NEWS

23 Oct 2024 - Investment Perspectives: 10 charts that recently caught our eye

22 Oct 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Dimensional Global Real Estate Trust Unhedged Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Global Small Company Trust - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Global Sustainability Trust AUD Hedged Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Global Sustainability Trust Unhedged Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Global Value Trust - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Realm Short Term Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 850 others |

21 Oct 2024 - Manager Insights | Seed Funds Management

|

Chris Gosselin, CEO of Australian Fund Monitors, speaks to Nichols Chaplin, Director and Portfolio Manager at Seed Funds Management. Nicholas shares insights on APRA's plan to phase out additional tier one bonds, which could destabilise the banking sector and impact retail investors. The Seed Funds Management Hybrid Income Fund has a track record of 9 years and has outperformed the Solactive Australian Hybrid Securities (Net) benchmark since inception in October 2015, providing investors with an annualised return of 6.39% compared with the benchmark's return of 4.86% over the same period.

|

18 Oct 2024 - Global Investment Committee's outlook: low risk no longer

|

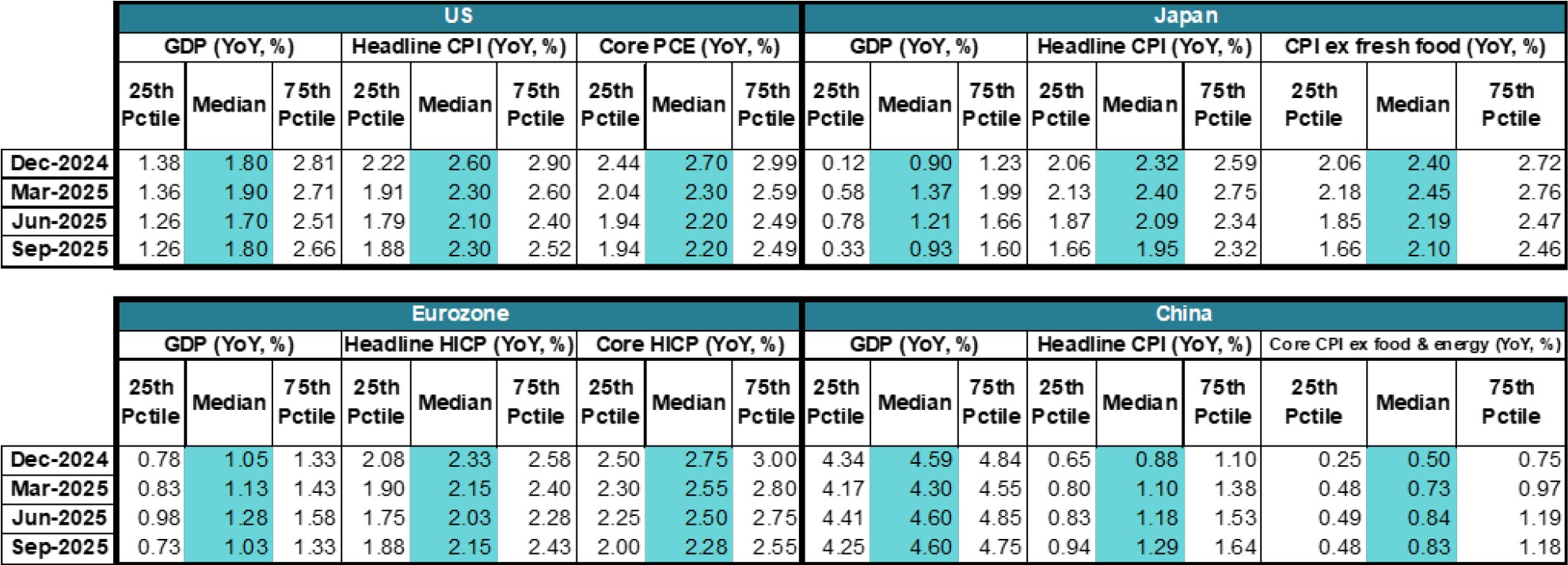

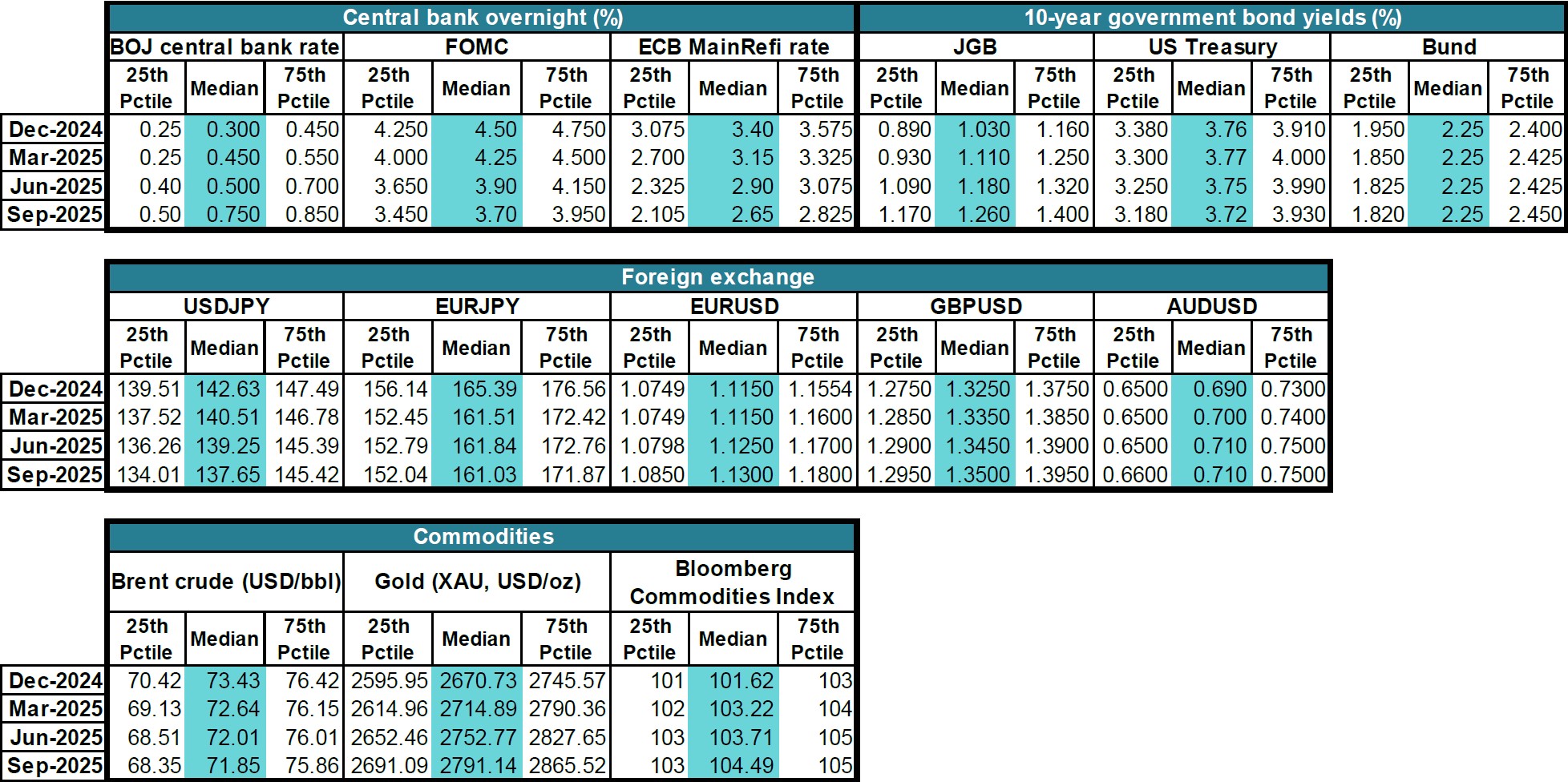

Global Investment Committee's outlook: low risk no longer Nikko Asset Management October 2024 As the Global Investment Committee (GIC) convened on 26 September, our Q2 outlook for resilient though somewhat softer US growth had materialised. However, our US EPS growth estimates (consistent with strong but softer GDP growth) remained slightly more conservative than market estimates. Going forward, we perceive heightened risk to both growth (two-way) and inflation (upside) compared to our Q2 guidance. Nevertheless, our central near-term scenario remains for slowing but positive growth in the US, alongside slowly moderating prices. Key takeaways are as follows:

