NEWS

3 Feb 2022 - Megatrend in focus: Silver Economy

|

Megatrend in focus: Silver Economy Insync Fund Managers September 2021 Broad trends are quite often easy to identify but what is much harder to do is identify specific industries and companies that are going to economically benefit from these trends and deliver compound annual returns for shareholders over the long term. Genomics or heart disease? A key insight from Insync's work on the ageing population is the projected rate of growth in the 70-75 age bracket. This is the fastest growing five-year age bracket for all people over the age of 55 for the next 15 years and beyond. The proportion of people of this age that develop heart related issues are astronomical.

The heart is a highly focused organ. It has just one job to do, and it does it supremely well. It beats. Slightly more than once every second; that's 100,000 times a day and as many as three and a half billion times in a lifetime. It rhythmically pulses to push blood through your body and recycle it. And these aren't gentle thrusts, they are jolts powerful enough to send blood spurting up to three meters if the aorta is severed.

In comparison to surgical procedures, TAVR has a higher survival rate (99%), lower rate of stroke, bleeding, and other complications. General anaesthesia is not necessary in the procedure and most patients leave after just an overnight stay. This provides a significant cost saving as hospital surgery, anaesthesia and costs of stay are significant burdens to healthcare systems.

Like many new and exciting technologies, it has taken time. Over 15 years in fact, for the market to start adopting TAVR to a level where the companies pioneering the technology become highly profitable and industry leaders.

Many healthcare and innovation investors have focused on genomics and gene editing. After all, it's emerging and exciting- the possibilities are immense. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund |

