NEWS

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +2.75% in May. Since inception in March 2016, the fund has returned +9.15% per annum, an outperformance of +0.35% relative to the S&P Global Infrastructure TR (AUD) benchmark which has...

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +1.23% in May, outperforming the ASX 200 Total Return benchmark by +0.31%. Since inception in January 2013, the fund has returned +12.57% per annum, an outperformance of +3.63% relative to the benchmark...

Read more...

Performance Report: Collins St Value Fund

The Collins St Value Fund returned -0.56% in May. Since inception in February 2016, the fund has returned +13.68% per annum, an outperformance of +3.99% relative to the ASX 200 Total Return benchmark which has returned +9.69% on an...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund since inception in February 2009, has returned +12.89% per annum, an outperformance of +3.1% relative to the ASX 200 Total Return benchmark which has returned +9.79% on an annualised...

Read more...

Data Dependency and Fiscal Stimulus Complicate Inflation Fight

Financial markets have dealt with a large volume of economic data and communication from central bankers in recent weeks. Despite some overly sensationalised media coverage and short-term predictions, we believe that the central banks'...

Read more...

Performance Report: Bennelong Australian Equities Fund

The Bennelong Australian Equities Fund returned -1.66% in May. Since inception in February 2009, the fund has returned +11.58% per annum, an outperformance of +1.79% relative to the ASX 200 Total Return benchmark which has returned +9.79%...

Read more...

Performance Report: Rixon Income Fund

The Rixon Income Fund rose by +0.98% in May, outperforming the RBA Cash Rate + 5% benchmark by +0.23%. Since inception in November 2022, the fund has returned +12.35% per annum, an outperformance of +3.44% relative to the benchmark which...

Read more...