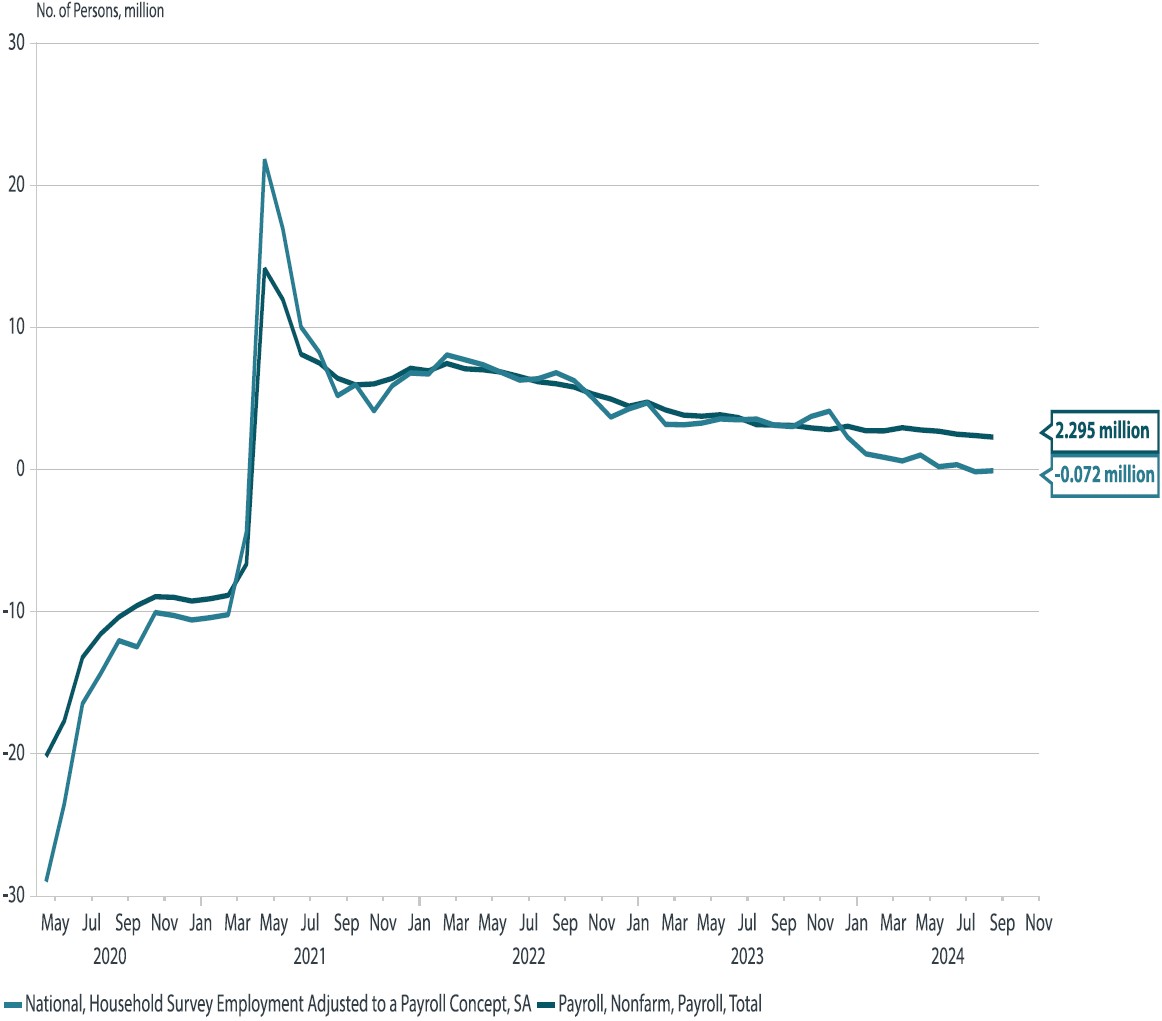

Q3 2024 in review: the "great dispersion" in stocks and bondsOver the course of Q3, the market experienced a change of course on several factors. Following a surprise rate hike from the Bank of Japan (BOJ) in July (the central bank took overnight rates to 25 bps), a downside surprise in US non-farm payroll data triggered speculation of imminent Fed rate cuts. This, in turn, led to the unwinding of speculative yen-funded "carry trades", triggering both a sudden drop in dollar-yen as well as unexpected volatility in Japanese equities--the target investments of short-term overseas investors utilising borrowed yen. Markets recovered quickly from the volatility, although dollar-yen appears to have corrected decisively lower from highs above 160. Domestic investors went bargain hunting as Japanese indices sold off and Japanese corporates used their large cash balances to buy back their shares at lower prices. Underweight institutional investors accumulated domestic equities to rebalance their portfolios while households, unfazed by speculative selling, continued to exercise the tax advantages that accrued to them under the New NISA. We convened an Extraordinary GIC at the time and shifted our guidance, primarily to allow for greater volatility. Aware that volatility tends to cluster and that markets may be at the threshold of a new volatility regime, we widened our ranges for both US GDP and the FOMC to admit downside risks. We also implemented new ranges for valuation (P/E) alongside existing earnings ranges for Japanese indices. Meanwhile, on the eve of the GIC on 26 September, markets had received news of surprise stimulus from China, on the heels of a larger-than-expected 50 bp rate cut from the FOMC on 19 September which had prompted bond markets to price in a succession of significant US rate cuts. Equity markets subsequently broke to new highs, even as bonds priced in a sombre macroeconomic scenario, though they barely reacted to the Fed's move on 19 September as the market had already priced in multiple 50 bp interest rate cuts. Meanwhile, toward the end of Q3, both Japanese stock markets and dollar-yen were influenced by speculation that Japan's ruling Liberal Democratic Party (LDP) would elect a new Abenomics-inspired leader (and thus prime minister). However, the LDP leadership vote on 27 September resulted in disappointment for the markets, which had to lower their expectations for the BOJ to end or indefinitely postpone its interest rate hike cycle. The LDP elected Shigeru Ishiba as its new leader and prime minister, who subsequently called a snap election for 27 October. However, as we noted in our insight, "Less may be more in Japan's LDP leadership contest", the situation is very different now than at the start of the Abenomics era when inflation struggled to turn positive. In Q3, we not only saw Japanese Q2 corporate earnings remain consistently strong but we also witnessed incipient signals of stronger consumption demand, backed by the advent of positive year-on-year (YoY) real wage growth. Global macro: growth risks persist, inflation tamer vs. Q2 on surfaceUS: From a macroeconomic standpoint, there is not enough clear motivation from underlying economic indicators to price in an imminent US recession, even despite softening data. Although the GIC foresees US GDP growth dipping below the 2% level, our outlook is for YoY growth to remain above 1.5% in the year to September 2025. The US consumer has remained resilient, even despite a softer job market, with consumption among higher-income households assisted by the "wealth effect" of gains in US stocks. While much slower than in early 2024, the US continues to add over two million jobs to non-farm payrolls YoY (see "What the Fed's rate cut tells us about current financial conditions"), which is stronger than job growth typically tends to be immediately prior to a US recession. That said, the unemployment rate has triggered the Sahm rule (typically a forward indicator of recession), due in part due to the widening disparity between the household survey (which shows YoY job growth already in contraction), and based on which the unemployment rate is calculated and the establishment survey, which tabulates non-farm payrolls. Chart 1: Employment conditions in the US