2 Feb 2022 - How high can government debt-to-GDP ratios soar?

|

How high can government debt-to-GDP ratios soar? Magellan Asset Management January 2022 The 'IMF crisis' is judged the worst event to have hit South Korea since the civil war of 1950-53. The rest of the world knows this financial upheaval as the 'Asia crisis' of 1997. The mismatch is because South Koreans, perhaps ungratefully, focus on the damage after the International Monetary Fund bailed out a country tormented by a currency-turned-banking crisis.[1] The then-record IMF package of US$58 billion dollars was laced with conditions. One was austerity. As government support shrank, South Korea's economy shrivelled 5.1% in 1998 while the jobless rate sprang to 7.0% from 2.1% pre-crisis (1996).[2] The contraction, however, was fleeting. South Korea's economy rebounded in 1999 (expanding 11.9%) and grew every year until the covid-19 pandemic struck in 2020. The jobless rate fell to 3.3% by 2002 and has been 3.something% ever since. Yet the crisis scarred South Koreans. Even though (at 10% of GDP in 1997) public borrowing provided no fuel for the upheaval, one legacy was a consensus that Seoul must not let gross government debt exceed 40% of output.[3] No longer. The government of President Moon Jae-in in August announced a budget for 2022 that vowed to use fiscal stimulus to counter the damage of the pandemic and, more broadly, fight poverty and inequality. Government spending is forecast to expand 8.3% in 2022. Public debt is expected to climb to 50.2% of GDP by next year and reach 59% by 2025, from 36% of output when Moon took office in 2017.[4] And why not let government borrowing rip? Does anyone care that government debt-to-GDP ratios (however imperfectly measured) are higher than seemed possible because interest rates are so low? US government debt is now at 103% of GDP.[5] Eurozone public debt is at a near-record 98.3% of output (where the record is 100.0%). France (114%), Greece (207%) Spain (123%), Italy (156%) and Portugal (135%) make a mockery of the suspended legal limit of 60%; even zero-deficit-by-law-pandemic-excepted Germany (70%) exceeds the legal ceiling.[6] While Australia's federal debt is only headed to 50% of GDP by 2025,[7] Japan's public debt stands at an astonishing 257% of GDP. Public debt in emerging markets extends to a record 64% of output. Brazil (91%), China (69%) and India (91%) exceed the average as do Latin American countries overall (73%). The IMF estimates 'general' government debt now reaches a record 99% of global output, from 83% in 2016.[8] An overarching question, especially when governments are relying on fiscal policy to fight this pandemic and linked economic crisis, is: At what level might public debt become disruptive? A debt crisis would erupt if investors assessed any country were unable to meet its debt repayments. They would baulk at buying, even holding, its bonds. Bond yields would soar, adding to the debt burden, while the country's currency would plunge, which is damaging if debts are denominated in foreign currencies. History is replete with examples of when excessive debt triggered a crisis, from an inflationary economic collapse to endless stagnation ('Japanification'). The role excessive debt played in the fall of the Ottoman and British empires shows it comes with global political implications. So, too, does China's 'debt-trap diplomacy' (that echoes US meddling in Latin America) where Beijing gains sway over emerging countries by giving them loans they can't repay. Governments have three standard ways to tackle their debt burdens. (A fourth would be asset sales, a fifth, conquest and a sixth, reparations.) The first conventional cure is to raise taxes and reduce spending. The UK in September became the first major country to raise taxes to cover covid-19 debt when it lifted payroll taxes.[9] More countries will follow. The handbrake here is that austerity is often politically fraught and can undermine economies so much it might backfire - such an outcome occurs if an economic contraction worsens debt ratios. A second, and the most appealing, option is to ensure economies flourish in a way that erodes real debt burdens over time - this is how the winners reduced their bills after World War II. The formula is to ensure nominal output (GDP unadjusted for inflation) grows at a higher rate than the average interest rate on public debt - a historic norm.[10] A variation on this recipe is that debts will be manageable if inflation-adjusted interest repayments stay below 2% of GDP for the foreseeable future.[11] Over the pandemic, these formulas were met because interest rates were around record lows partly due to central-bank asset purchases.[12] A repeat of the post-World War II drawdown - Washington's debt fell from a record 106.1% of GDP in 1946 to 23% of output in 1974[13] - will be hard because back then pent-up demand, low regulation, favourable demographics and free trade drove economies, huge multi-decade-long advantages that no longer prevail. Still, within this option, governments can choose to allow some inflation and supress interest rates. The benefit of this approach is that rising nominal GDP growth offers governments tax windfalls via higher nominal business profits and by pushing individuals into higher tax brackets. Post-war governments practised 'financial repression' to prevent market forces setting the price of money. But capital controls, fixed-exchange rates, curbed bank lending and ceilings on interest rates would entail a U-turn from the liberalised bent of the past four decades. Low rates would only encourage companies and consumers to add to their record debt loads that come primed with risks too. Permitting inflation is tricky. Officials might lose control of prices if they print too much money and 'debase the coinage' because that comes with economic and political problems.[14] Interest rates would rise if inflation were to accelerate in a durable way, which hampers economies and adds to repayment burdens. Governments would be tempted to pressure central banks not to raise rates, as US presidents Lyndon Johnson and Richard Nixon did to help pay for the Vietnam war. But that would demolish central-bank independence to fight inflation, perhaps the economic policy most responsible for recent prosperity. The other option is to default (and any 'restructuring' is technically a default). When it comes to advanced countries, Japan's debt ratio shows countries with national currencies can rely on their central banks to stave off default for a long time. But, while no defaults in such advanced countries are imminent (now that a fight over the US debt ceiling has been settled for another 12 months), their governments can't boost debt forever. Pressure will mount for authorities to control debt ratios to stop ratings downgrades, perhaps even engage in accounting tricks. Central banks could do this by cancelling the government debt they have bought under quantitative-easing programs.[15] Treasury departments could print trillion-dollar coins.[16] Eurozone governments with high debt ratios are more vulnerable to default because they lack their own currencies. Yet any default could bring down the European Monetary System. More crises around Greece, Italy and perhaps eventually France and Spain that threaten mayhem are likely, especially if bond yields rise after the European Central Bank stops its asset buying. Emerging countries, which are inherently less stable economically and politically, are most likely to default. The candidates are many - the IMF in December estimated that 60% of low-income countries are at "high risk or already in debt distress" compared with 30% in 2015.[17] Emerging countries that have borrowed in foreign currency (a diminishing percentage) and ones that have borrowed from foreigners rather than locals are the most at risk. For indebted advanced and emerging countries, a world of record government debt could soon enough be a realm of hard choices and one of sporadic crises. As the debt status quo appears unsustainable, any rise in US interest rates will signal trouble ahead. To be clear, government debt proved its worth during the pandemic and there's nothing risky with it per se especially when governments borrow in local currency from locals. Sovereign bonds are a useful financial asset that institutions hold for regulatory reasons. Debt allows governments to spread the cost of capital goods across time. A desire to sell debt forces countries to be creditworthy. Debt is a Keynesian tool for managing the economy. The flaw here, however, is that few governments post budget surpluses and debt must be repaid sometime. As Japan shows, debt-to-GDP ratios can climb far higher than thought possible without any obvious damage to an economy. It's true too that few indebted governments are struggling to sell debt at low rates. But, at some point, rising debt would trigger steeper borrowing costs and puncture the complacency that public debts are manageable because interest rates are low. History shows that public debt ushers in its nemesis; higher interest rates. That reckoning one indeterminant day likely means a harsher, poorer, perhaps crisis-prone future awaits. The likely trouble spots On November 30, Federal Reserve Chair Jerome Powell said the central bank's asset-buying program might end "a few months earlier" than its scheduled finish in mid-2022 and that it was "probably a good time to retire that word" [transitory] when describing faster inflation.[18] A report two weeks later showed US consumer prices rose 6.8% in the 12 months to November, the most since 1982. On January 5, by when the Fed had halved its pandemic asset buying to US$60 billion a month, minutes from the Fed's policy-setting meeting showed the central bank was thinking of raising the US cash rate "sooner or at a faster pace" than expected.[19] In Europe on January 7, a report showed eurozone inflation reached 5% in 2021. This fresh record high for the euro area flags the end of the European Central Bank's ultra-loose monetary policy that includes ample purchases of government debt. If the ECB trims, even slashes, its bond purchases, the eurozone's indebted countries will have lost their 'lender of last resort', a term that describes the emergency role that governments can play in countries with bespoke currencies and central banks. By acting as a buyer of its own debt in the absence of other buyers, governments can ensure they won't default on their obligations - though they generally can't avoid an economic crisis as severe as if they had reneged on their repayments. When the ECB reduces, even ends, its asset buying, global bond investors are likely to reprice eurozone sovereign debts according to a country's theoretical ability to repay. 'Lo spread' as the Italians dub the premium on Italian government debt over German bunds, to cite just one example, could well rise to troubling levels. The euro's lack of a supportive fiscal, banking and political union could inevitably lead to more debt crises and bailouts aka those of the 2010s that cast doubt on the single currency's viability. Whatever is happening in the eurozone, emerging markets are likely to more threatened by what the Fed does to global interest rates and what that might mean for the value of the US dollar. A worry is that in 2019 the IMF and World Bank assessed the world's emerging countries were already "at high risk of or already in debt distress" at the end of 2019.[20] Now average gross government debt in emerging markets is up by almost 10 percentage points since 2019 (with large variations around that average).[21] Emerging countries were vulnerable to a financial crisis pre-pandemic because many turned (once again) to borrowing after the global financial crisis. The debts of the 111 low- and middle-income countries more than doubled from US$600 billion in 2008 to US$1.3 trillion by 2018. Over the 10 years, interest plus principal repayments jumped from US$47 billion to US $117 billion.[22] Some worried that the sporadic debt holidays of 2020 - a reneging on debt repayments - could undermine trust in emerging countries and boost risk premiums on their bonds. But, even if continued, they are unlikely to be enough to prevent more developing countries defaulting - Zambia in November 2020 became the first country to default post covid-19.[23] The worry is that emerging countries are inherently riskier investments. They typically have unstable political systems and poor institutions, ones that lack capable and trustworthy bureaucracies. Governments struggle to raise adequate tax revenues, which is why they turn to borrowing. Public finances are often murky. Rule of law is sporadic. The judiciary lacks independence. The media is hobbled. Many rulers have usurped power or have gamed the democratic process to cement their rule. Their subjects identify more with tribal, religious, ethnic or cultural groups than with countries created by colonial powers that lack national unity. The poor institutions, murky politics and tribal allegiances allow corruption to thrive. Economic risks include that emerging countries often rely on a few primary exports. They are thus vulnerable to a drop in the prices of the commodities that earn their foreign exchange. Many are net food importers and their local produce is vulnerable to harsh weather (climate change). While emerging governments these days borrow more in local currency, they are still reliant to a large extent on foreign investors buying their bonds. Default risks are heightened if the investments are short term, thereby requiring constant debt renewal at inauspicious times. It's true that emerging countries, which typically posted higher growth rates than advanced ones, have taken steps to boost their financial stability that averted financial catastrophes at the start of the pandemic. They have built up foreign reserves in recent times to protect their currency regimes. Their central banks are prepared to engage in unconventional steps such as quantitative easing to protect government debt. In March and April last year, for instance, central banks of 14 emerging countries including those of India, Indonesia and Mexico announced bond-buying programs.[24] But many emerging countries have been hard hit by covid-19 in terms of deaths and lost income, especially from absent tourists. Policymakers are aware emerging countries are at risk, especially that their debts tie their fate to rich world monetary policies.[25] Yet the world lacks a global rules-based system for managing such default shocks, something the policymakers at the IMF and UN have investigated without solving.[26] If a government defaults now, only the parties involved sort out an agreement under New York or English law that may involve write-offs, loan extensions, grace periods and rate reductions, even if the negotiations are supervised by the IMF, which is conflicted if it's a creditor. Such an ad-hoc system (compared with US court-overseen corporate or municipal defaults) favours developed over emerging countries and rarely resets a country's financial position onto a sustainable path. The typical result is a country doomed to sporadic crises and economic devastation. Greece's torment of the 2010s, when it underwent three bailouts, serves as a prime example of how a country becomes an investor pariah. Argentina's nine defaults since 1827 offers another.[27] But not industrialised and OECD-belonging South Korea, even if the people there still wince at the acronym, IMF. Written By Michael Collins, Investment Specialist |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund [1] See 'The 1997-98 Korean financial crisis: causes, policy response and lessons.' Speech by Kim Kihwan, Chair of the Seoul Finance Forum, International Advisor to Goldman Sachs and Chair of the Korea National Committee for the Pacific Economic Cooperation Council, at the High-Level Seminar on Crisis Prevention in Emerging Markets organised by the IMF and the government of Singapore. 2006. imf.org/external/np/seminars/eng/2006/cpem/pdf/kihwan.pdf [2] IMF figures for Korea's economy from the World Economic Outlook Database. October 2021. The IMF's definition of gross debt consists of all liabilities that require payment or payments of interest to a creditor at some future point. [3] IMF estimates, the fairest international comparison, even if lagged, place Korean general government at just above 40% since 2015 and score it at a peak of 42% of GDP in 2019. [4] Reuters. 'South Korea drafts aggressive spending plan for 2022, taking government debt to 50% of GDP.' 31 August 2021. reuters.com/world/asia-pacific/skorea-drafts-aggressive-spending-plan-2022-taking-debt-50-gdp-2021-08-31/ [5] Congressional Budget Office. 'An update to the budget and economic outlook: 2021 to 2031.' 1 July 2021. cbo.gov/publication/57218. Within 10 years, half Washington's forecasted budget deficit is expected to go on debt repayments. See Congressional Budget Office. Presentation. 'An overview of the 2021 long-term budget outlook.' 20 May 2021. cbo.gov/publication/57189 [6] Figures as at 30 June 2021, where the eurozone debt record was set on 31 March 2021. Eurostat release. 'Government debt down to 98.3% of GDP in euro area.' 22 October 2021. ec.europa.eu/eurostat/documents/2995521/11563335/2-22102021-AP-EN.pdf/4bc91cb6-b073-d8c8-349d-18aa2bcd2b91 [7] Parliament of Australia. Budget review 2021-22. 'Commonwealth debt.' Net debt is projected to reach 41% of output by 2025. aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/BudgetReview202122/CommonwealthDebt [8] IMF 'Fiscal monitor.' October 2021. See Table 1.2 'General government debt, 2016-26.' Chapter 1. Page 9. Record for emerging markets can be confirmed from the World Economic Outlook Database. October 2021 (op cit). imf.org/en/Publications/FM/Issues/2021/10/13/fiscal-monitor-october-2021 [9] BBC. 'Boris Johnson outlines new 1.25% health and social care tax to pay for reforms.' 7 September 2021. bbc.com/news/uk-politics-58476632 [10] See Olivier Blanchard. 'Public debt and low interest rates.' Working paper 19-4. February 2019. piie.com/publications/working-papers/public-debt-and-low-interest-rates. He responds to criticism of the paper here: 'Why critics of a more relaxed attitude on public debt are wrong.' 15 July 2019. piie.com/blogs/realtime-economic-issues-watch/why-critics-more-relaxed-attitude-public-debt-are-wrong [11] See Jason Furman and Lawrence Summers. 'A reconsideration of fiscal policy in the era of low interest rates.' Discussion draft. 30 November 2020. brookings.edu/wp-content/uploads/2020/11/furman-summers-fiscal-reconsideration-discussion-draft.pdf [12] IMF. 'Fiscal monitor.' October 2021. Chapter 2. 'Strengthening the credibility of public finances.' Page 17. imf.org/en/Publications/FM/Issues/2021/10/13/fiscal-monitor-october-2021 [13] Congressional Budget Office. 'Federal debt: A primer.' See 'Data underlying figures.' 12 March 2020. [14] Higher prices impede economies through 'menu' or mark-up costs, the 'shoe leather' cost as shoppers search for lower prices, relative price distortions and tax distortions against savings income and 'bracket creep' on wages. Inflation redistributes wealth from creditors to debtors, from people of fixed incomes to those on flexible (indexed) incomes, from consumers to producers. Profiteers tend to flourish along with populists. [15] See Mark Dowding. 'BlueBay CIO: It's time to think about debt cancellation.' 4 January 2021. ft.com/content/dffca01a-173a-4d68-bc68-9af9045e712e [16] See ABC News (US). 'Is minting a $1 trillion platinum coin the answer to the debt limit crisis?' 8 October 2021. abcnews.go.com/Politics/minting-trillion-platinum-coin-answer-debt-limit-crisis/story [17] IMF Blog. 'The G20 common framework for debt treatments must be stepped up.' 2 December 2021. blogs.imf.org/2021/12/02/the-g20-common-framework-for-debt-treatments-must-be-stepped-up/ [18] Bloomberg News. 'Powell weighs earlier end to bond tapering amid hot inflation.' 30 November 2021. bloomberg.com/news/articles/2021-11-30/powell-says-appopriate-to-weigh-earlier-end-to-bond-buy-tapering?sref=ORbm2mFs [19] Federal Reserve. 'Minutes of the Federal Open Market Committee. 14 to 15 December 2021.' 5 January 2022. federalreserve.gov/monetarypolicy/fomcminutes20211215.htm [20] International Development Association, IMF. 'The evolution of public debt vulnerabilities in lower income countries.' 2 January 2020. Page 2. documents1.worldbank.org/curated/en/695971579921244762/pdf/The-Evolution-of-Public-Debt-Vulnerabilities-in-Lower-Income-Economies.pdf [21] IMFBlog. 'Emerging economies must prepare for Fed policy tightening.' 10 January 2022. blogs.imf.org/2022/01/10/emerging-economies-must-prepare-for-fed-policy-tightening/ [22] Centre for Economic Policy Research. 'Averting catastrophic debt crises in developing country extraordinary challenges calls for extraordinary measures.' CEPR Policy Insight No 104. July 2020. cepr.org/active/publications/policy_insights/viewpi.php?pino=104 [23] Geopolitical Monitor. 'Zambia becomes first post-covid debt default.' 17 November 2020. geopoliticalmonitor.com/zambia-becomes-first-post-covid-debt-default/. Most sovereign bond contracts do not include automatic force majeure protection that allows contracts to be broken due to unforeseen circumstances such as a pandemic. [24] Adam Tooze. 'Shutdown. How covid shook the world's economy.' Allen Lane. 2021. Page 164. [25] To reduce the risk, many partial solutions are offered to avoid steep defaults. US economist Joseph Stiglitz, for instance, argues for mechanisms such as 'voluntary sovereign-debt buybacks' that proved effective in Latin America in the 1990s and during the Greek crises of the 2010s. "They have the advantage of avoiding the harsh terms that typically come with debt swaps," Stiglitz argues. A buyback program under IMF oversight would aim to reduce debt burdens by securing significant discounts on the face value of sovereign bonds and by minimising exposure to risky private creditors, Stiglitz says. Such programs could advance health, climate and other goals by requiring that beneficiary governments spend the money that otherwise would have gone to debt service on creating public goods. See Centre for Economic Policy Research. Op cit. [26] See IMFBlog. 'Time is ripe for innovation in the world of sovereign debt restructuring.' 19 November 2020. blogs.imf.org/2020/11/19/time-is-ripe-for-innovation-in-the-world-of-sovereign-debt-restructuring/. See also United Nations. 'The commission of experts of the president of the UN General Assembly on reforms of the international monetary and financial system.' 2009. un.org/en/ga/president/63/pdf/calendar/20090325-economiccrisis-commission.pdf [27] Bloomberg. 'One country, nine defaults: Argentina is caught in a vicious cycle.' 11 September 2019. bloomberg.com/news/photo-essays/2019-09-11/one-country-eight-defaults-the-argentine-debacles Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

