NEWS

Can the RBA be patient with inflation?

Will May's monthly inflation data push the RBA to hike again? If it can be patient, says Pendal's head of government bond strategies Tim Hext, some relief is at hand.

Read more...

Performance Report: Digital Income Fund (Digital Income Class)

The Digital Income Fund (Digital Income Class) rose by +1.88% in June, outperforming the Bloomberg AusBond Composite 0+ Yr benchmark by +1.11%. Since inception in May 2021, the fund has returned +23.48% per annum, an outperformance of...

Read more...

Attention shifting from inflation to the growth outlook

We continue to expect inflation to return to around 2% and the key investor debate to shift back to the growth outlook. Our expectation remains a soft landing, but we outline the main risks investors should watch.

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +0.28% in June. Since inception in February 2009, the fund has returned +12.83% per annum, an outperformance of +3.03% relative to the ASX 200 Total Return benchmark which has...

Read more...

Investment Perspectives: Why are we listening to central banks?

Since the global financial crisis, most western economies have relied on central bank policy to manage both inflation and employment.

Read more...

Hedge Clippings |19 July 2024

Last week's Hedge Clippings commentary focused on global politics, particularly the US presidential election. Biden remains in the race despite declining Democratic support, while Trump, bolstered by his MAGA base, continues to dominate.

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) since inception in March 2016, has returned +8.4% per annum, a difference of +0.13% relative to the S&P Global Infrastructure TR (AUD) benchmark which has returned +8.27% on an annualised basis...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +1.06% in June, outperforming the ASX 200 Total Return benchmark by +0.05%. Since inception in November 2009, the fund has returned +9.47% per annum, an outperformance of +1.45%...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.82% in June, outperforming the RBA Cash Rate + 5% benchmark by +0.07%. Since inception in April 2018, the fund has returned +11.76% per annum, an outperformance of +5.16% relative to the benchmark...

Read more...

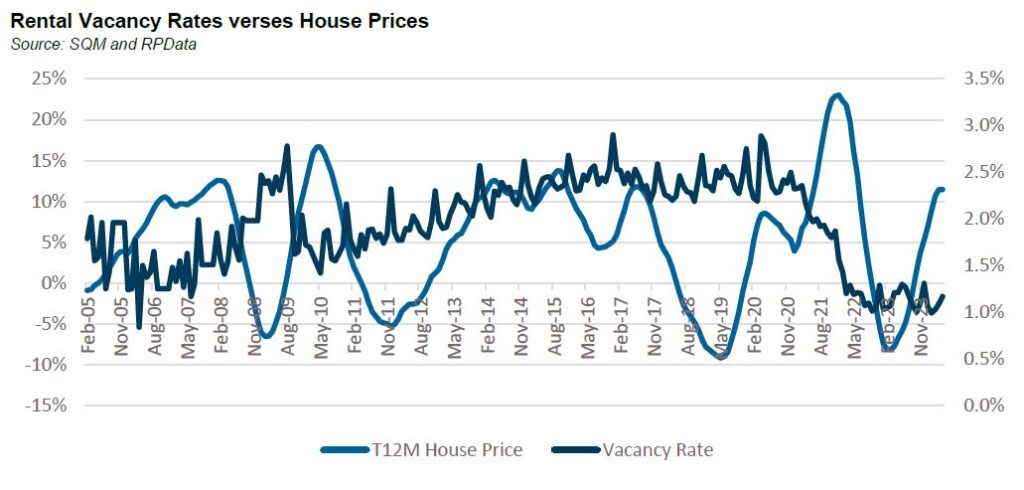

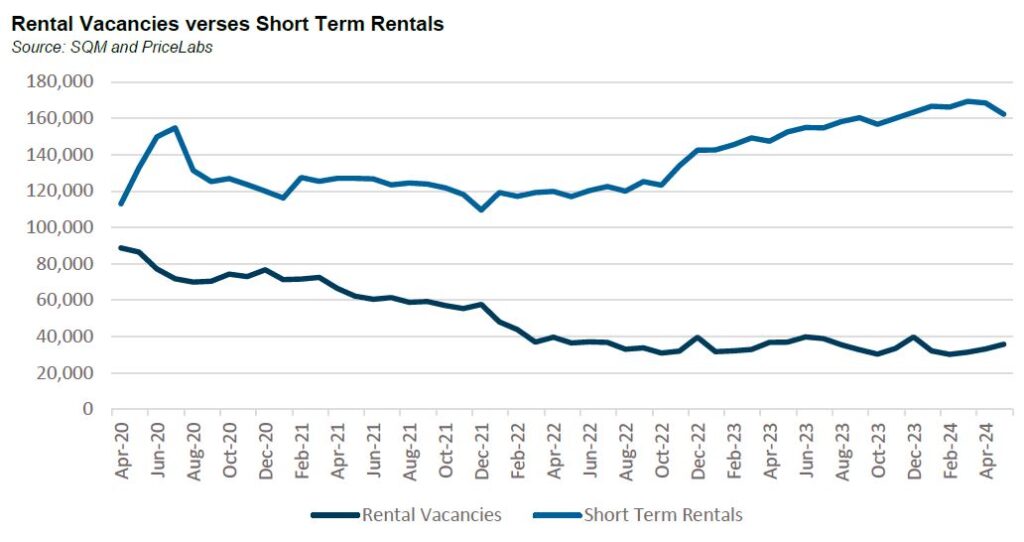

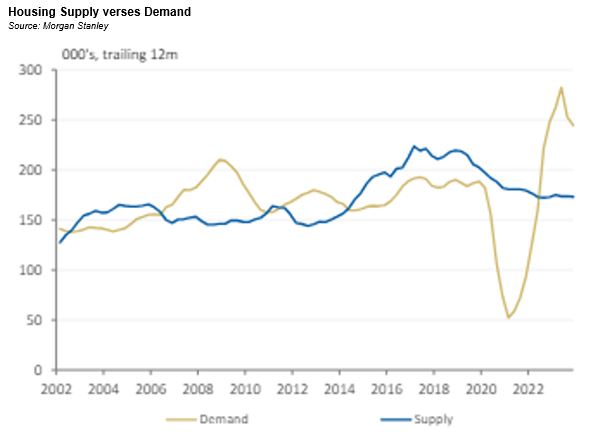

Interrogating the bull case for housing

Over the past few months, we've been puzzled by the strength of the bullish tone around house prices. Puzzled because the argument supporting house prices seems to be hanging on the lack of supply/strong migration creating a supply demand imbalance.

Read more...