Source: Nikko AM, BLS Motivating the divide in part are disperse conditions between higher income households (where both job conditions and investment income are more supportive) and lower-income households, which are a higher proportion of the household survey than the establishment survey. Meanwhile, we see inflation as likely to stay on a gradual downward trajectory, although our median US core PCE outlook is for prices to show above 2% YoY growth over the course of the year to September 2025. Meanwhile, our voter survey shows a less dispersed central tendency for both headline and US inflation compared to Q2 as inflation subsides gradually. Notwithstanding, several members cite heightened inflationary tail risks. Many of the risks cited by voters have the potential to extend beyond the one-year outlook horizon. Macro vs. forward-looking financial market indicators: We are carefully observing the "great dispersion" of scenarios priced into financial markets, particularly in equities and bonds. We are unconvinced that the circular logic of aggressively lower rates could justify ever-higher equity valuations. This is particularly so given the messaging from the Fed. Although the FOMC did comply with market expectations for a "jumbo" cut in July, Fed Chair Jerome Powell continues to warn against assuming this would be the "new pace" of monetary easing in the absence of clear deterioration of economic conditions. Meanwhile, should economic conditions deteriorate (which is the bond market's signal) we are doubtful that the optimistic scenarios priced into the equity markets would indeed come to pass. Japan: Despite financial volatility in August, Japanese GDP appears to be on a trajectory to continue growing above-trend (potential GDP has been estimated at around 0.6% by the BOJ). Nonetheless, the median GIC voter offers more conservative estimates of Japanese GDP growth than in Q2 (no longer above 2% YoY) thanks in part to slower--albeit positive--growth in the US and other export markets. Meanwhile although headline CPI is foreseen dipping below 2% as early as the September quarter of 2025 with imported price inflation allayed by a slowly strengthening yen, our median GIC outlook is for ex-food inflation to remain above 2% over the year to September 2025. Euro area: The median GIC voter meanwhile foresees Eurozone GDP growth as likely to break above 1% YoY and remain at these levels over the year to September 2025, although both headline and core inflation are likely to remain stubbornly in excess of the European Central Bank (ECB)'s 2% medium-term target. However, immediate upside inflationary risks have been somewhat downgraded since the Q2 GIC, when much greater upside dispersion was seen among voters' estimates of future European inflation in both headline and core HICP. China: were it not for China's recent fiscal and monetary stimulus packages, GIC voters would have likely downgraded their GDP growth outlook, which they expect to still remain in the upper 4% range (but under 5%) over the year to September 2025. According to GIC voters, compared to the beginning of Q3, when stimulus was not priced in, moves by the Fed and the People's Bank of China (PBOC) have shifted the growth outlook. At the beginning of Q3, growth was perceived to come from abroad while now there is much more focus on domestic recovery. Meanwhile, communication between the PBOC and the government, which had previously been much more compartmentalised, now demonstrates greater coordination and a tone of shared urgency among Chinese officials. Their aim extends beyond simply stemming the decline in the housing market, focusing instead on stimulating domestic demand growth. Voters note that Chinese stimulus has been delivered at a time when markets are particularly sensitive to easing, though the size is half of what was delivered in 2009 (CNY 4 trillion vs. CNY 2 trillion in debt-funded fiscal easing in 2024) when the economy was one-third the size it is now. GDP growth is now less likely to falter near the 4% level (compared to the 5% target), particularly in the near-term--specifically, in the fourth quarter of 2024 and the first quarter of 2025. That the package also includes consumption coupons issued by an administration that once eschewed what it deemed "welfarism" underscores the priority for China to keep social unrest at bay given its sluggish domestic economy. Nonetheless, the outlook for headline CPI remains on the 1% handle, with core CPI still foreseen below 1% YoY over the year to September 2025. This is because voters perceive difficulties for China in lifting prices successfully; rather, attempts to date to allay weakness in the much greater consumer economy with investment in industry and export could potentially mean some degree of exportation of deflationary price pressures on exported Chinese goods. However, the impact of such pressures on trade partners could be limited in comparison to the early 2000s given today's higher relative price levels, reduced global trade openness and rise in trade barriers. That said, exported deflationary pressures are not always persistent. Though many Chinese firms do compete on price to gain market share, once gained, price increases often follow in an attempt to expand margins. Interest rates: the power of financial markets, a double-edged swordFOMC: In line with our relatively softer growth and inflation guidance over the year to September 2025, we have also downgraded our FOMC outlook relative to Q2. As mentioned in the "macro" section, softer indicators--particularly pertaining to US jobs--reinforce the need for further rate normalisation, as also apparent in the FOMC's own downgraded "dot plots" for growth, inflation and rates. The median GIC voter took the Fed's own forecast at face value to bring rates another 50 bp lower by the end of 2024. This is less dovish than the outlook currently priced into the bond market, which foresees potential for up to 75 bps in cuts by the end of 2024. Subsequently, the GIC foresees roughly 25 bps of easing per quarter, with a median outlook of 3.7% and an interquartile range between 3.45% and 3.95% by the end of September 2025. BOJ overnight rates: In Q2, we had priced in a partial but not a full probability of a July rate hike, which we saw as a modest surprise. However, following our August review, we saw little risk of the BOJ following up its surprise July hike with immediate additional tightening prior to gauging the impact of its move in Q3. Moreover, the BOJ called out both financial markets volatility as well as uncertainty abroad (e.g. in US growth) as one reason to remain on hold in September. Much like the influence that the markets appear to have had on the Fed's "pre-emptive" 50 bp cut, we see the BOJ's stance as being much more market-conscious than it was prior to the volatility experienced in early August. We do foresee potential for another rate hike before year-end, but such a move would most likely come after the October inflation data is published. According to the media, consumers will face price hikes on 2,900 food and drink items in the month of October (the broadest price increase in 2024 so far), as firms pass along higher raw material costs to consumers. GIC voters are therefore pricing in prospects of another hike prior to year-end (with the median guidance at 0.3%). There remains the risk that if financial market volatility resurges, the BOJ may remain on hold--all else being equal--at any point over the coming year. Conversely, if inflation surprises to the upside, there is also the risk that the BOJ could deliver a larger hike; our voters attribute a 25% or less chance that rates may rise to 0.45% before the year-end. Subsequently, the median GIC voter foresees rates as likely to rise to 50 bp by June 2025, and to 75 bps by September 2025. ECB: After the Q2 median guidance of 3.65% for the September-end refinancing rate came in close to the actual outcome, the GIC modestly downgraded its ECB outlook for the coming year. The Fed's larger-than-expected rate cut in September may have opened the door for more aggressive easing by the ECB. The median GIC voter predicts that it is somewhat likely for the ECB to reduce overnight rates before the year-end, with the interquartile range by the end of December 2025 at 3.075% to 3.575%). Nonetheless, given persistent services inflation, especially in Europe, the rate cut outlook is more conservative compared to the FOMC. Our median voter foresees a further 75 bps of cuts as likely in 2025. This compares to the FOMC's 80 bps foreseen for 2025, in addition to the 50 bps of cuts in Q4 2024. 