NEWS

9 Aug 2024 - Fixed income: the likely impact of rates, inflation and a Trump presidency

|

Fixed income: the likely impact of rates, inflation and a Trump presidency Pendal July 2024 |

|

THE services side of the economy - particularly wages and rental inflation - have held up prices in recent times. But forward indicators monitored by Pendal's income and fixed interest team show the drivers of these two factors weakening. That means inflation in developed markets should continue to fall, allowing central banks globally to start cutting rates, argues Pendal's head of credit and sustainable strategies, George Bishay. "That means central banks globally can start cutting rates," he says. "My view is that central banks will cut rates because inflation is coming down -- not because we are going into recession." It's an important distinction, because when an economy goes into recession, bonds usually perform well, while credit and equity markets can underperform. "If inflation is falls, that's a bullish environment for bonds as central banks will cut cash rates and interest rates in general should come down. "This is also bullish for credit and equity markets." What a Trump White House meansThe key risks to this view is if oil prices rise or if Donald Trump beats presumptive Democratic nominee Kamala Harris in the US presidential election later in the year, Bishay says. "If Trump wins the election, will he have the ability to change policy? Will he have a majority in both houses of Congress? "If he does, then that's problematic for bonds because ultimately that's likely to be inflationary," Bishay says, nominating tax, immigration and trade as key areas of policy to watch. The impact of a Trump Presidency is more skewed towards longer-term bonds because his policies would likely have a medium-term impact on inflation, he says. "The short end continues to perform because central banks will be easing rates as current inflation comes down." Active management remains important for fixed incomeWith so much uncertainty in the market, active management of credit portfolios is critical. "Most credit managers in Australia are buy-and-hold managers. In periods such as Covid, performance of those strategies can get hammered before eventually recovering. "Volatility of their returns can be quite high. "We prefer to actively de-risk and re-risk our credit exposures, based on a top-down process. "If we have concerns about the macro environment, we will reduce risk across the board on credit exposures. That tends to support outperformance because it minimises downside risk. "When we have more confidence in the market, we re-risk and participate in the upside benefit." The three main pillars of Pendal's top-down process are a qualitative view, quantitative models and technical analysis. "When the three pillars line up, we de-risk or re-risk the portfolios and that's been incredibly powerful."

Author: George Bishay |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

8 Aug 2024 - The RBA's August decision: Insights from Nick Chaplin of Seed Funds Management

|

Chris Gosselin, CEO of Australian Fund Monitors, speaks to Nichols Chaplin, Director and Portfolio Manager at Seed Funds Management. Topics covered include: interest rates and inflation; US markets; volatility in equity markets; and bonds and hybrids.

|

||

7 Aug 2024 - Glenmore Asset Management - Market Commentary

|

Market Commentary - July Glenmore Asset Management July 2024 Equity markets were stronger in June. In the US, the S&P 500 rose +3.5%, the Nasdaq increased +6.0%, whilst in the UK the FTSE100 declined -1.3%. The US markets were boosted by growing confidence that inflation is slowing, and interest rate cuts are on the horizon. During the month, the Canadian central bank cut its key interest rate by 25 basis points to 4.75%, making it the first member of the G7 to lower rates. Domestically, the ASX All Ordinaries Accumulation Index rose +0.7%. Top performing sectors included financials and consumer staples, whilst materials were the worst performer, due to concerns about the Chinese economy and its demand for commodities. In Australia, inflation continues to track higher than targeted by the Reserve Bank (RBA). Given this high inflation and recent expansionary fiscal policy from the federal government, this potentially sees the need for the RBA to lift rates in August, however, to date it appears equity investors on the ASX are taking the view that the cycle of rate hikes is almost over. In addition, we would note valuations across a wide range of small to mid-cap stocks on the ASX are still very attractive, which should lead to investors being well rewarded over the next few years. Funds operated by this manager: |