1 Feb 2022 - Why I think 2022 will be a very good year for investors

|

Why I think 2022 will be a very good year for investors Montgomery Investment Management 05 January 2022 A year ago, I wrote an article in The Australian which set out the factors I thought would make it a very good year for equities. So far, the local market has behaved as expected - despite all the turmoil in the world - with the All Ordinaries up 13.6 per cent for the 12 months to 31 December 2021. Looking ahead, I think markets will continue to reward investors, particularly those who invest in quality businesses. Significant price moves are always determined by the magnitude of surprise. The bigger the surprise, the bigger the move. And so, in the absence of a black swan - something completely unexpected - market returns will be determined by earnings growth. And, completing the idea, the best returns will come from those companies whose earnings grow faster than currently anticipated. For those who believe the market will crash, it is worth remembering such events are typically triggered by the unexpected, the black swan. Those who profited greatly from the Global Financial Crisis were so few and far between a book was written about them. The logic on which they established their trades at the time of the crash was not widely known. When the idea a large cohort of subprime borrowers might be unable to make their first loan repayment was published, it was not widely embraced as a market catalyst. Generally, it won't be what we already know that brings on a correction. For now, we can probably rule out a correction from inflation or the current Omicron strain of COVID-19 because there are as many adherents of these ideas as there are detractors. Most of the headlines warning inflation isn't transitory cite manufacturers and retailers who state emphatically prices aren't coming down. But that isn't tantamount to accelerating inflation. It just means there will be no deflation. If US inflation this year is seven per cent but next year 6.5 per cent, the retailers and the manufacturers will be right - prices aren't going down. It is also true however that price increases are decelerating and that's called Disinflation. Disinflation, when it coincides with economic growth, is historically very good for equities, especially growth equities. Innovative companies and those with pricing power, which tend to be those with sustainable competitive advantages do best in a disinflationary economic expansion. Read any of our documentation and you will find we have always preferred businesses with sustainable economic advantages because it is these companies that produce attractive returns on their equity. Supply chain bottlenecks have impacted almost every corner of commerce and while these bottlenecks remain, inflation will be elevated. Our channel checks of impacted businesses, which include wholesalers, hospitality and retailers, digital, healthcare, IT and advertising, suggest the bottlenecks are lingering. And while that is true it isn't tantamount to further acceleration in the inflation rate. With respect to the inflation discussion, I currently believe only a surprise acceleration would be negative for the market in aggregate. Even fears of such an acceleration won't cause a crash because those fears have persisted for a year now. And don't forget inflation has surged without crashing the market. Following the virus, I believe, is more imperative than following inflation. A new definition for fully-vaccinated is emerging - three doses. On that definition, about one per cent of the world is fully vaccinated, including me. Of course, that means plenty of opportunity for variants to emerge. Understandably, Main Street is worried a variant emerges, able to undermine the current crop of vaccines. Trading at near record highs, market prices suggest such an outcome is not anticipated, so such a development could be an unmitigated disaster. As investors we do have to keep a close eye on the progress of COVID-19. Transmissibility appears to be increasing with each variant. The original variant had a basic R number of about three, followed by Alpha, estimated to have an R0 of 4-5 and Delta, with an R0 of 6-8. Omicron appears to be even higher. Measles has an R0 which has been estimated to be as high as 18 and is therefore one of the most infectious human-to-human diseases. COVID-19 may yet have a long way to evolve. Such developments aren't being widely discussed, so it is these developments, investors should be tracking closely. But of course, through every crisis the highest quality companies, by definition, have fallen less and then rallied first and fastest afterwards. I suggest the same pattern will emerge during and after the next crisis. Take a look at the Buy Now Pay Later (BNPL) sector. We have warned investors about this space since 2018. Describing the players as nothing more than factoring businesses we pointed to three things that investors were missing or deliberately ignoring:

Since we published those many warnings, Afterpay is now down about 49 percent from its 2021 highs and the rest of the field has fallen a minimum of 70 percent from their highs. Investing in quality, avoiding the rubbish and not jumping at the shadows that are already a part of the investment landscape are the keys to navigating markets and it will be no different in 2022. There is the ever-present risk of a 10-15 percent correction but in the absence of a COVID-19 Black Swan, I think investors have little to worry about in 2022. Indeed, if disinflation also emerges, we may just find markets record another strong year. And longer term (sooner if international borders open to migrant workers), I currently expect we will return to structurally lower wages growth and therefore structurally lower inflation and interest rates. All very positive for markets. Written By Roger Montgomery Funds operated by this manager: Montgomery (Private) Fund, Montgomery Small Companies Fund, The Montgomery Fund |

31 Jan 2022 - Running a life settlements fund

|

Running a life settlements fund Laureola Advisors January 2022 Like any fund manager a life settlements fund has a team of specialists and an asset to analyse and purchase to maximise return. It must be understood that the market is tiny where only 3,200 life insurance policies came onto the market last year in the USA. Given the surrender rate of several hundred thousand each year, it is a small number. A lot of people don't often know what a valuable asset they have paid for over many years and simply let them close down. People buy insurance to protect a family or a mortgage debt in the event of untimely death but once the family has grown up and left home and the house paid for, the need for insurance has gone. Typically the insured will contact the insurance company and just accept the contractual surrender value. Some will instead speak to their agent and learn that there is a chance of a far greater cash sum by selling the policy to an investor. In this instance the agent will contact a Licensed Broker whose job it is to represent the seller. He will prepare a file which will include all the policy details and arrange for the insured to have a medical examination the results of which will be provided to one (or more) of the actuarial firms that provide a Life Expectancy (LE) for the individual where the LE is a number usually given in months. It is worth making the point that the LE is not the month in which the insured is expected to die but rather the midpoint on a probability distribution curve where of 1,000 people of the same age and gender and with the same health issues, 500 are expected to die before the LE and 500 after. The file is then sent to Licensed Providers in the U.S. who are the only people legally able to buy an insurance policy from an insured and who represent the investors who are typically managers; an auction process follows. The managers have a great deal of certainty around many of the metrics of the asset; the death benefit is known; the premium costs are known and the credit risk is immaterial; the only thing that is not known is the maturity date. Managers do have the LE which has been provided by the actuarial firms that service the life settlement market and can have access to the medical records but most simply rely upon the LE. It then remains for the manager to choose what discount rate to apply to the cashflows (given the assumed LE) and to make a bid for the policy on that basis. The market usually trades policies where the purchase price assumes a projected internal rate of return (IRR) of between 12% and 14% (though there is wide dispersion around this range) and on this basis the purchase price offered is usually around four times more than the contractual surrender value offered by the insurance company. Most middle-class Americans do not have sufficient assets to fund a comfortable retirement, let alone pay for all the medical and care costs that might be anticipated. Selling their life insurance contract, rather than surrendering it to the insurance company, in many cases makes a very significant difference to the quality of their lives going forward. If the LEs were right and were in fact the mid-point of the mortality curve then the manager could rely upon the law of large numbers, buy lots of policies and expect gross IRRs across the portfolio to be 12% to 14%. The asset is very expensive to track and fund costs are correspondingly high so management fees and fund costs will reduce this gross return by 4% or 5% leaving a net-to-investor return in this situation of 7% to 10%. Most managers and investors do rely upon the accuracy of the LE and the law of large numbers. However, if instead of 500 dying before the LE and 500 after what happens is that only 450 die before and 550 die after, then the LEs from which the policies were purchased and the portfolio was valued are wrong and where the gross projected IRR was 12% to 14%, the gross actual IRR turns out to be 8% to 10%, with a corresponding net-toinvestor return of 3% to 6%. It is obvious that you can test the accuracy of LEs historically, but how can you be sure if forward-looking LEs are accurate? Consider this: With a probability distribution curve over a large population, for any given LE it is possible to predict how many deaths the portfolio would experience each year with a high level of statistical confidence. So, even though the LE has not yet been reached, deaths should already be occurring and the number can be compared with those expected. If the actual number of deaths is (statistically significantly) less than expected, the LE is too short and should be pushed out to fit the early years' experience. History has shown that the LEs provided by the actuarial firms have been and continue to be too short and consequently investor expectations have not been met. If a manager is able to construct a portfolio where half the insureds die before the LE and half afterwards then the gross projected IRRs are preserved and this is the focus of the Laureola investment approach. The six actuarial firms that provide LEs to the market have strengths and weakness across different illnesses and clusters of illnesses. This fact is known qualitatively by all the participants in the life settlement market, including the Licensed Brokers who first bring the policy to the market. It should be no surprise that the Brokers choose the shortest LE available because this pushes the price (and their commission) up. Laureola's four-person investment team spent two years analysing the strengths and weaknesses of the LE providers and has a much better understanding quantitively of how short or long they are with respect to various health conditions. Additionally, Laureola has a medical and scientific advisory panel which reviews the LE in the light of current research. Areas of expertise of the panel include heart disease, circulatory disease and cancer - illnesses which account for the death of two thirds of American citizens. For example the heart specialist (who is working on the leading edge of new treatments for heart disease and has several patents for medical devices) might advise the investment team that there are treatments being developed which might prolong the life of a particular insured with heart or circulatory problems beyond current estimates, in other words that he/she is more likely on average to live beyond the given LE than die before; this would be a reason not to buy this policy. Or in the case of a cancer patient, the Chief Scientific Officer might advise the investment team that a particular insured with a particular from of cancer with particular features and at a particular stage is more likely on average to die before the given LE which would be a reason to consider buying the policy. It is not enough just to buy cheap policies (as measured by the discount rate) because the real value is extracted from this asset class by choosing policies which mature before the LE; all the value of a cheap policy is lost if the insured lives too long past his/her LE. The added value of the Laureola investment team is its focus on the mortality of every single policy in the portfolio. Once a policy has been purchased and is held within the portfolio, it needs to be understood that the health of the insured might worsen or improve over time, affecting its value within the portfolio. Changes in the health of the insureds is critical information for an investment team focussed on the mortality of every policy. Most managers outsource what is loosely referred to as "tracking" to third parties where the information sought is when there has been a death. Laureola carries out the tracking function internally with a team dedicated to forming relationships with the insureds. In the case where the health of an insured has improved, for example by surviving cancer, the team will quickly learn about it and although the improvement in health and life expectancy is to be celebrated, the mortality of the policy has worsened from Laureola's standpoint and the policy has become an underperforming asset. In these circumstances, the investment team is likely to consider selling the policy to another manager. Policies are valued very conservatively within the portfolio and Laureola's experience is that in those circumstances where they have sold policies they have done so at a price higher than the prices marked on the book, thus making cash profits on the sale. Laureola Advisors is an established boutique manager in the life settlement space with a 9-year track record (and only 2 negative months). Over 80% of Laureola's published returns are realised gains, i.e. profits from death benefits or policy sales. Returns which are derived from mortality secure the non-correlation sought by many investors. It takes a 12-person team to run Laureola's life settlements operation because the qualitative input requires time and expertise alongside the quantitative analysis to maximise returns. Written By John Swallow, Director of Investor Relations Funds operated by this manager: |

28 Jan 2022 - What can you make of highs & lows?

|

What can you make of highs & lows? Frazis Capital Partners January 2022 Portfolio Manager Michael Frazis gives a perspective on what could be driving sell-offs We are in the middle of one of those extraordinary periods where valuations collapse and investor time frames have shortened from years to days. Long term plans are forgotten and the whole market is focusing on where prices will land tomorrow. At periods like this extraordinary transfers of wealth take place. As with similar shocks in March 2020, Dec 2018, and 2008/2009, those liquidating shares will realize sharp short term losses, while the immense long term wealth created by fast-growing technology companies over the coming years will flow to those who hold or buy. A number of indications suggest things have reached the kinds of extremes that lead to buying opportunities. Over 40% of the Nasdaq is now down more than 50% from one-year highs, which includes many of the best companies in the world, and many of those likely to generate the highest returns over the coming years. The rolling quarterly new lows in technology is now as high as it has been since Lehman collapsed in 2008, a generational buying opportunity. The performance of technology over the following decade was phenomenal, painful though it was for everyone holding tech shares at the time. Tech bottomed several months before the rest of the market, and then pushed to significant new highs. We saw this dynamic in March 2020, when our fund sold off well before the market - and much harder too - only to recover long before the indices and push to major new highs.