10-year interest rates: Despite the uncomfortable positive correlation between equities and 10-year bond prices (with long-term bonds affording insufficient diversification from market risk), it is hard for participants in the bond market to "fight the Fed" given the apparently strong influence financial markets have on policy. This may paradoxically dilute the power of financial market indicators, including term structures of interest rates, as forward indicators of economic activity. Moreover, the positive correlation across geographies in longer-term bond markets is also apparent, even despite disparate policy trajectories. For example, in spite of improved prospects for near-term BOJ hikes since Q2 as priced into the short end of the JGB yield curve, the term structure of Japanese yields has flattened modestly since July, possibly influenced by Fed easing. Meanwhile, long-term US Treasury yields have declined even though the inversion between the 2- and 10-year benchmark Treasury yield has corrected. GIC voters foresee limited movement in 10 year Treasury yields from their current levels, even despite additional FOMC cuts, due to many of the cuts already being priced into the bond curve. Likewise, voters' central scenario is for little movement in 10-year Bunds over the coming year. One significant caveat--though not a central scenario among voters that inflation will disrupt the Fed's rate cut trajectory-- inflationary surprises and fiscal risk have registered higher than in Q2 in both probability and impact among voters' tail risks (see "Risks to Our Outlook* below). Foreign exchange: gradual yen appreciationFollowing volatility in August, we adjusted our outlook on the Japanese yen to allow for greater appreciation by the currency, as did the market as a whole. Partly responsible for this outlook adjustment was the prospect for narrowing yield differentials as the Fed eased and the BOJ tightened. Also, after observing one round of carry-trade unwinding and observing that market volatility tends to cluster, we upgraded the potential for volatile moves; volatility tends to come alongside yen appreciation. Meanwhile, the dollar's prospects have been downgraded modestly across currencies. The downgrade is less pronounced against the euro, pound and Australian dollar compared to the yen. Noting that the September 2024 BOJ Tankan survey released on 1 October references a fiscal year-end dollar-yen rate of 144.31, which is reasonably close to the spot rate at the time of writing, additional appreciation may impact exporters' overseas revenues, which we cover in the Japanese equities section. Mild upside to commodities, dispersed view on gold and oilIn line with the downward adjustment in oil prices thanks to supply and demand factors, the GIC downgraded its Q2 assumptions on Brent crude, foreseeing oil to remain below USD 80 per barrel for the year to September 2025. Any upside surprise, meanwhile, may result in an upgrade to inflation expectations. While this is not our central scenario, we do see rising tail risks connected to geopolitics, including violence in the Middle East. As its central scenario the GIC foresees mild upside to commodity prices over the coming year. Meanwhile, we expect the quest for diversification away from market risk, along with the inconvenient positive correlation between equities and US Treasuries (a traditional risk haven) will prove very supportive for gold in the coming year. Although the market prices a correction to near USD 2,500 per ounce over the next year, the GIC median voter sees potential for gold to rise above USD 2,700, with a 25% chance of the precious metal climbing to USD 2,800 or higher over the year to September 2025. Earnings growth and equity valuation: making way for higher asset volatilityOver the immediate horizon, the Fed's pre-emptive rate cut has had positive effects. Ongoing stimulus may continue to offer potential for resilient earnings growth from US stocks over the year to September 2025. We foresee double-digit YoY earnings growth still remaining intact over the year to September 2025. However, we also flag risks associated with ongoing market concentration (see "Risks to Our Outlook" below). Although our earnings outlook remains roughly in line with consensus, we foresee the potential for valuations to overshoot near-term due to Fed stimulus, and then gradually moderate over the course of the year to September 2025. We also anticipate potential for rebounds in lower-valued indices, such as the STOXX and Hang Seng. We believe that the latter can capitalise on its recent trough as Chinese stimulus takes effect and earnings growth recovers. But we expect valuations to remain on a downtrend for the STOXX, while we see earnings recovering over the course of the year to September 2025. Japan equities: low valuation + earnings growth + volatility = opportunityAlthough we foresee a rising trend in Japanese earnings and some adjustments in valuation over time, we expect volatility and dips in price creating significant opportunities for new purchases among longer-term investors. Notwithstanding the volatility, we see potential for broad-based Japanese corporate earnings growth, plus significant ability for the index to regain ground after sharp dips. This is due not only to comparatively reasonable valuation relative to US stocks, whose P/E ratios are well above their historical 20-year range, but also Japan's strong structural growth backdrop. This is evidenced by the gathering momentum of domestic consumption and investment alongside improving governance among corporates. We also note the presence of structural buyers in the form of domestic corporates buying back their own shares, institutions topping up domestic shareholdings to meet allocations and households exercising the tax advantages inherent in the new NISA. However, we do not discount the potential for interim negative surprises, particularly among large exporters, given the smaller buffer that current yen rates provide to exporters in terms of overseas revenues and investment income windfalls. Broader price ranges reflecting reactions to earnings surprises and valuation shifts: In August, we had introduced ranges not only for EPS growth but also for P/E ratios. We calculate price ranges taking into account the combined maximum and minimum impacts of earnings growth and valuation shifts. The highs within the price range represent our anticipated upper end of index fluctuations due both to earnings surprises and valuations, which we believe will experience bouts of interim volatility so long as market trading remains dominated by foreign investors (who on aggregate trade more frequently than domestic investors) even though many classes of domestic investors are likelier to buy and hold. Chart 2: Percentage of total TSE trading volume by foreigners

