NEWS

Performance Report: Cyan C3G Fund

The Cyan C3G Fund returned -1.4% in May. Top contributors included Readcloud, Beamtree, Alcidion and Swift Networks, while Big River, Silk Logistics, Quickstep and Birddog were the key detractors. Cyan noted several investee companies in...

Read more...

It doesn't look like the RBA is planning to join the global rate-cuts club soon

Anyone hoping for Australia to join the global rate-cut club is likely to be disappointed in the short term, writes Pendal's head of cash strategies, Steve Campbell

Read more...

Performance Report: PURE Income & Growth Fund

The PURE Income & Growth Fund rose by +0.9% in May, outperforming the S&P/ASX Small Industrials TR benchmark by +1.77%. Since inception in December 2018, the fund has returned +10.79% per annum, an outperformance of +5.96% relative to the...

Read more...

Performance Report: Insync Global Quality Equity Fund

The Insync Global Quality Equity Fund rose by +1.4% in May. Since inception in October 2009, the fund has returned +12.66% per annum, an outperformance of +1.32% relative to the All Countries World (AUD) benchmark which has returned...

Read more...

Performance Report: Emit Capital Climate Finance Equity Fund

The Emit Capital Climate Finance Equity Fund rose by +3.6% in May, outperforming the All Countries World (AUD) benchmark by +2.14%. Since inception in August 2019, the fund has returned +29.13% per annum, an outperformance of +17.86%...

Read more...

Transition trilemma: a reckoning for decarbonisation?

How can infrastructure help with the energy transition?

Read more...

Performance Report: Equitable Investors Dragonfly Fund

The Equitable Investors Dragonfly Fund was flat in May, returning 0.01%. Top contributors included Intelligent Monitoring and MedAdvisor, while MadPaws and Spacetalk were the key detractors. During the month, the Fund participated in...

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose by +0.9% in May. Since inception in October 2009, the fund has returned +10.78% per annum, a difference of -0.56% relative to the All Countries World (AUD) benchmark which has returned +11.34% on...

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund rose by +1.34% in May, outperforming the Barclay Hedge Global Macro benchmark by +0.19%. Since inception in January 2020, the fund has returned +17.34% per annum, an outperformance of +9.47% relative to the...

Read more...