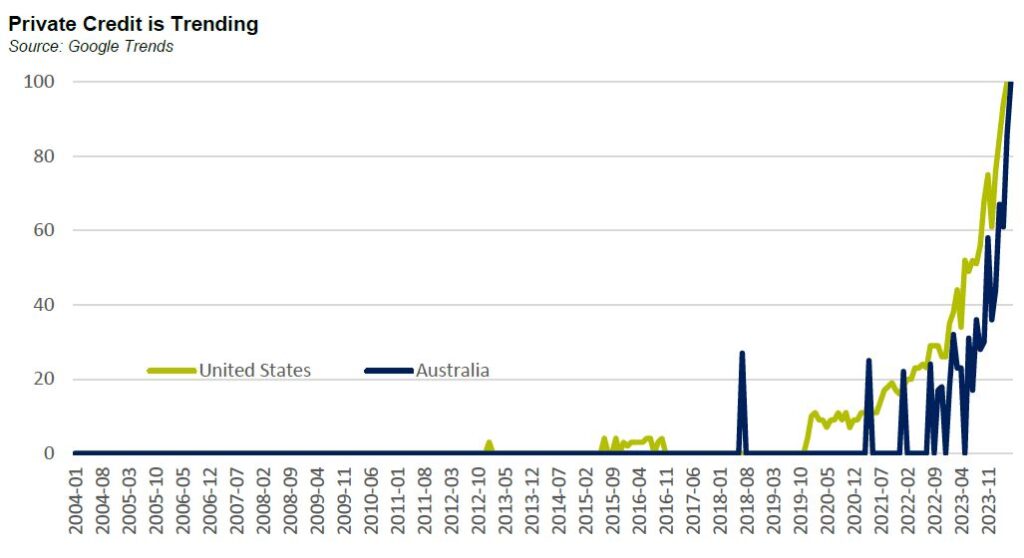

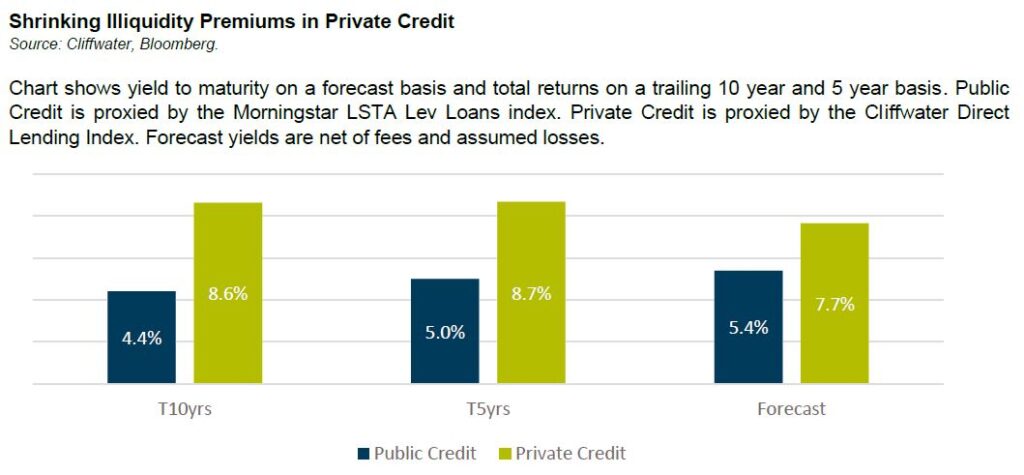

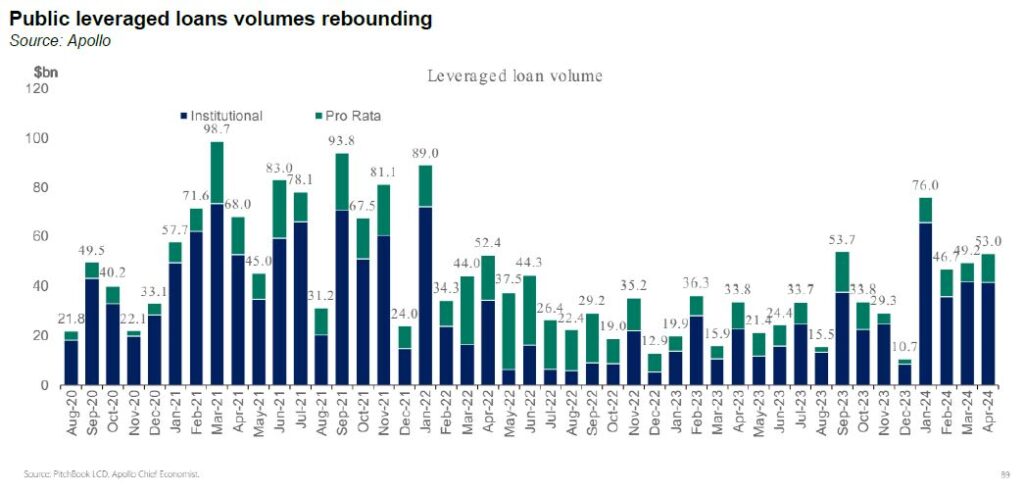

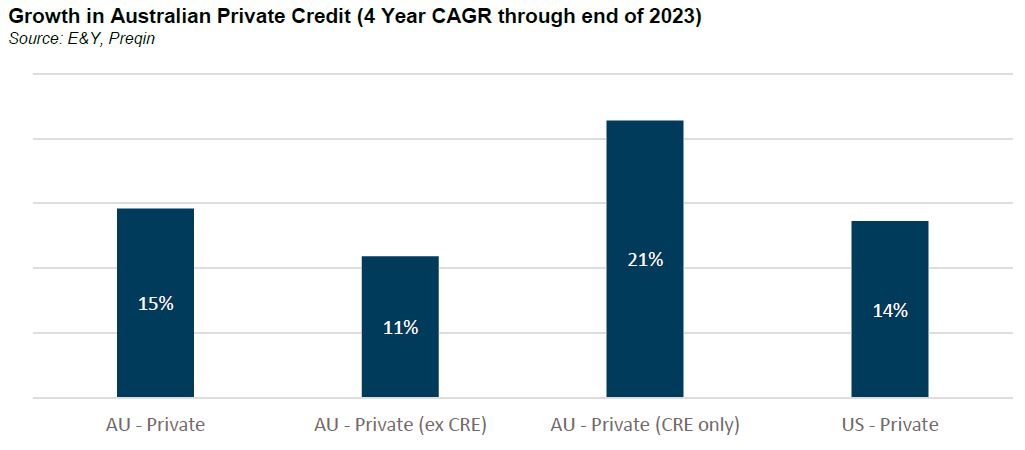

Assessing the "rizz" of the private credit market

The Oxford Word of the Year 2023 was "rizz". An abbreviation of charisma it is used to refer to an individual who has a lot of style and is attractive to others, albeit not just in their appearance. As Dennis Denuto said in the classic...

Read more...

Manager Insights | Digital Asset Funds Management

Chris Gosselin, CEO of FundMonitors.com, interviews Dan Nicolaides on how Digital Asset Funds Management uses crypto market volatility for stable returns and risk management.

Read more...

Hedge Clippings | 07 June 2024

Anyone waiting for the RBA to cut interest rates to mirror the downward movements in Europe and Canada would be well advised to be patient, in spite of Australia's GDP growth slowing to a crawl in the March quarter. In fact, GDP growth of...

Read more...