Source: Nikko AM, Tokyo Stock Exchange Risks to our outlook: harbingers of inflationDespite the generally benign outlook to global growth and inflation, our voters cited the following heightened risks that were biased toward the inflationary upside:

Investment strategy conclusion: stay invested, insure against inflationOur anticipated economic outlook remains benign. Although we anticipate a slowdown in US growth, we do not foresee recession as imminent, with the Fed's pre-emptive rate cut already contributing to accommodative financial conditions due to its anticipatory impact on financial markets. Accommodative financial conditions remain supportive near-term. Meanwhile, though it remains difficult to anticipate the timing of market-related corrections, we also signal heightened tail risks associated with policy uncertainty surrounding elections in the US as well as the potential for even small disappointments in economic data and policy to exercise a greater impact on asset markets and therefore growth in the future. We see the risks as biased toward the inflationary, and also foresee the disparity in outlooks priced in by the US bond and stock markets as ultimately unsustainable. In the event of upside risks to inflation, holding stocks (however volatile) may help protect the future purchasing power of investors, while upside may be limited for bonds, even if central banks do deliver easing as anticipated. For this reason, we continue to see demand for assets that are typically resilient to inflation that may also provide diversification hedges against US market risk. We favour gold and increasing exposure to Japanese domestic demand, which is showing signs of sustainable structural recovery and is less correlated with US growth and stimulus than export-oriented firms. The GIC's guidance ranges may be found in Appendix 1 of this document. A note on changes to the Global Investment Committee Process: In June 2024, we made changes to the Global Investment Committee, as to align our quarterly Outlook more closely with the views underlying our portfolio investments. In lieu of forecasts, we have chosen to provide guidance ranges for indicators and indices that we feel most closely relate to the asset classes we manage. In place of forecasts the Global Investment Committee now provide aggregate guidance at the median for our central outlook, and at the 25th and 75th percentiles. The asset classes represented in our Outlook can change over time, depending on what is most representative of our active investment views. In the event full ranges are not available, this may be interpreted as to mean that the asset class is not a central focal point for our highest conviction investment views. Appendix 1: GIC Outlook guidanceGlobal macro indicators