Fortunately, many of these companies raised money or IPOd recently, so we can all be grateful that scientific progress will continue. There's a narrative around rates and quantitative tightening causing the sell-off. There is some truth to this, but a better explanation is that institutions, as they did in March 2020 and 2008/2009, have rushed to the exit, swinging from max overweight to max underweight technology (as measured by data above). Goldman Sachs reported the heaviest tech selling in over five years and that was earlier on in the sell-off. This institutional shift, combined with rising short selling and no doubt some level of retail panic (data on that is harder to come by) is both causing the current volatility and creating opportunity for longer term investors to take the other side. Of course, the most important thing is not to participate in mass selling, and where possible, take advantage. All the gains from the growth in life sciences, software, fintech, and e-commerce will flow to those who end up with the shares being dumped on the market now. The most important thing to know is that our companies are still performing exceptionally well. Many of them are internet-based so we can track real-time data, and they have made substantial progress since the sell-off began, and most certainly since the highs of early 2021. Strikingly, this sell-off has not been triggered by any operational issues. For example: Sea In November only two long months ago, Sea reported: So far, indicators suggest Sea's e-commerce app Shopee is doing even better in India than it was in Brazil, where it quickly became the most downloaded app and already accounts for ~8% of Sea's GMV. After their October launch, Shopee is already the third largest shopping app in India by daily active users. The main negative news was that Tencent, a major shareholder, sold a small portion of its holding below 10%. But even this has a silver lining - as it allows Sea to avoid foreign ownership restrictions in India. In September, Sea raised $6 billion of capital at $318/share (currently $167) leaving the business with $11 billion of cash and a current enterprise value of $88 billion. If you separate the two businesses, and value payments at zero, this is one of the cheapest e-commerce companies around, as well as the fastest growing and most dominant at this scale. As with many of our companies, Sea is truly an apex predator, entering new markets and rapidly taking share, forcing competitors to react. Throughout the sell-off, estimates have been consistently revised upwards:

The difference between serious losses and returning multiples of your capital depends entirely on whether you are a buyer or a seller at times like this, which always feel like an eternity when you're in them. Our fast growing companies may be both the worst place to be during the sell-off, and the best place to be after markets put in a low. This happens well before people expect, and we are starting to reach consensus bearishness reminiscent of those times, as well as a level of seller exhaustion. In previous sell-offs, reporting season marked a turn as investors refocused on the substantial progress our companies had made, often growing 10-20% over the prior three months with improving economics. There is a very good reason to be invested in these kinds of companies. The bulk of investment returns over the next five to ten years will come from these sectors, and accrue to the companies growing and taking market share - the apex predators. We will be fully invested throughout and catch them in their entirety. For the full report and more company analysis, go to Frazis Profile Page. Written By Michael Frazis Funds operated by this manager: Disclaimer The information in this note has been prepared and issued by Frazis Capital Partners Pty Ltd ABN 16 625 521 986 as a corporate authorised representative (CAR No. 1263393) of Frazis Capital Management Pty Ltd ABN 91 638 965 910 AFSL 521445. The Frazis Fund is open to wholesale investors only, as defined in the Corporations Act 2001 (Cth). The Company is not authorised to provide financial product advice to retail clients and information provided does not constitute financial product advice to retail clients. The information provided is for general information purposes only, and does not take into account the personal circumstances or needs of investors. The Company and its directors or employees or associates will use their endeavours to ensure that the information is accurate as at the time of its publication. Notwithstanding this, the Company excludes any representation or warranty as to the accuracy, reliability, or completeness of the information contained on the company website and published documents. The past results of the Company's investment strategy do not necessarily guarantee the future performance or profitability of any investment strategies devised or suggested by the Company. The Company, and its directors or employees or associates, do not guarantee the performance of any financial product or investment decision made in reliance of any material in this document. The Company does not accept any loss or liability which may be suffered by a reader of this document.

|

27 Jan 2022 - Lithium - Where to From Here?

|

Lithium - Where to From Here? Airlie Funds Management 17 January 2022 |

|

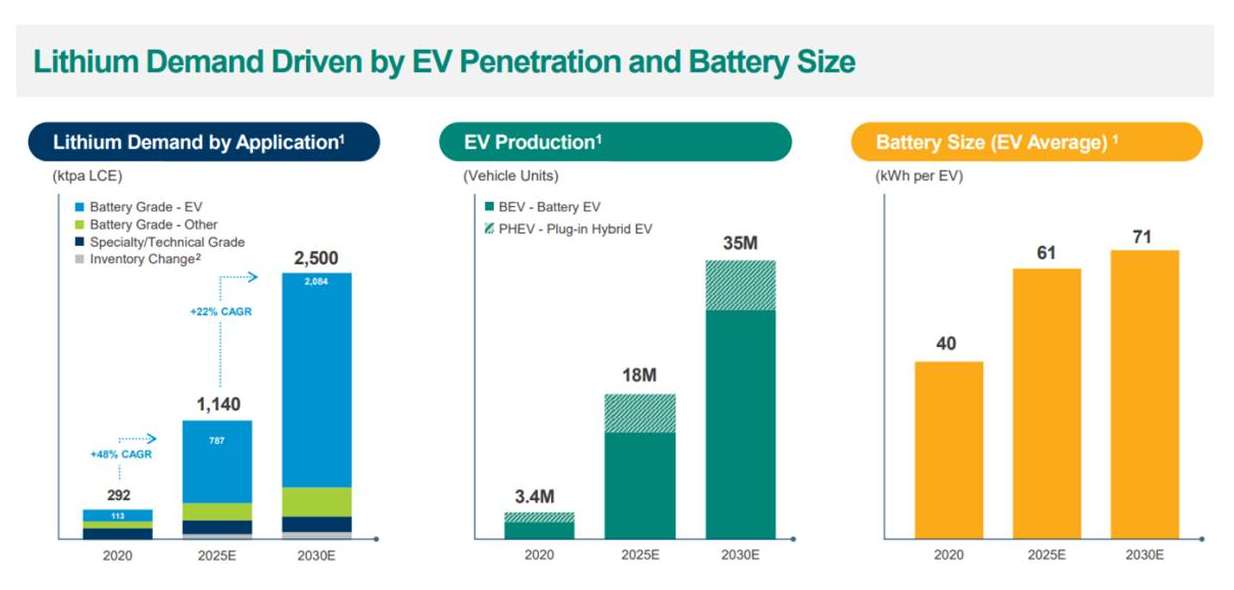

Following on from our report last month on Mineral Resources and in particular its lithium business, we thought our background work on the lithium industry and supply/demand fundamentals might be of interest: Over the past 12 months, the share price movements for ASX-listed lithium producers and developers have been eye-watering. Pure-play producer Pilbara Minerals (PLS) is up +280%. Nickel / lithium producer IGO is up +80%, having completely reshaped their entire business through a procession of transactions to become an integrated "battery metals" business. Iron ore / lithium / mining services company Mineral Resources (MIN - an Airlie favourite) is up +50%, despite a 27% decline in the iron ore price over the same time. Listed developers / explorers Liontown Resources (LTR), Firefinch (FFX) and Core Lithium (CXO) are up +318%, +380% and +270% respectively (!). The sceptic in me is wary of being the greater fool in the lithium sector, but pragmatically the equation is simple - even the most conservative estimates see the lithium market entering a material deficit at some point over the next 10 years as the electrification of transport takes place globally.

Figure 1 - Airlie Funds Management The potential for a material lithium supply deficit means prices for lithium raw materials and chemical products could continue to rise. As more lithium extraction volumes and processing capacity comes online, the cost curve for lithium will continue to evolve and potentially result in a range of economic outcomes for companies depending on their cost position and capital invested. Herein lies the opportunity and uncertainty for investing in lithium extractors and processors going forward. DemandLithium mining and processing aren't new industries, but they are experiencing a structural change in their demand profile. Lithium is a chemical element that doesn't occur freely in nature, but only in compounds, and is generally extracted from hard-rock despots or brines and then processed into a useable chemical product. Historically, demand for lithium chemical products has come from applications in glass and ceramics, as well as additives in steel and aluminium production. Today, due to the superior energy-to-weight characteristics of lithium, lithium chemical products have become an important component of the rechargeable battery cells that can be found in most modern electric vehicles. As the world looks to transition away from fossil fuels, the demand for electric vehicles, and subsequently lithium chemical products, is robust.

Figure 2 - Albemarle Investor Day September 2021; Roskill The trouble is, while lithium is not exactly scare, the supply chain from raw material to useable chemical product is still developing as demand grows rapidly.