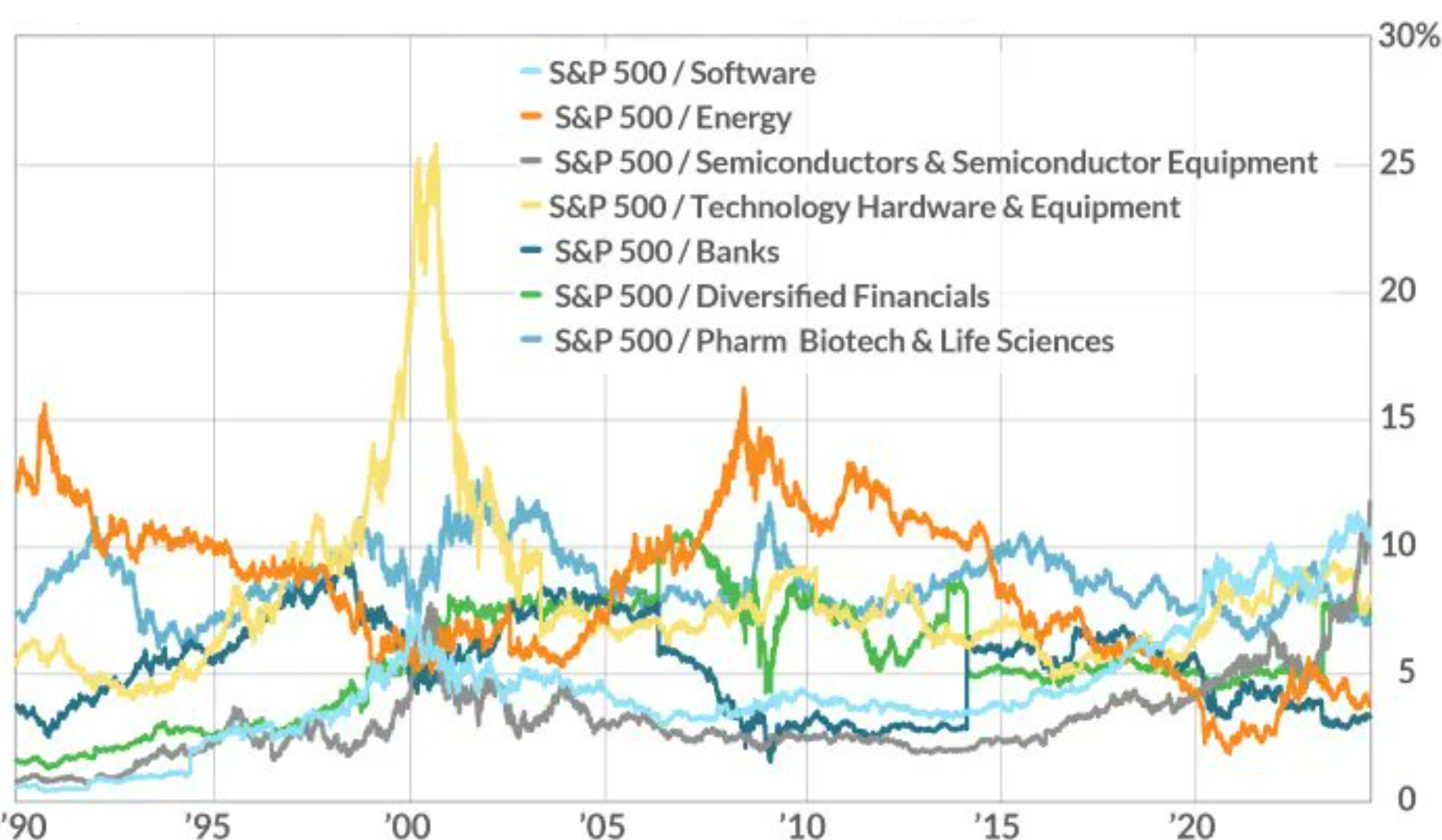

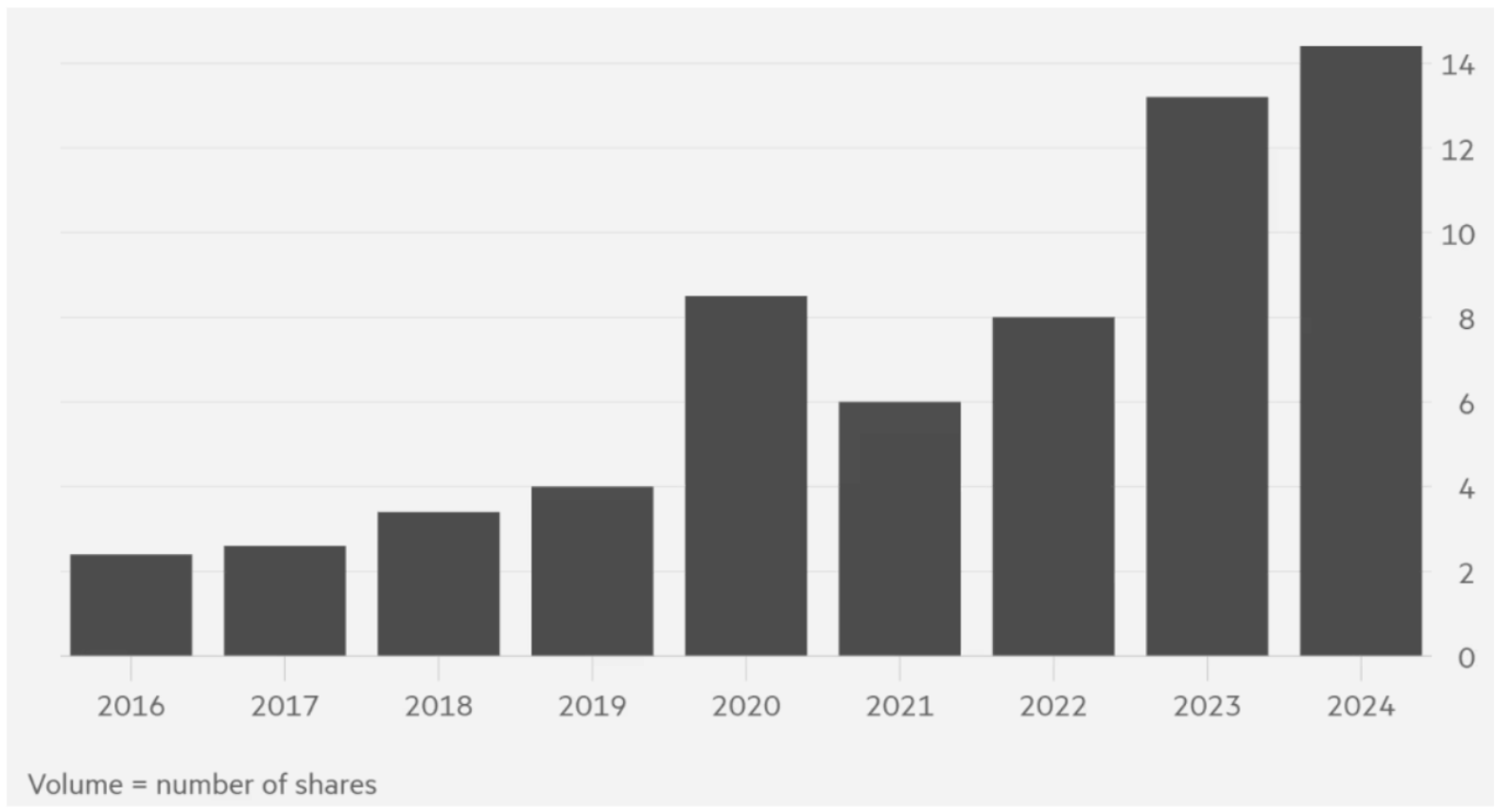

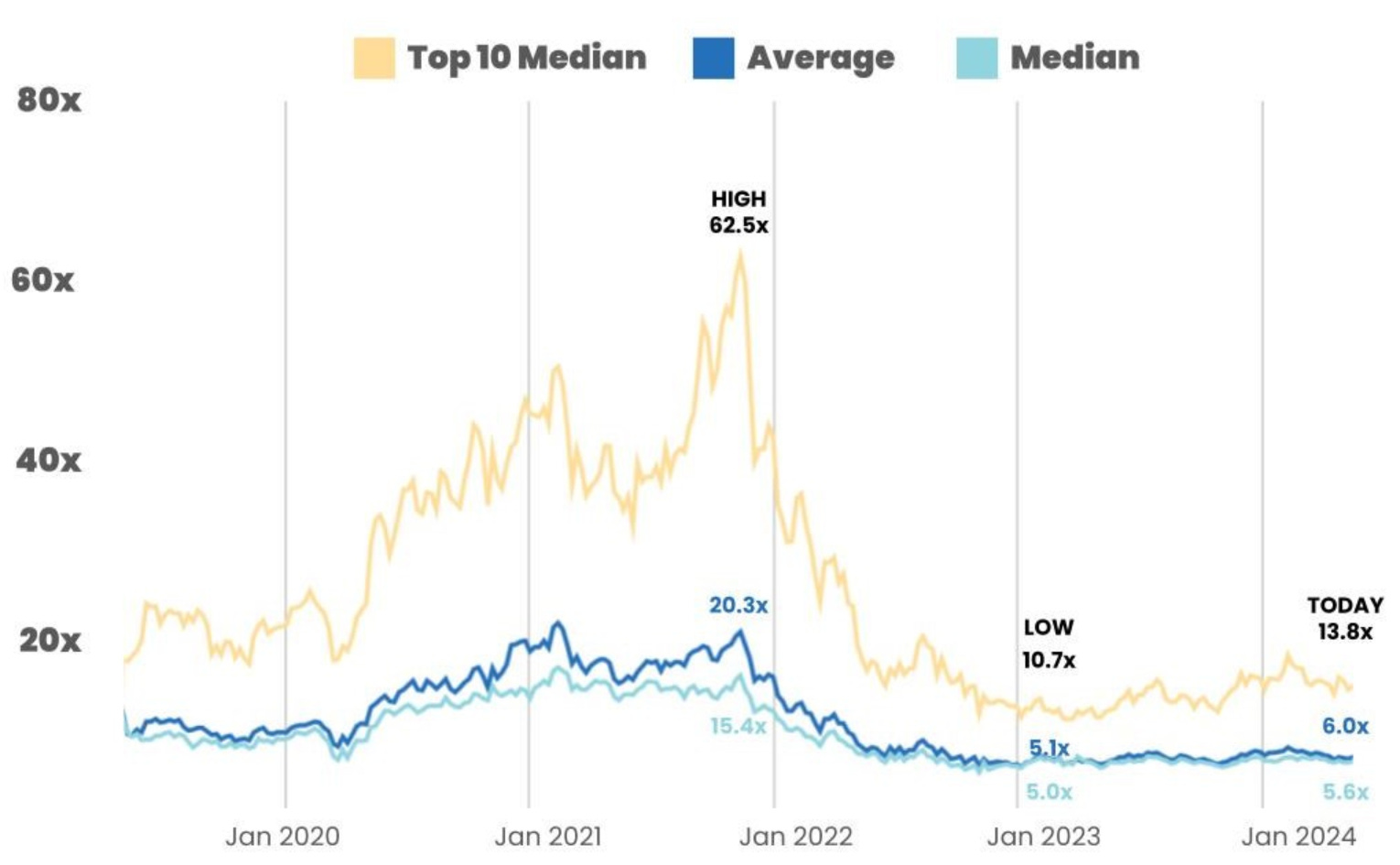

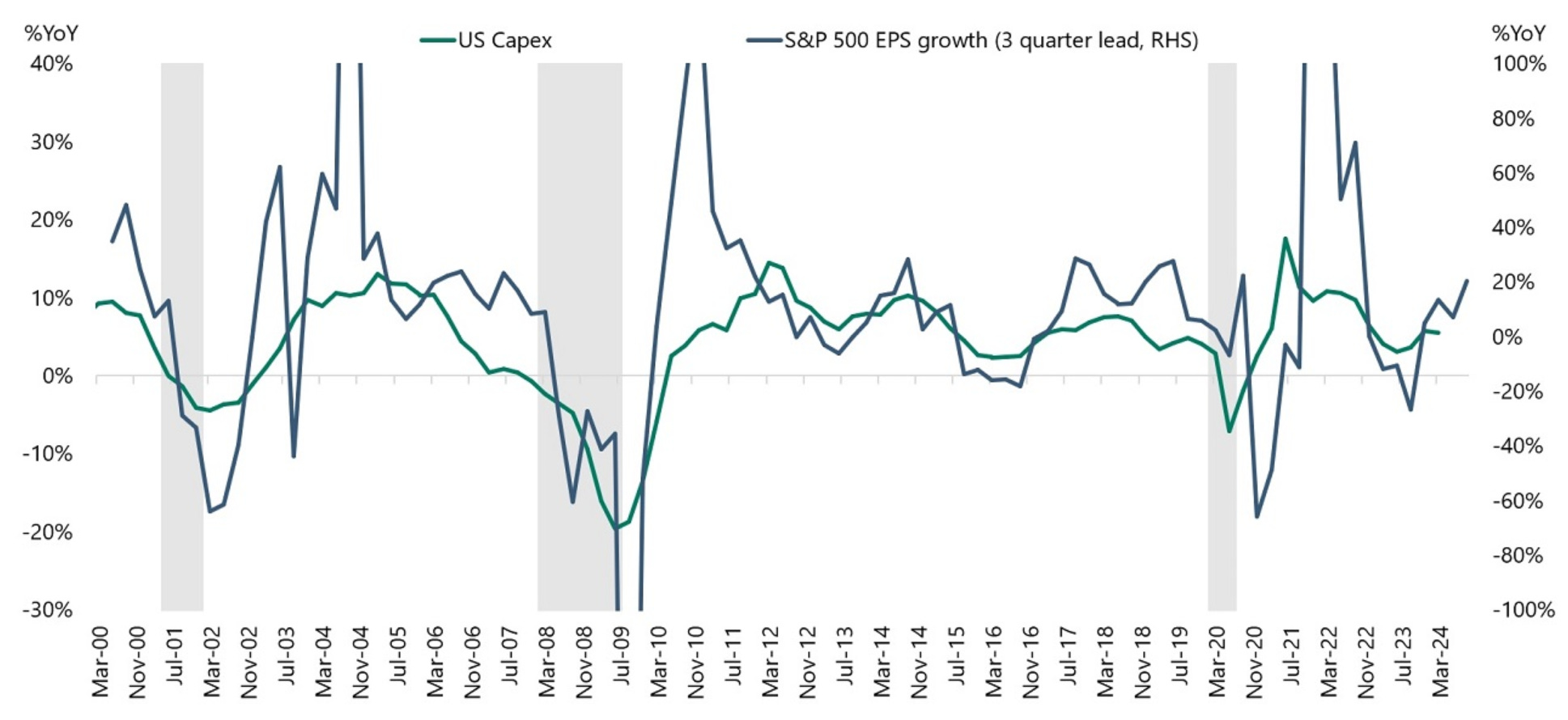

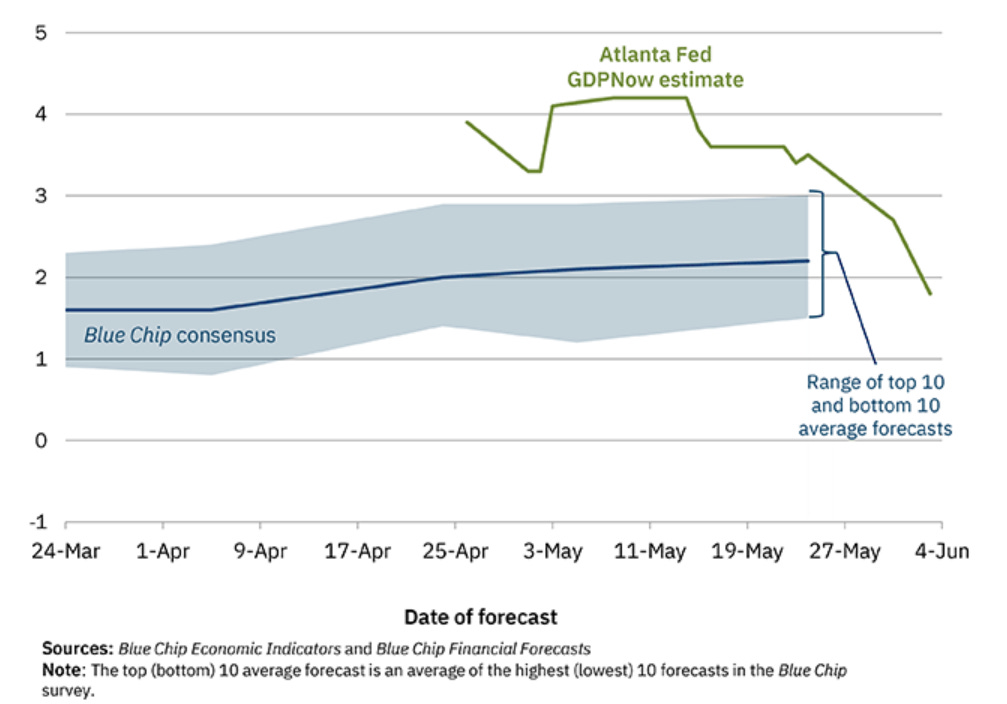

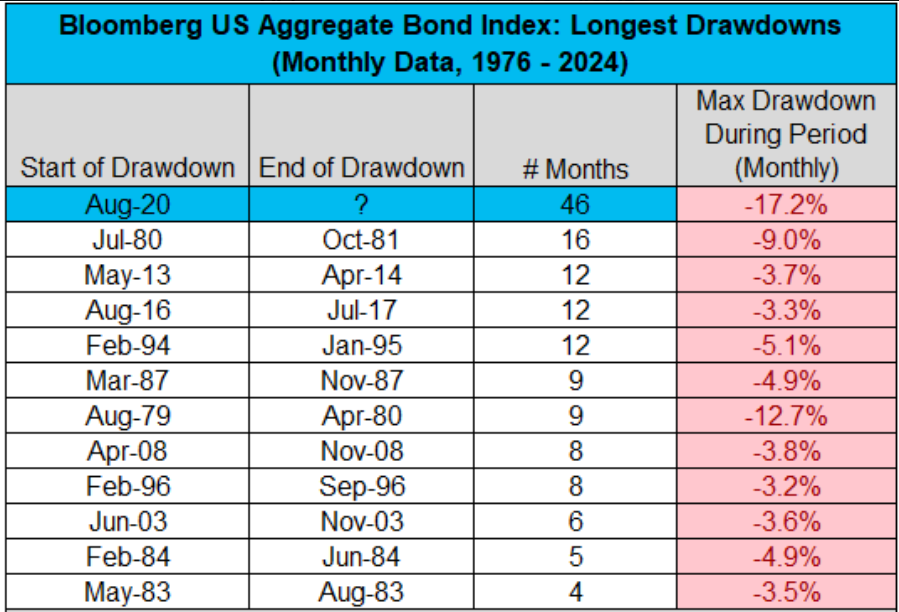

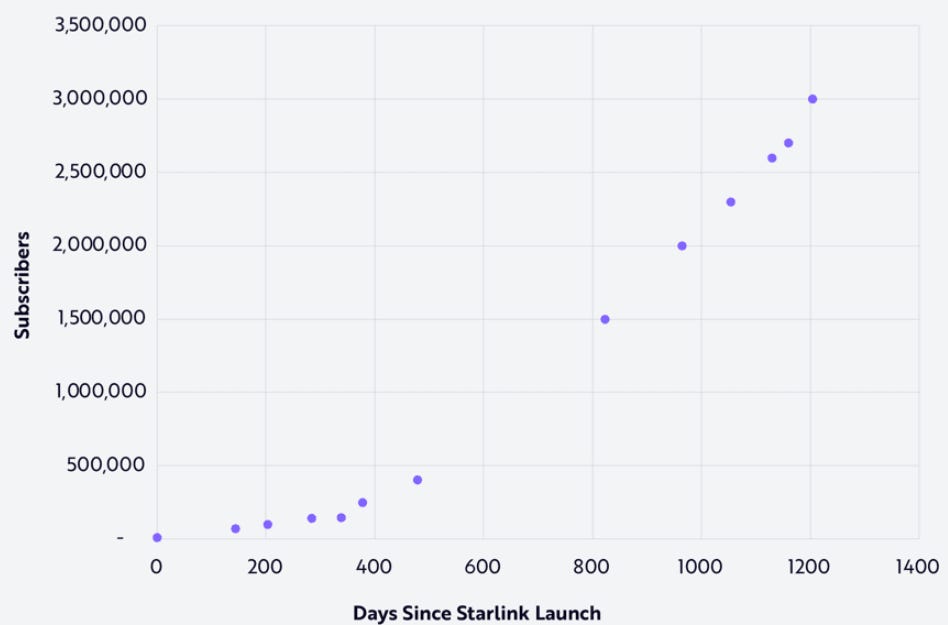

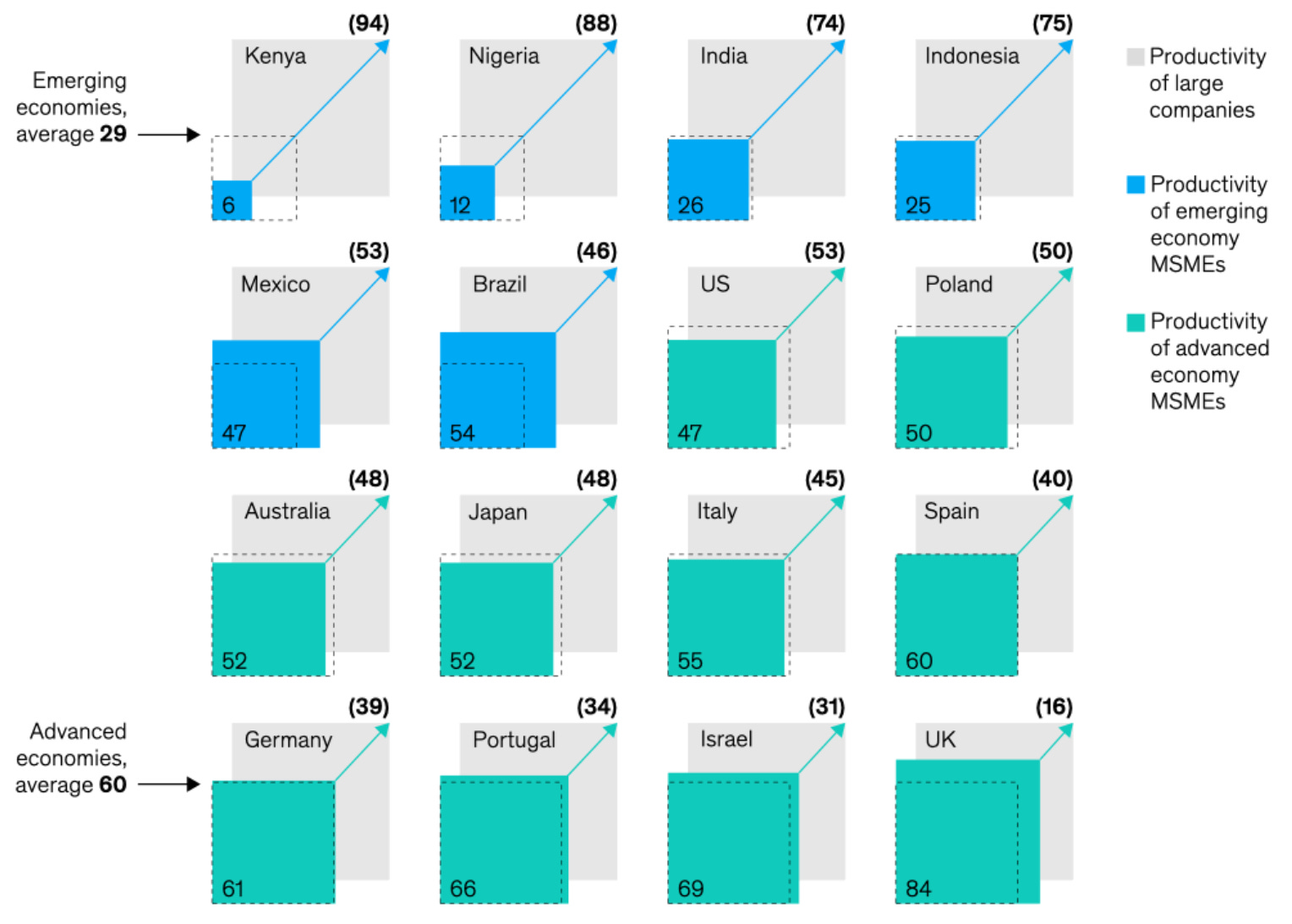

10k Words | June 2024

We have semiconductors snatching the sector title in equities as penny stock activity also rise in the US (not so much in Australia; and no mention of GameStop here, sorry). B2B SaaS growth moderates - as have tech EV/Revenue multiples -...

Read more...