Central bank rates, forex, fixed income and commodities

Equities

Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund Important disclaimer information Please note that much of the content which appears on this page is intended for the use of professional investors only. |

17 Oct 2024 - The China Pivot: This Time Is Different

|

The China Pivot: This Time Is Different Ox Capital (Fidante Partners) October 2024 Ox Capital has always believed the "perceived" structural problems in China are well discounted by the cheap valuations of Chinese stocks. Furthermore, the underlying issues are less severe than commonly believed for a few reasons.

At Ox, we believe this time is different. The authorities are addressing the important issues.

In addition, there are more policies being considered.

While China has some structural issues, not unlike most other major economies, we have always believed that the key drag to the HK/China share market was a lack of willingness to sufficiently relax policies to tackle the deflationary impulse resulted from property market adjustment. It appears that the direction and magnitude of these new measures can potentially address these challenges. The stock market related measures have the potential to re-invigorate the market and so far the impact is encouraging with share market trading volume in both the Mainland and HK surging with rising stock prices. The property market relaxation policies should stabilise prices. If the authorities follow up by tackling some of the longer-term issues, such as local government finances and income distribution (via taxes and direct transfers), this can improve the fiscal sustainability, defuse risks for the economy and boost end consumption demand. This pivot from the authorities can ignite the long-awaited Chinese economy reflation. Given the extremely attractive valuations, upside from here can be highly rewarding. Funds operated by this manager: Ox Capital Dynamic Emerging Markets Fund Important Information: This material has been prepared by Ox Capital Management Pty Ltd (Ox Cap) (ABN 60 648 887 914) Ox Cap is the holder of an Australian financial services license AFSL 533828 and is regulated under the laws of Australia. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriaten |

16 Oct 2024 - Glenmore Asset Management - Market Commentary

|

Market Commentary - September Glenmore Asset Management October 2024 Globally, equity markets were broadly positive in September. In the US, the S&P 500 rose +2.0%, the Nasdaq increased +2.7%, whilst in the UK, the FTSE declined -1.7%. In Australia, the All Ordinaries Accumulation Index outperformed, rising +3.5%. The top performing sectors on the ASX were resources and technology, whilst healthcare was the worst performer. Resources was boosted by news of stimulus from the Chinese government, following a period of weak economic growth, whilst technology benefited from lower bond rates as the US Federal Reserve commenced its easing cycle. Notably, small caps outperformed large caps on the ASX (ASX small ords increased +5.1%) as investor risk appetite improved. As discussed, a key event for equity markets in September was the US Federal Reserve cutting interest rates by 0.5% due to inflation reaching acceptable levels and a slowing economy. Whilst the event was expected by the markets, it is still an important milestone for equities, particularly small/mid cap stocks. Currently, Australia is not as close to rate cuts as the US, however we believe some easing in monetary policy is likely in the next 9-12 months. In bond markets, the US 10 year government bond yield fell -8 basis points to 3.78%, whilst in Australia the 10 year bond rate was flat at 3.97%. Funds operated by this manager: |

15 Oct 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||

| Dimensional Global Core Equity Trust (AUD Hedged Class) - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Global Core Equity Trust (Unhedged Class) - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Emerging Markets Sustainability Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Emerging Markets Value Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Global Large Company Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Vanguard Balanced Index Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 850 others |

14 Oct 2024 - Manager Insights | Altor Capital

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Benjamin Harrison, Chief Investment Officer at Altor Capital. The Altor AltFi Income Fund has a track record of 6 years and 5 months and has outperformed the RBA Cash Rate + 5% benchmark since inception in April 2018, providing investors with an annualised return of 11.68% compared with the benchmark's return of 6.67% over the same period.

Disclaimer This video presentation (the "Content") has been prepared by Australian Fund Monitors Pty Ltd, "AFM" (AFSL 324476) and has been prepared without taking into account the investment objectives of the viewer or recipient. The Content is intended for information purposes only, and recipients should conduct full research and take appropriate advice prior to making any investment decisions. The Content is believed to be accurate at the time of publication, but past performance is not guaranteed. Copyright, Australian Fund Monitors Pty Ltd. October 2024. |