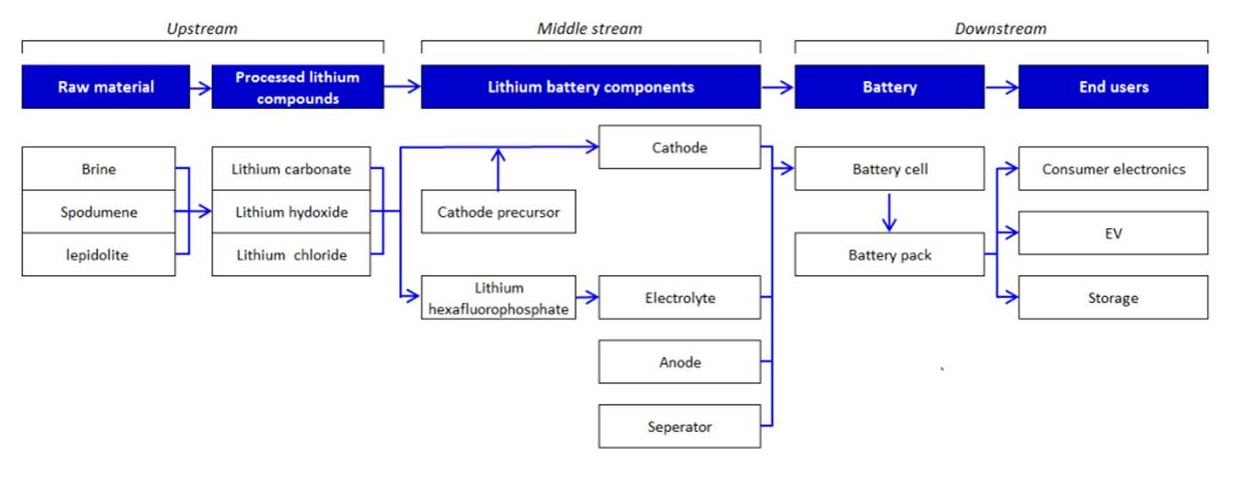

ExtractionAs mentioned earlier, lithium must be extracted (via hard-rock mines or brine lakes) and then processed into a useable chemical product. The Australian lithium extraction industry is dominated by hard-rock assets (mines) that produce an ore which contains the lithium-bearing mineral spodumene. Like all ore bodies, hard rock spodumene deposits can vary in size and grade, which ultimately affects the quantity, quality and cost of the product produced (see Australian spodumene cost curve below). Spodumene must be processed into a concentrate of a suitable grade before it can be processed into a chemical product, and thus higher-grade ore bodies can have significantly less costly pathways to final product. Brine assets (most found in South America) take saline brines with high lithium content and pump them from below the earth's surface into a series of evaporation ponds from which a more concentrated lithium-brine is produced.

ProcessingSpodumene concentrate can be converted directly to lithium hydroxide, while brine assets ultimately produce a lithium carbonate, which can then be further treated to create a hydroxide product if necessary. To further complicate things, not all processing assets are integrated with upstream raw material extraction assets, meaning they must procure raw materials (i.e., spodumene or lithium carbonate) from producers. Currently China has the dominant share of downstream lithium conversion capacity, a function of a historical cost advantage and proximity to customers. Australia's share of global downstream conversion is significantly smaller than its extracted share and will remain so even as assets currently under construction come online. Increasingly, Australian spodumene producers are looking to capitalise on the opportunity for margin expansion via vertical integration into downstream conversion, largely because of the price strength in lithium chemical products and the view that customers will want an ex-China supply chain. Given Australia is long spodumene (and China is short) it makes sense to develop optionality around spodumene concentrate offtake and create a lever around which the "seaborne" lithium products markets can be kept tight. Like extraction assets, processing assets will have different capital requirements and cost positions depending on their location, scale, and access to raw materials. The cost curve for integrated processing assets remains in its infancy, given many projects that make up industry cost estimates are either still under construction or ramping up.

SupplyUltimately to meet demand raw material supply will have to come from both hard-rock and brine assets. Battery chemistry will vary depending on the availability of supply as well as the manufacturers preference, meaning supply of both lithium hydroxide and carbonate will be necessary. The main takeaway here is simply that the lithium battery supply chain is complex, and that given this it should be expected that theoretical supply will undoubtedly differ from realised supply. Below is a consensus estimate of the future supply-demand balance for lithium (as measured in Lithium Carbonate Equivalent tonnes) out to 2030. While obviously these estimates are rubbery, it gives a feel for the extent to which an imbalance may eventuate.

