NEWS

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +4.98% in March, outperforming the ASX 200 Total Return benchmark by +1.71% compared with the ASX 200 Total Return benchmark which rose by +3.27%. Since inception in June 2017, the fund has...

Read more...

Why reframing fixed income is key to portfolio stability

Conventional portfolio construction theory positions equities as the primary driver of returns, while fixed income typically takes a back seat as a low-return and low-risk asset class. However, this perspective often overlooks a crucial...

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +1.76% in March. Since inception in March 2016, the fund has returned +9.22% per annum, an outperformance of +0.73% relative to the S&P Global Infrastructure TR (AUD) benchmark which has...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +1.62% in March. Since inception in January 2013, the fund has returned +12.97% per annum, an outperformance of +3.69% relative to the ASX 200 Total Return benchmark which has returned +9.28% on an...

Read more...

Performance Report: ASCF High Yield Fund

The ASCF High Yield Fund rose by +0.62% in March. Since inception in March 2017, the fund has returned +8.17% per annum, an outperformance of +6.54% relative to the Bloomberg AusBond Composite 0+ Yr benchmark which has returned +1.63% on...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +1.95% in March. Since inception in February 2009, the fund has returned +13.62% per annum, an outperformance of +3.57% relative to the ASX 200 Total Return benchmark which has...

Read more...

Performance Report: Delft Partners Global High Conviction Strategy

The Delft Partners Global High Conviction Strategy rose by +5.97% in March, outperforming the All Countries World (AUD) benchmark by +2.96%. Since inception in August 2011, the strategy has returned +15.42% per annum, an outperformance of...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund rose by +2.14% in March. Since inception in February 2009, the fund has returned +12.22% per annum, an outperformance of +2.17% relative to the ASX 200 Total Return benchmark which has returned...

Read more...

Performance Report: Rixon Income Fund

The Rixon Income Fund rose by +0.94% in March. Since inception in November 2022, the fund has returned +12.37% per annum, an outperformance of +3.51% relative to the RBA Cash Rate + 5% benchmark which has returned +8.86% on an annualised...

Read more...

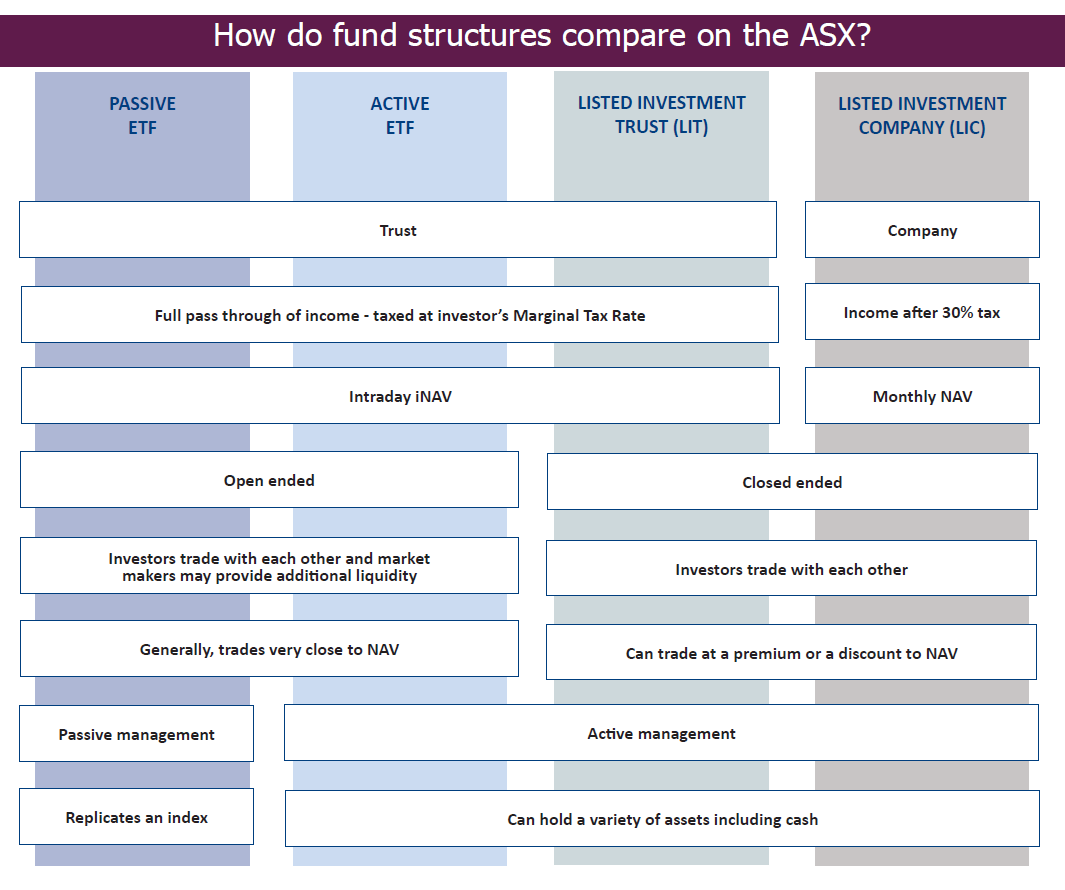

Exchange Traded Funds

Exchange Traded Funds (ETFs) are a simple way for investors to gain access to a wide range of asset classes. They are open-ended funds whose units trade on a securities exchange (Exchange), just like an ordinary listed security. They...

Read more...