11 Oct 2024 - Are high grade bonds a natural choice for strengthening your fixed income allocation

|

Are high grade bonds a natural choice for strengthening your fixed income allocation JCB Jamieson Coote Bonds September 2024 In a rapidly evolving macroeconomic landscape, Australian investors are increasingly turning to global high grade government bonds as a highly defensive component of their investment portfolios. This move is predominately driven by global government bond markets offering greater portfolio diversity, enhanced return potential and broad sources of yield. In this article, we unpack the key themes influencing investors' long-term views on the value of including global high-grade bonds into a fixed income portfolio. Where are we now in the cycle?The key question facing investors today is: Where are we in the current business cycle, and when will the next shift occur? A glance at the economic growth of the world's major economies and stock markets over the past decade reveals that we've been in an extended expansionary phase. However, determining exactly when the cycle will peak is notoriously difficult. While certain indicators have pointed to an approaching recession, accurately predicting this shift remains a challenge. At a time where geopolitical tensions are intensifying and policy makers are grappling with softening global growth and persistent inflation, investors face a landscape of heightened uncertainty on many fronts. Global central banks are embarking on a synchronized interest rate cutting cycle as the narrative has switched this year from inflation concerns to growth concerns. Global inflation has moderated from its peak levels, with current annual rates of inflation at 2.50% in the US (the lowest since February 2021), 2.00% in Canada, 2.20% in the UK, 2.20% in EU and 3.8% in Australia, although forecasted to fall to 2.70%. Meanwhile economic growth has started to show some cracks, which until now has been supported by government spending. Employment remains a key determinant in the direction of growth and recent signs from the US indicate that this is turning. US employment data was recently sharply revised lower - which has triggered anxiety amongst central bankers. In response, they are eager to get on the front foot and curb labour market weakness before it deteriorates sharply. Savings are already getting depleted, and signs of rising delinquency are cautionary tales that will be exacerbated from job losses. Asset allocations can be dynamically adjusted to optimise performance during different phases of the cycle. With the recent loss of US employment momentum, are we moving from Slowdown to Recession? If so, improving asset quality and liquidity will be important to navigate the coming market environment. Chart 1: Phases in the business cycle.The economic cycle consists of four key phases: Boom, Slowdown, Recession and Recovery, which then leads back to another Boom - continuing the cycle.

Expanding horizons: Unlocking enhanced alpha opportunities that may awaitNot all bonds are created equal. High quality sovereign global bonds offer a lower risk profile due to their stability and creditworthiness. These bonds are typically issued by governments with strong financial standing, making them less susceptible to default and economic fluctuations compared to lower-rated or corporate bonds. As a result, they can serve as a safer option for investors seeking to mitigate risk within their portfolios. Global high grade bonds currently present unique alpha opportunities for investors.

Chart 2: Global Government Bonds Have Outperformed International Equities During Major Sell-OffsGlobal government bonds are among the safest investments in an investor's portfolio, offering capital preservation and helping to reduce equity volatility due to their long-term negative correlation with stocks. They also provide stability to portfolios, especially during market downturns. We can observe how global sovereign bonds perform during periods of financial market crises and significant events in the chart below. During the dot-com crash, the global financial crisis and European debt crisis, global government bonds outperformed equities providing capital preservation and a hedge against the equity market collapse. During the COVID-19 pandemic, global sovereign bonds and equities once again exhibited contrasting performances, although the dynamics were more complex than during previous crises. The pandemic caused a sharp, short-term market shock in early 2020, followed by an unprecedented recovery, largely driven by aggressive fiscal and monetary stimulus.

Source: JCB team analysis based on data from Bloomberg. How should investors position fixed income portfolios as global rate cuts begin?When considering the long-term value of fixed income, high grade bonds stand out as one of the safest investments in an investor's portfolio. Not only do they preserve capital but also help reduce equity volatility due to their long-term negative correlation with stocks, ultimately stabilising portfolios during tough market conditions. We believe that now could be an ideal time to lock in elevated income levels and broaden fixed income portfolios to include a variety of global bonds. The onset of the cutting cycle is likely to lead to a decrease in bank deposit rates, making government bonds a more attractive option for investors seeking capital appreciation. As a significant amount of dollars currently parked in money market funds is expected to flow into the government bond sector, this shift is further supported by the frothy nature of the private credit market, which has more than doubled in size since 2019. Interest rate cuts mean private credit's floating rate is less attractive, redirecting capital away from it into higher interest bearing assets. The transparency and liquidity of government bond funds provide a compelling argument for this reallocation. Adapting to market changes: why global sovereign bonds matter nowFalling interest rates signal a shifting investment landscape, presenting new opportunities for asset allocators. Rate cutting cycles underscore the importance of diversification, especially as economic conditions can change rapidly. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