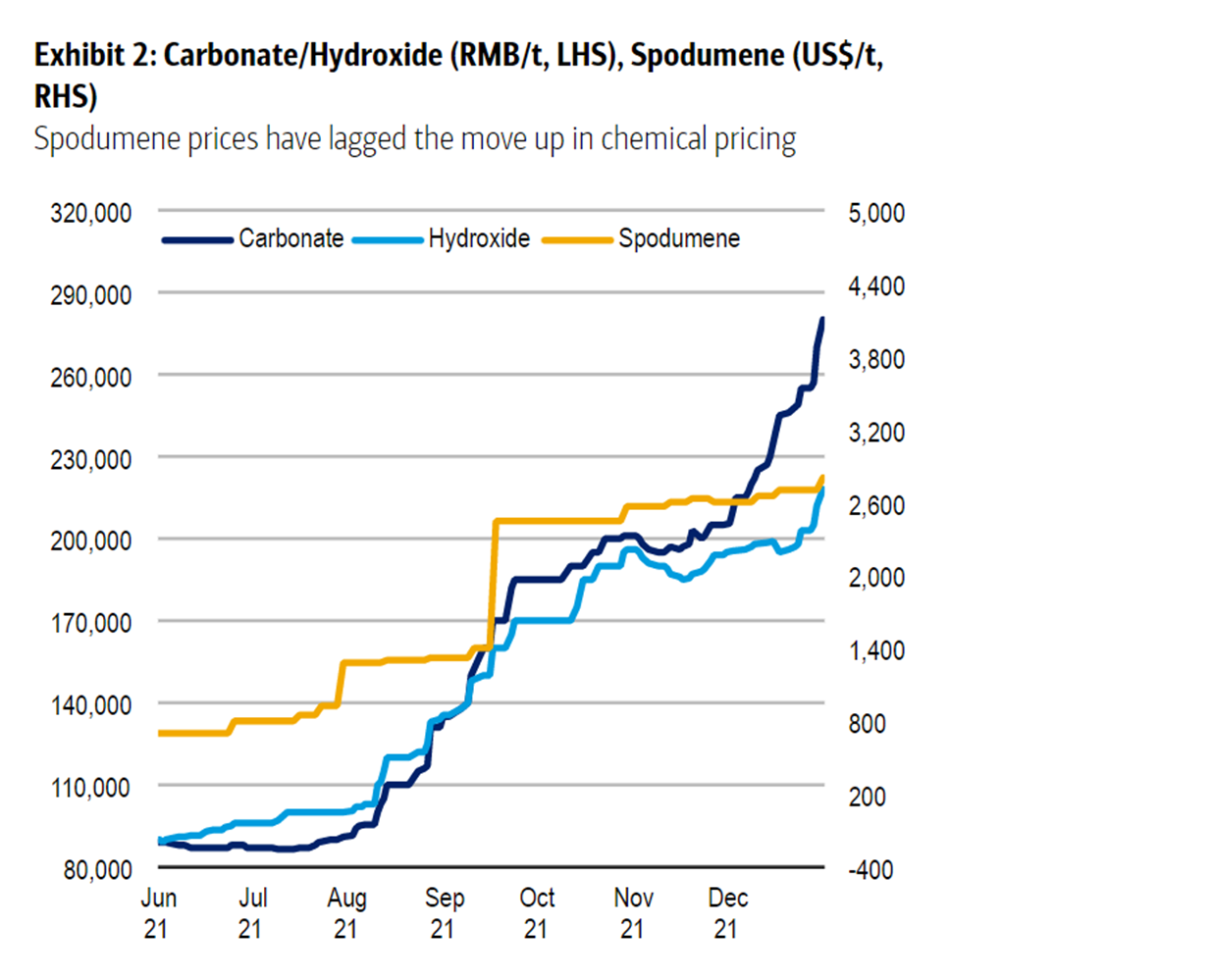

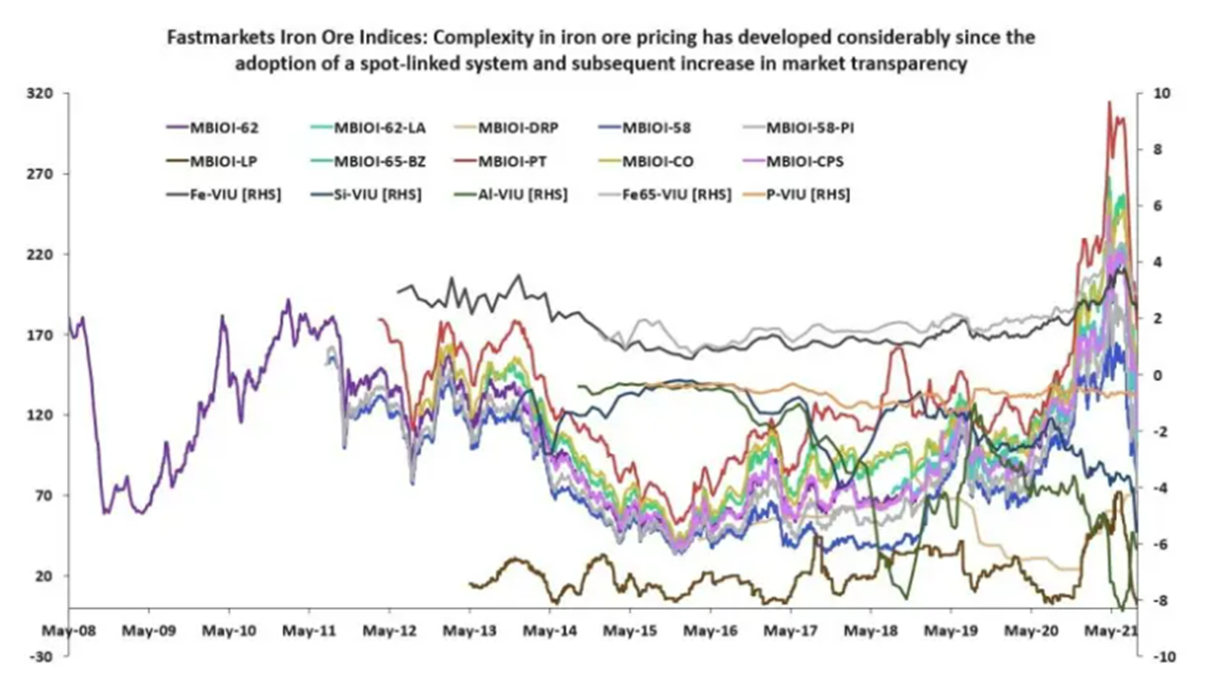

Figure 6- Airlie Funds Management PriceOf course, the reason cost curves, and supply-demand paradigms are poured over by investors is to take a view on future prices. Often with resources stocks, get the commodity price right and you'll give yourself a fighting chance investing in the right companies. Over the past twelve months, prices for lithium products have exploded.

Figure 7 - BofA Global Research, January 2022

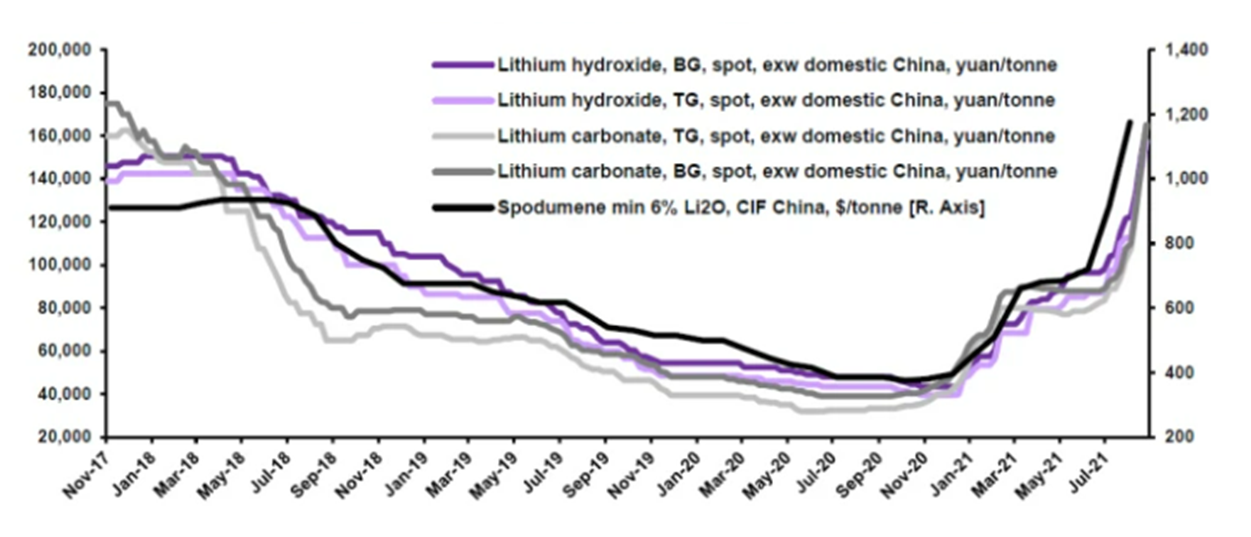

Figure 8 - Fastmarkets 2021 But how should we interpret spot prices given the structure of the lithium industry? Are "spot" prices an accurate reflection of what producers are receiving? At present, spot transactions only account for a small portion of supply of lithium raw materials and chemical product producers, with most volumes traded in fixed price or index-linked contracts (for set periods). For spodumene spot pricing, many market participants have begun relying on Pilbara Minerals (PLS) BMX Platform results, in which the company auctions off small parcels of spodumene to prospective customers. If these "spot" prices reflect what is being paid for the marginal tonne of product, then they still give great insight into the market balance. Without wanting to oversimplify things or draw flawed comparisons, we can look at the development of the iron ore price (and value-in-use price variation) as a guide to how the lithium pricing system could mature. The iron ore market moved to a spot-linked pricing system in 2008, despite considerable variation in product quality and specific end-use. The result has ultimately been a significant increase in market transparency which we believe should be expected for lithium over the next decade.

With greater transparency over market pricing should come greater ability for market participants to allocate capital, and ideally create a smoother transition to electric vehicle use. Yet, as investors we still must take a view on future prices even as pricing systems develop. For mature commodities, long-term price forecasts typically reflect a marginal cost of production, where prices are set by cash operating cost levels that ultimately mean those at the top of the cost curve are not profitable, so as not to induce oversupply. The general rule of thumb most people use here is equivalent to ~90% of the cost curve. An obvious example where this logic is applied is to a mature commodity is again iron ore, where long run prices are usually US$60-80/t, with 90% of the cost curve effective profitable at ~US$70/t. Using this approach for say spodumene, would yield a long run price of ~US$450/t, versus spot of >US$3,000t. Given the lithium market is not "mature" in the sense that pricing is underdeveloped, and the future supply-demand equation remains so unbalance, a marginal cost of production method for forecasting future price is perhaps unreasonable. Instead, to address the future supply-demand imbalance predicted, new production needs to be incentivised - i.e., Long-term pricing must be bid-up to encourage investment in new supply, and so it's not out of the realm of possible that current spot prices can hold for longer than people expect, or for long run prices to settle above the current cost curve (especially given this cost curve will have to change over the next decade). All in all, without a crystal ball and given the plethora of unknowns, we remain open to the possibility that spot prices can hold or go higher despite their impressive run. Even modest changes to the supply-demand equation can see hefty price responses, and it would be foolish to assume to future will not be volatile in both directions. How are we navigating the lithium sector at Airlie?Given the industry dynamics discussed above, we believe it is prudent to have some form of lithium exposure in our portfolio. The uncertainty that features in all aspects of the lithium paradigm means each opportunity warrants a degree of conservatism, and valuation is still important, despite rubbery supply, demand, and price forecasts. Undoubtedly, we will see an endless stream of new explorers-cum-developers front the market over the next decade, some of which will be fantastic investment opportunities and some of which will be looking to take advantage of investor optimism. In our previous Stock Story, we highlighted Mineral Resources (MIN) as our preferred lithium exposure. Mineral Resources represents a compelling investment both in isolation, and when considering its relative valuation versus other ASX-listed producers. For MIN, earnings growth will be driven by the organic expansion of spodumene and iron ore production volumes, as well as the development of a lithium hydroxide conversion plant via a JV with global producer Albemarle. Supporting this growth is MIN's robust mining services business and exceptional management, and it remains a key holding in our portfolios. Written By Joe Wright, Analyst - Airlie Funds Management Funds operated by this manager: Airlie Australian Share Fund |

.PNG)

.PNG)

.PNG)

.PNG)

25 Jan 2022 - Webinar Recording | Paragon Australian Long Short Fund

|

Webinar recording: Paragon Australian Long Short Fund

|

25 Jan 2022 - Some stuff you don't want to think about - but should

|

Some stuff you don't want to think about - but should Delft Partners January 2022 |

|

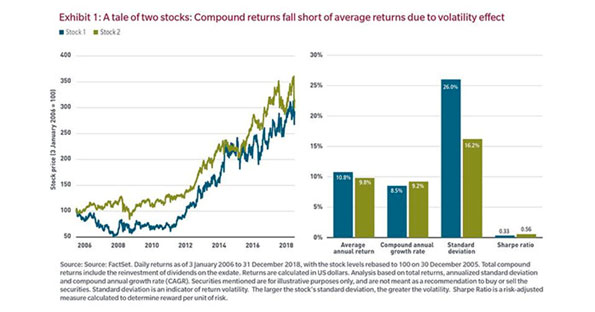

Or Risk is the independent variable and Return, the dependent one. Ever been on a car journey as a passenger where the driver was going too fast; being reckless; and essentially taking chances? Over and under-taking, switching lanes without looking, going too fast and braking too hard. We all have. It's not so pleasant especially as you get older and realise how much is at risk from a needless mistake: your health, your life even; the realisation that family members depend on you staying healthy and not becoming a burden; your enjoyment from their growing old. So, we try to avoid such a scenario. It's relatively easy since reckless driving is usually associated with inexperienced younger members of society in fast cars. So, we can avoid such journeys as being readily identifiable in advance. And yet we often find that a similar journey, multi-generational wealth investing, has older wealthy members indifferent to risk and unaware of the loss of wealth that occurs when insufficient attention is paid to the risk path taken by their managers. Investing Is not so different from a car journey? It's a path to an end point with risk to be managed; speed, comfort, time horizon all matter for investing as much as they do for being driven. Better to get to the end point safely and aware of risks on the way, and how to drive defensively at such times, than to get there at speed dangerously? And yet here we are, perhaps caused by years of unorthodox monetary policy, where many managers and clients perceive risk as irrelevant and an irritant? All focus is upon return - those 'sexy' growth stocks, that 10 bagger PE fund, that property that will inevitably benefit from a lick of paint or a change of use permission, and of course the free put option available to all investors that has been a feature of monetary policy in essentially the last 25 years. So were going to bore you with a brief article on the independent variable known as risk. Return, the glamourous bit, is the dependent variable. No risk, no return. So, if you can't define, measure, and manage risk then your returns are a function of luck. Not a lot of people know that. We spend a lot of time obsessing about risk especially in multi-asset portfolios, whose Alphas and Betas are both correlated at different extents at different times, and where they offer differing opportunities for active and passive approaches at different times. The cost of variance or variance drain The variance of returns over time directly impacts our ability to grow wealth. $100 invested at 5% interest for 30 years grows to become $432. Of that, $100 is of course your initial capital, $150 is the total amount of simple interest paid, and $182 is the effect of compounding - interest on interest. (Let's assume away the taxman?!) Once uncertainty in returns (volatility) is introduced into the mathematics, there is an immediate noticeable drain. If that same investment still yields 5% but now with a volatility of 17% (like a typical equity index ) the cumulative growth rate - the rate your wealth actually grows over time including rises and falls - is now just 3.56%. After 30 years you will have instead of $432 just $285, and you will have lost almost $150 to volatility. Risk is expensive!1 A lower-return investment with a lower risk may often outperform a high-return high-risk alternative.

Multi-asset portfolios of course mitigate the high volatility from equity and many investors choose hard assets to go into the mix since their price is 'not volatile'. However, bonds, especially high yield bonds, can behave like equities at certain times 2 and an absence of price volatility shouldn't be equated with an absence of risk 3. For example, if you own a physical property whose revenues are derived from retail tenants, and your equity portfolio is heavily weighted to retail and consumer companies, guess what happens when a general consumer recession hits. That 'lack' of volatility in the property will suddenly not be so lacking as your cash flows from rental payments dry up and the next valuation of the property will be a jump down in value, and a reduction in re-investable cash flows, just when you most needed to be immune from volatility as a drain on wealth. The infrequent tails that happen too frequently We tend to think of "drawdowns", crashes, corrections, shocks or other sudden unusual "non-Normal" events as a completely different animal from typical market volatility. When we consider investments, we should consider not just volatility or tracking error but also the incidence of these drawdowns. Simple mathematics to transform mean and volatility without drawdowns to equivalent numbers that correctly include the effect of such infrequent drawdowns has been known for almost 100 years 4. If we make this adjustment to historical return series, we observe two troubling effects. First, the historical "alpha" that is often reported in academic papers and relied on by active managers from factors like Momentum, Size, Value, or Beta, once adjustments for drawdowns have been made, either radically shrinks, or disappears, or reverses sign and becomes a persistent drag. This phenomenon is described at length in one of Northfield's recently published journal articles 5. Secondly, adjusted volatility numbers are usually much bigger than the unadjusted numbers - meaning that these investments have both a lower return and a higher risk than would at first appear. The effect of that higher risk is once again, as above, to reduce the effectiveness of compounding. Investments that experience periodic shocks have both lower return than would appear at first glance, and higher risk. Drawdowns are also expensive! The evasive Alpha Another closely related aspect is uncertainty in active management. Unfortunately, Alpha is hard to find, easy to lose, and always changing. Because Alpha is uncertain, we should include that uncertainty in our calculations of risk - in this case it is "the risk of being wrong" or strategy risk 6. It may come as some surprise that usual risk measures completely ignore this and assume that the managers' return is known with certainty. We wish it was. With active management we deliberately move away from the benchmark return and believe that we have a new mean return (our alpha) that is bigger than the benchmark. Tracking error, which originated in passive management, or value at risk, or any other measure that is based on volatility measures variability or uncertainty around the mean (alpha) and says nothing about variability or uncertainty of the mean (alpha) itself. As with all the previous examples - you might be spotting a pattern here - correct inclusion of strategy risk makes the total actual risk of the investment larger, which once again negatively impacts compounding. Active management where big bets are taken is risky and being wrong is very expensive indeed! There is no such thing as linear in the world of risk There is one additional implication of compounding that is utterly ignored - if we consider the compound return, as we should, given its importance to us, then return no longer increases linearly with risk as we are told by the textbooks 7. It is now a convex function, and as risk increases past the peak, our return begins to decline with increasing risk. This has serious implications for asset allocation. In every market there will be a "peak beta", beyond which as explained returns decline with increasing risk, so we must stay to the left of that peak. This tends naturally to send us looking for lower beta stocks, or into multi-asset class portfolios 8. So, what to do? Experienced judgement helps. By experienced we mean professionals whose careers extend back to when corporate failure was possible, when central banks tightened monetary policy as much as they engaged in QE and granted a free put option, and when dividends and balance sheets mattered. Models also help to provide a framework for identifying, measuring, and managing the Betas and the Alphas and their correlations and payoffs. Many fund managers do not use risk models and are ignorant of the absence of diversification of the risk sources in their portfolios. Many don't want to know and prefer a 'pedal to the metal' approach. We acknowledge that all models are 'wrong' but believe that some are useful. The useful ones such as the Northfield model we use (northinfo) allow liquid and illiquid asset forecasts to be combined; have data on bonds as well as equities, allow scenario and stress testing, and incorporate the multi-generational time horizon and planning for periods of investment and consumption that many plan sponsors will have to manage. We conclude that successful wealth management requires carefully nurtured compounding. This compounding can only occur when three forms of risk are carefully managed the exposure to volatility from risk factors and asset-specific sources, the risk of drawdowns, and strategy risk - the risk of being wrong. Portfolios are constructed by focusing risk exposures only in areas the manager has skill. |

|

Funds operated by this manager: Delft Partners Global High Conviction Strategy, Delft Partners Asia Small Companies Strategy, Delft Partners Global Infrastructure Strategy

|

25 Jan 2022 - Airlie Market Outlook, January 2022

|

Airlie Market Outlook, January 2022 Airlie Funds Management 17 January 2022 |

|

Matt Williams, Portfolio Manager, offers his views on the year ahead, the challenges he sees for Australian companies and discusses investments in the portfolio. Funds operated by this manager: Airlie Australian Share Fund |

24 Jan 2022 - Peer Groups

|

Peer Groups FundMonitors.com If you are interested in how a particular fund has performed compared to its competitors or how different sectors have performed against each other, you can use FundMonitors.com to access and compare peer groups. |

|

|