NEWS

7 May 2024 - Performance Report: Rixon Income Fund

[Current Manager Report if available]

7 May 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Blackwattle Small Cap Quality Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Blackwattle Mid Cap Quality Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Blackwattle Long Short 130/30 Quality Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Blackwattle Large Cap Quality Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Seed Funds Management Hybrid Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

6 May 2024 - Managers Insights | Glenmore Asset Management

|

|

||

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Robert Gregory, Founder and Portfolio Manager at Glenmore Asset Management The Glenmore Australian Equities Fund has a track record of 5 years and 6 months and has outperformed the ASX 200 Total Return benchmark since inception in June 2017, providing investors with an annualised return of 21.78% compared with the benchmark's return of 8.69% over the same period.

<

|

3 May 2024 - Hedge Clippings | 03 May 2024

|

|

|

|

Hedge Clippings | 03 May 2024 Jerome Powell's press conference following the US Federal Reserve's FOMC meeting held front and centre attention this week. He started with the good news, saying there's been "considerable progress" towards the FED's dual mandate to promote maximum employment and stable prices - with inflation easing over the past year, and a strong labour market, before quickly pivoting to the bad news - inflation is too high, progress in bringing it down is not assured, and the path forward is uncertain. As such, inflation is showing a lack of progress towards their 2% target, while economic activity is expanding at a "modest pace" consumer spending is robust, the labour market is tight with unemployment at 3.8%. Hence the bottom line was rates stayed on hold at 5.25 to 5.5%. Previous expectations for a May rate cut have gone out the window, and while Powell indicated it's a "meeting by meeting" decision making process based on the data, he considered a rate hike is unlikely. Longer for stronger seems to be the market's mantra and expectation, with expectations for just one or possibly two cuts later this year, a far cry from the six cuts that had been penciled in at the start of the year. For rate cuts to eventuate, Powell said inflation is going to have to move down, not sideways as it is now, or the labour market is going to have to weaken. However the 2% inflation target is the key, not employment or wages. Overall Powell's favourite word in his conference seemed to be "confidence" either lack of it, or needing it before taking action. Locally next Tuesday sees the RBA take their turn, and like the situation in the US, the Board's view will depend on the data. Household spending slowed further in March, growing just 2.1% vs 4% in February, and retail trade numbers are due next week, and are also expected to be under-whelming. In spite of this, and with the most recent CPI number at 3.8%, and wage rises and tax cuts around the corner, makes a rate cut here equally unlikely with market pundits now pushing rate cuts out until 2025. The RBA's inflation target is higher than the FED's hard 2%, but neither want to admit that their respective targets - while admirable - might be too low for the current environment. To do so would be to admit defeat, and neither will want to go down that path. News & Insights Managers Insights | Glenmore Asset Management New Funds on FundMonitors.com Market Update | Australian Secure Capital Fund 10k Words | Equitable Investors March 2024 Performance News Insync Global Capital Aware Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

3 May 2024 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

3 May 2024 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

3 May 2024 - Staying invested in resources stocks: has the bull-market started?

|

Staying invested in resources stocks: has the bull-market started? Janus Henderson Investors April 2024 At the outset of this year, we suggested that investors should stay invested in resource stocks and join us in our patient wait for a long-anticipated bull market in global natural resources. Updating an annual outlook after just one quarter may seem presumptuous, but there have been many very significant developments in the market that have compelled us to restate the case for staying the course. China continues to grow and innovate at an impressive rate. Electric vehicle design, manufacture and exports look set to rapidly impact global markets. Just as the US has skirted a well-anticipated recession, it appears the China slowdown is turning a corner; we expect to see indications that a cataclysmic slowdown has been averted and normal operations resume. Valuations in the stock and property markets are already at low levels and are pricing in very low expectations, so the surprise factor is much more likely to be to the upside from here. Meanwhile, geopolitics remains complicated, but the "return to normal" in the macroeconomic environment seems to be well underway. It is hard to imagine anything more confounding than the extraordinary distortions created by the pandemic, and three significant conflicts (China-US trade, Ukraine and the Middle East). But underlying all these challenges, global trade continues to surprise on the upside and we are seeing some economic and corporate indicators turning positive for growth. We think much of the unmet demand from the past few years may have yet to be fulfilled, which is among the reasons we see a progressively more positive environment for natural resource companies. On the pathway in the bull-market journey for resourcesIf I step back and contemplate on 35 years in the industry, many well-worn aphorisms can give some guidance and yet at times be completely wrong. For instance, it is generally accepted that commodities prices are mean reverting, that is, they tend to move back to their long-run average over time. This is clearly not true. I am imagining being asked a question by my great granddaughter in 2065 as I near 100 years. She says, "Pa, tell me about the Great Inflation of the 2030s." Well, I say, how surprising would it be to have a systematic commodity inflation of great amplitude over a ten-to-twenty-year period when the world is growing, adding two billion more people, and achieving higher living standards. Globally, we have not invested in commodity production adequately for the prior 15 years, so how can we assume per-capita consumption for three quarters of the world's population has been improved in any meaningful way? To illustrate, in the first 10 years of my investing career, copper was a $1/lb commodity, keeping within a $0.65 to $1.40 range, in a period that was mostly a bear market. Then, it traded between $3.00 to $3.50/lb for almost 20 years. Copper deposits are hard to find, develop into mines and operate. Demand is growing, with electric vehicles, storage batteries, and decarbonisation driving growth of electricity grids - all of which is likely to push prices higher. Copper has just moved higher from a broad pricing range in the past three years, it is now trading at circa $4.30/lb. This suggests we have strong support for the metal that is fundamental to modern human existence, given its broad usage e.g. home appliances, transportation equipment, electronic products, electrical grids and building construction. Similarly, oil was a $15 to $20/per barrel commodity, which moved up to $40 to $65, and now looks to be in an $80-$120 range as seen in the past three years or so. These large step changes of around 3x (300%) can also be seen in other key commodities such as iron ore, gold, uranium, lithium. Another way of expressing this is that the commodity index (S&P GSCI) gained around 10% per year, for 15 years into the peak of the China growth boom commodity super-cycle. The subsequent 15 years have seen the commodity index flat to -1% per year for 15 years. (Past performance does not predict future returns). Which areas have the most constructive outlook?Uranium Gold We have always really liked gold companies. This industry has one of the fastest paths to profitable development with the best potential for project investment returns and short payback years. In addition, it offers great optionality on mine extension and additional district gold discoveries. Oil Fundamentals for resource companies remains strongStrong companies with a multi-decade investment horizon don't 'waste a downturn'. The last three years have been a quiet range-trading period with plenty of noise, but below expectation returns (around 4% p.a., vs expectations of +10%).1 But the companies we invest in have executed some of the largest mergers and acquisitions of all time. Remember Newmont bought Newcrest, Exxon is buying Pioneer, Chevron is attempting to buy Hess, BHP divested their oil business, Agnico bought Kirkland Lake, among others. As a result, the balance sheets of many major natural resource companies look exceptionally healthy. Cash generation typically is high, while dividends and buybacks are robust. We believe that companies like these are very well positioned to capitalise on this new commodities cycle with many opportunities for shareholder value creation. Author: Daniel Sullivan, Head of Global Natural Resources | Portfolio Manager |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund, Janus Henderson Australian Fixed Interest Fund - Institutional, Janus Henderson Cash Fund - Institutional, Janus Henderson Conservative Fixed Interest Fund, Janus Henderson Conservative Fixed Interest Fund - Institutional, Janus Henderson Diversified Credit Fund, Janus Henderson Global Equity Income Fund, Janus Henderson Global Multi-Strategy Fund, Janus Henderson Global Natural Resources Fund, Janus Henderson Tactical Income Fund

1 S&P Global Natural Resources Index All prices shown are in USD unless otherwise stated Bull/bear market: a bear market is one in which the prices of securities are falling in a prolonged or significant manner. A bull market is one in which the prices of securities are rising, especially over a long time. Re-rating: occurs when investors are willing to pay a higher price for an asset, usually in anticipation of higher future earnings/returns. Risk premium: the additional return an investment is expected to provide in excess of the risk-free rate. The riskier an asset is deemed to be, the higher its risk premium, to compensate investors for the additional risk. IMPORTANT INFORMATION Commodities (such as oil, metals and agricultural products) and commodity-linked securities are subject to greater volatility and risk and may not be appropriate for all investors. Commodities are speculative and may be affected by factors including market movements, economic and political developments, supply and demand disruptions, weather, disease and embargoes. Natural resources industries can be significantly affected by changes in natural resource supply and demand, energy and commodity prices, political and economic developments, environmental incidents, energy conservation and exploration projects. Sustainable or Environmental, Social and Governance (ESG) investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than the broader market. There is no guarantee that past trends will continue, or forecasts will be realised. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

|

2 May 2024 - Performance Report: PURE Resources Fund

[Current Manager Report if available]

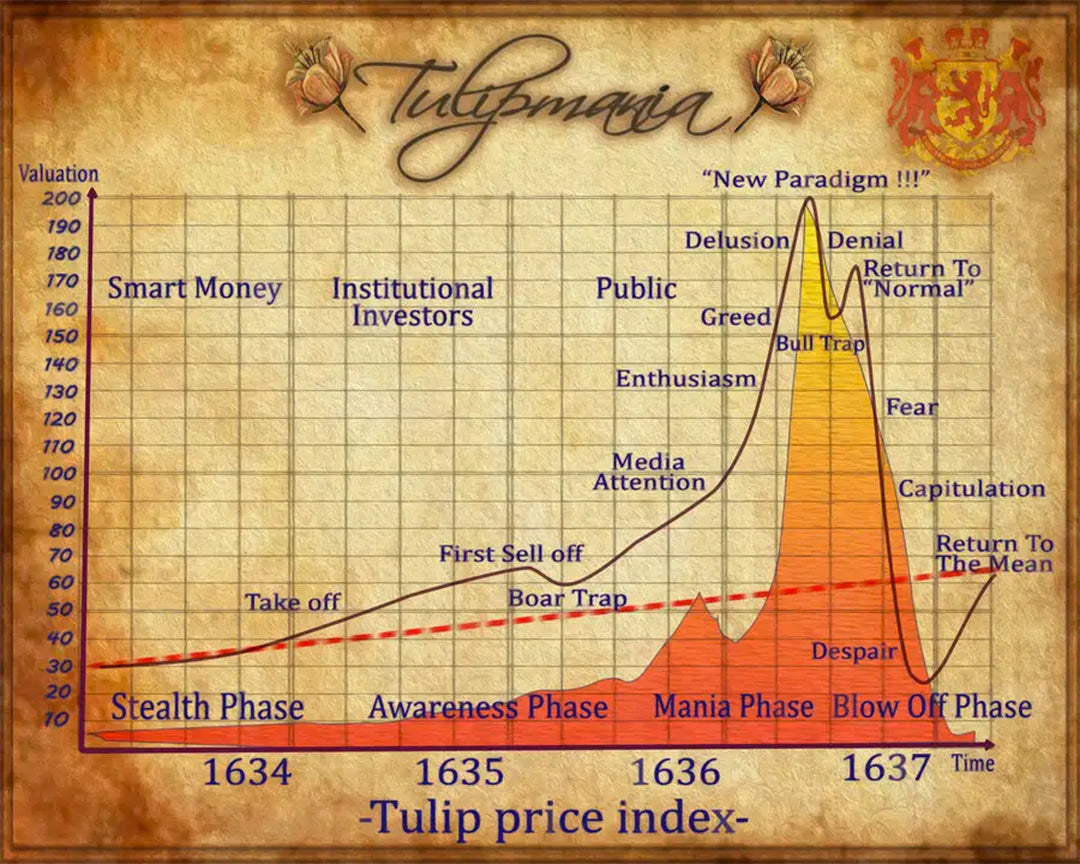

2 May 2024 - Tulipmania

|

Tulipmania Marcus Today April 2024 |

|

When it comes to the stock market, there are rallies, and then there are bubbles.The media slips into 'bubble jargon' on a whim, but bubbles are rare. At the moment, we are in the middle of an AI Bubble apparently, and a Crypto Bubble. But these aren't bubbles, they are not going to be remembered for long.So let's talk real bubbles. There have been a few, the South Sea Bubble (1720), the Dot-Com Bubble (the 2000 Tech Boom and Tech Wreck), the Japanese Real Estate and Stock Market Bubble (the Tokyo property and stock market peaked in 1989, and the Japanese equity market returned minus 7.3% for the next 22 years), the US sub-prime driven Housing Bubble (that led to the GFC), and the most colourful of all bubbles, Tulipmania. Tulipmania - Let me take you back to 1623. This was a bubble. In tulip bulbs of all things. Some of the highlights:

There has been a lot written about bubbles and how to spot them. Here are the lessons from 400 years ago. How to spot a bubble:

Bubbles create crashes. The Wall Street Crash in 1929 and the Tech Wreck in 2000. When speculative demand, rather than intrinsic value, fuels prices, the bubble eventually, but inevitably, and often dramatically, bursts. But to burst a bubble you need a bubble, and it needs to be blown up tight. What bursts it is a bit irrelevant because it is the tightness of the bubble that matters, not the prick. What bursts it can be inconsequential, after all, a "waterfall starts with one drop". The drop is not the cause, it is the pressure that causes the drop. Keep pumping a price up and it will burst, and the more pumped up it gets the less you need to burst it. Just like the drop and the waterfall, all it takes in a stock market bubble is one seller to take the lead and the whole herd goes over the cliff. There is no conventional logic. No warning. No reason. It just went up too much. Bubbles burst. Inevitable in hindsight. When is that? When this is happening:

And in the stock market:

These are the signs of the bottom, the foundations for a recovery. Equity prices go down, risk aversion peaks, and cash is king, When the best investment a company can make is in its own shares, it's time to turn. When you hear companies announcing big share buybacks and increased dividends, you know the world has become too cautious, and the focus is about to shift from risk to return once again. Buy when others are fearful, they say. Absolutely right. When the herd is at their most fearful, the market bottoms. To identify that moment, you have to be objective. You have to watch the herd, not join the herd. You cannot see the herd when you are part of the herd. You cannot coldly turn and exploit the delusion when you have deluded yourself, when you, too, are doing 200 miles an hour with your hair on fire. Where are we now? We have few extremes. We are in the middle ground. A comfortable rally has us thinking things are overbought, but overbought is not a bubble. Overbought does not provoke a 'wreck' or a 'crash'. And neither are we in the opposite of a bubble. Yields are not historically high. No one fears losing their job. Cash is not busting out at the seams. For now - things are 'normal'. Normal is great. We're making money and sleeping soundly at night. Source: Investopedia Footnotes

Author: Marcus Padley |

|

Funds operated by this manager: |

(1).png)

Now let's turn this on its head and see the opposite of a bubble. These are periods of high opportunity and always occur when the crowd has lost its head in pessimism. This is when watching the herd, rather than joining the herd really pays off. At the end of the GFC. At the end of the pandemic. At the end of the Tech Wreck. When the crowd has lost its objectivity. When everyone is undervaluing everything, when everyone is being too bearish.

Now let's turn this on its head and see the opposite of a bubble. These are periods of high opportunity and always occur when the crowd has lost its head in pessimism. This is when watching the herd, rather than joining the herd really pays off. At the end of the GFC. At the end of the pandemic. At the end of the Tech Wreck. When the crowd has lost its objectivity. When everyone is undervaluing everything, when everyone is being too bearish.:max_bytes(150000):strip_icc()/dotdash-five-largest-asset-bubbles-history-FINAL-7eb958a1ff6e49b7ab9c9f3afbaf9d85.jpg)

1 May 2024 - Performance Report: Insync Global Capital Aware Fund

[Current Manager Report if available]