10 Oct 2024 - ESG Insights: China emerges as green energy leader.

|

ESG Insights: China emerges as green energy leader. Tyndall Asset Management September 2024 I recently spent a few days in Hong Kong meeting with Asian companies and experts to explore China's economic shift from relying predominantly on infrastructure and real estate to its emergence as a global leader in renewable energy. Government policies support emerging industriesChina's rapid economic growth over the last few decades has been driven by investment, infrastructure development, and real estate. In 2021, real estate investment accounted for 27% of China's total fixed asset investment, but by 2023, this figure had fallen to 22% and is arguably even lower today. The sector has faced shrinking investments, declining sales, and a notable drop in housing prices. Between January and July 2024, real estate development investment decreased by 10.2% year-on-year (YoY) to RMB 6.09 trillion. The gross floor area (GFA) of new construction starts also saw a significant decline, with a 23.2% YoY decrease, while the GFA of completed projects dropped by 21.8% YoY. Although real estate remains a significant contributor to the economy, the Chinese government has been actively working to diversify the country's economic drivers. The government has introduced policies aimed at reducing payments and interest rates on property loans to prevent a collapse in the real estate market, which remains a vital part of China's economy. At the same time, the government has implemented significant reforms and provided incentives to encourage the growth of key industries such as EVs, solar energy, and lithium-ion batteries. These new sectors are crucial not only for domestic growth but also for China's goal to become a global leader in renewable energy and green technologies. I will discuss two of these industries in further detail in this paper. Global leader in EV manufacturingThe electric vehicle (EV) sector is a cornerstone of China's new industrial policy. As the world shifts toward cleaner energy, China has positioned itself at the forefront of the EV revolution. By 2024, domestic EV penetration had surpassed 50%, reflecting the growing consumer demand for environmentally friendly alternatives to internal combustion engine (ICE) vehicles. The Chinese government's push for sustainable transport has been instrumental in shaping this industry. However, subsidies are no longer the primary source of EV growth, as these vehicles have become competitive with ICE cars. The rapid growth of China's EV market is one of the most significant trends in the country's industrial landscape. In 2023 alone, EV sales in China reached 7.8 million units, representing a significant share of the global EV market. This growth has been driven by several factors, including government subsidies, the development of battery technology and an extensive charging infrastructure network. Additionally, Chinese consumers are increasingly favouring EVs over ICE vehicles. China's EV market is not only expanding domestically but is also influencing global markets. Chinese automakers such as BYD, Li Auto, and NIO are rapidly gaining market share within China and overseas. Chinese EV manufacturers have overtaken many traditional automakers in sales and technological innovation, with BYD now ranked fifth in global EV sales. However, Chinese automakers face challenges in expanding globally, due to the impact of trade barriers and tariffs. In 2024, the European Union imposed tariffs up to 38% on EVs imported from China, while the United States and Canada have also increased tariffs on Chinese EVs. The US and Canada appear to be particularly concerned about the software within the vehicles with a built-in internet connection. The issue relates to concerns on Chinese companies collecting data on American drivers and infrastructure together with the potential for foreign adversaries to remotely manipulate connected cars on the US roads. Overcapacity increases price competitionThe Chinese government's massive investments in EV manufacturing have resulted in an oversupply of vehicles. Many companies, particularly smaller startups, are struggling to maintain profitability due to the high cost of production and competition from established players. While companies like BYD and NIO have scaled production efficiently, others are facing challenges with underutilised capacity and financial losses. This overcapacity has led to price competition, with many manufacturers slashing prices to maintain market share. This has resulted in thin profit margins across the industry, particularly for companies still in the early stages of scaling production. China dominates solar energy productionSolar energy is another key sector in China's energy transition. China is the world's largest producer of solar panels, accounting for over 90% of global production. Between 2021 and 2023, China's solar capacity more than doubled, driven by strong demand and technological innovation. The country added over 200 gigawatts (GW) of solar capacity during this period, making it the largest solar energy producer in the world. The Levelised Cost of Energy (LCOE) for solar power has dropped significantly, making it cost-competitive with traditional energy sources such as coal and natural gas. By 2023, the LCOE for solar power in China fell to just $0.04 per kilowatt-hour, on par with the cost of coal-fired electricity. Chinese companies have improved solar efficiency while reducing production costs, making solar energy more affordable and accessible. This has enabled China to export its solar products globally, particularly in Europe, Asia, and the Americas. One of the most significant innovations in the solar industry has been the development of "N-type" solar cells, which offer higher conversion efficiency than traditional "P-type" cells. These advanced solar cells have helped reduce the overall cost of solar energy, making it more competitive with other forms of electricity generation. Despite this impressive growth, China's solar industry faces similar challenges to the EV industry. The rapid expansion of production capacity has led to an oversupply of solar panels, causing prices to plummet. Between 2021 and 2023, the average cost of solar panels fell by more than 60%, squeezing manufacturers' profit margins. To address overcapacity, the Chinese government has implemented policies encouraging consolidation within the industry. Smaller, less efficient producers are encouraged to exit the market, while larger companies expand their market share. This process of consolidation is expected to help stabilise prices and improve profitability in the long term. Expansion into global marketsChina's solar industry is also expanding its presence in international markets, particularly in Southeast Asia and the Middle East. Chinese companies such as Longi, Jinko Solar, and Trina Solar have established production facilities in countries like Malaysia, Vietnam, and Thailand, where they can benefit from lower production costs and favourable trade policies. In the Middle East, these companies are scaling up operations to meet the region's growing demand for renewable energy. The United Arab Emirates and Saudi Arabia have become key markets for Chinese solar products. China's dominance of the Global Battery marketThe rise of electric vehicles (EVs) has significantly increased the global demand for lithium-ion batteries. As countries strive to transition to cleaner energy sources, the battery industry has become a critical component of this shift. China has emerged as a dominant force in battery production, contributing to a substantial oversupply in the market. China's battery production capacity in 2023 alone matched global demand, highlighting its overwhelming presence in the industry. The country has invested heavily in research and development, with companies like BYD and CATL leading the charge. This dominance is not just in sheer volume but also in technological advancements, making China a formidable player in the global battery market. Global lithium-ion battery manufacturing capacity has outpaced demand, with an estimated 2,600 GWh produced in 2023 against a demand of 950 GWh. This oversupply is expected to increase, leading to falling prices and squeezing profit margins for manufacturers. For consumers, this could mean more affordable EVs and stationary storage solutions. The low prices are making it difficult for new entrants outside of China to compete, even with generous support provided by the US Inflation Reduction Act and other such support structures. The sustainability of the low battery prices is an intriguing question and will likely result in an industry shakeout as is normal during overcapacity cycles. Lithium, a key raw material cost is in over supply and thus helping keep battery prices low. However, regulatory and environmental approvals are making it more difficult to bring on new mining or refining capacity than build a battery plant. This may help bring the supply and demand fundamentals back into balance. ConclusionChina's industrial transition represents a fundamental shift in its economic model, as the country moves away from traditional investment-driven sectors like real estate and toward new, innovative industries such as EVs, solar energy and lithium-ion batteries. These sectors are crucial to China's long-term economic sustainability and its efforts to reduce carbon emissions and become a global leader in green technology. Exports of the traditional labour-intensive products are declining due to falling competitiveness. However, the capital and technology intensive industries are rapidly filling the gap. This transition is not without its challenges. EV, lithium-ion battery and solar industries all currently face significant issues related to overcapacity, profitability, and growing international competition. The Chinese government's role in managing these challenges through policies and supply-side reforms will be critical in ensuring the success of these industries. As China continues to expand its global presence in the EV and solar sectors, it is poised to remain a dominant player in the global market for green technologies. However, the country must navigate complex trade dynamics and competition from other global players to maintain its competitive edge. Western World governments do not want to be totally reliant on China for these technologies. Australia plays a significant role in China's ongoing industrial transition and its legacy industries given its endowment of both critical minerals and iron ore. Tyndall currently holds a modest overweight in the resources sector, exposing it to the short-term stabilisation of the property market and the China economy, as well as to the longer thematic that relates to global decarbonisation and China's industrial transition. Author: Brad Potter, Head of Australian Equities Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |