our portfolio benefits from a diversified set of independent growth drivers. At present, we see long-term alpha opportunities from enablers of the energy transition; the normalisation and structural growth in global travel following pandemic-imposed restrictions; and among the providers of more efficient healthcare at a time when the world's population is ageing rapidly and there is a great need to reduce the cost of health services worldwide. A Future Quality case study: Nvidia Once a trend has been robustly ascertained, the next step is to look at the set of players to identify who will be the likely winners and losers. To do this, we looked back at previous waves of technology adoption - there have already been several over the last few decades - and found that leading hardware providers have dominated. They have had first mover advantage and have taken the lion's share of profitability. In the mainframe era, the winner was IBM. In terms of PC adoption it was Intel, and for smartphones it has undoubtedly been Apple. So, when we looked at hardware spend on AI, we found that one name currently leads the pack: Nvidia. Nvidia ticks all the boxes of our Future Quality thesis. It has long-term leadership in the provision of the GPU/DPU technology needed for leading-edge AI, making it the partner of choice for many key technology customers (Franchise). It has stable management and scores highly in terms of both corporate governance and human capital development (Management). Its balance sheet is strong, with net cash, high free cash flow returns and further share buybacks are expected (Balance Sheet). As one of the magnificent seven stocks that led the stock market advance last year, its share price may have already appreciated significantly, but we forecast an enduring period of high growth (Valuation). Chart 1: Nvidia cash return on equity (%), 2023 - 2027 |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

21 Mar 2024 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]