6 Aug 2024 - Australian Secure Capital Fund - Market Update

|

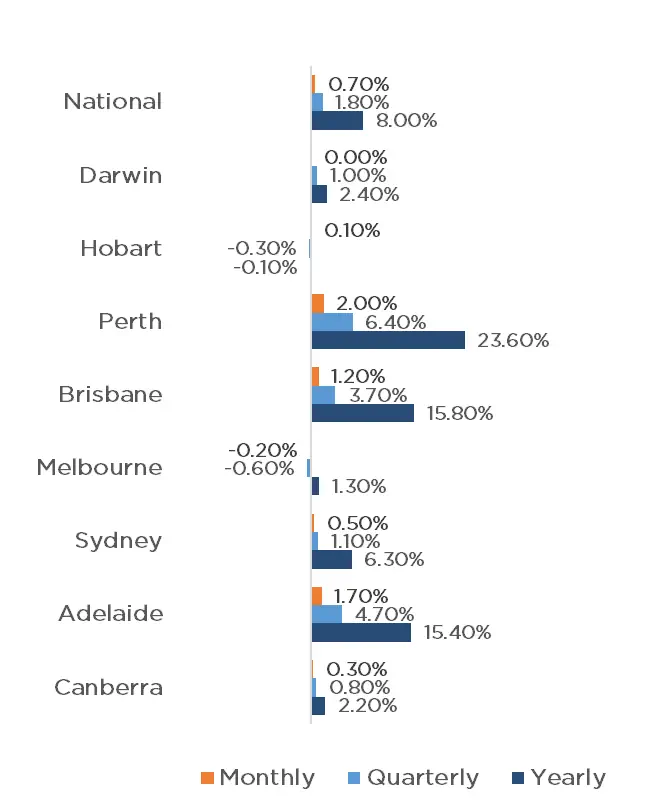

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund July 2024 Property prices across the capital cities have risen yet again, bringing the 17th consecutive month of price growth with June's 0.7% increase, taking growth to 8% across the nation for the 2023-24 Financial year. Yet again, Perth has experienced the largest growth with a further 2% increase, followed closely by Adelaide with 1.7% and Brisbane with a 1.2% increase. Sydney, Canberra and Hobart also experienced growth, albeit it to a lesser degree, with 0.5%, 0.3% and 0.1% respectively. Property prices in Darwin remained stable, whilst Melbourne saw a reduction of 0.2%. The financial year data is nearly all positive, with all capital cities experiencing growth, excluding Hobart which received a small reduction of 0.1% for the year. Perth, Brisbane and Adelaide all experienced growth well into the double digits, with Perth leading the way with a mammoth 23.6% increase, followed by Brisbane and Adelaide with 15.8% and 15.4% respectively. Sydney, Darwin, Canberra and Melbourne also finished the year in the positive, with 6.3%, 2.4%, 2.2% and 1.3% respectively. Growth wasn't just experienced in the capitals, with the regions also increasing by 7%. Property Values as at 30th of June 2024

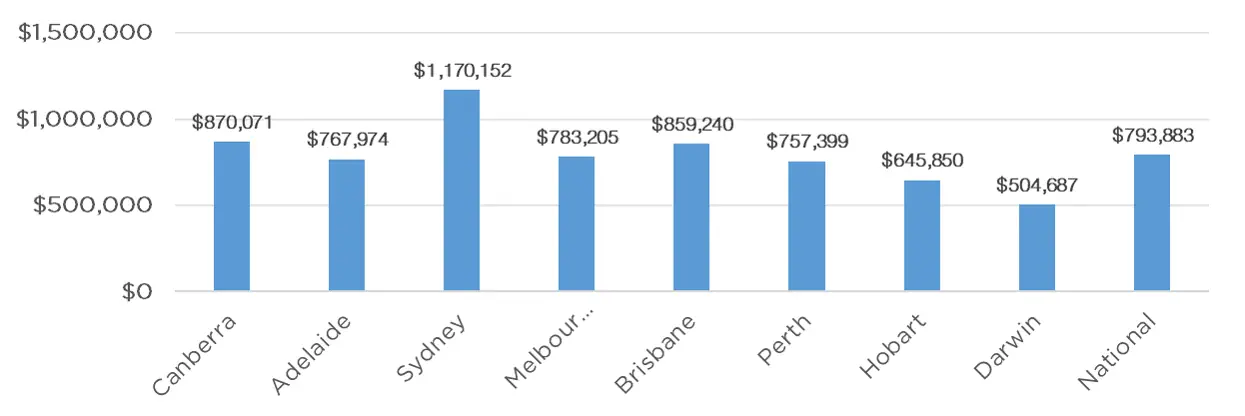

Median Dwelling Values as at 30th of June 2024

Quick InsightsLarger LoansThe average new owner-occupier home loan is at $626,055 nationally, hitting a record high, as the growth housing markets of Perth, Brisbane and Adelaide surge higher, according the latest official lending figures. "It's astounding to think owner-occupiers are, on average, taking out larger loans than ever before despite the fact the cash rate is sitting at a 12-year-high.", said Sally Tindall, research director at comparison website, RateCity.com.au. Source: Australian Financial Review

Construction Costs & Increasing Interest RatesHigh interest rates and construction costs are now choking off the supply of new housing. High construction costs in particular are being singled out amid a complex mix of factors that have pushed up the cost of building in most capital cities. "There has been some relief in access to inputs and labour, and in the prices of some early-stage inputs, but labour costs remain elevated and the regulatory burden high.", investment banking firm Barrenjoey's chief economist Jo Masters said. Source: Australian Financial Review Author: Filippo Sciacca, Director - Investor Relations, Asset Management and Compliance Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

5 Aug 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Regal Resources Long Short Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Regal Private Credit Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Regal Resources High Conviction Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Regal Tactical Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Prime Value Diversified High Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Microequities High Income Value Microcap Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Alphinity Global Sustainable Equity Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 800 others |

5 Aug 2024 - Manager Insights | Argonaut

|

Chris Gosselin, CEO of FundMonitors.com, speaks with David Franklyn, Executive Director & Head of Funds Management at Argonaut. The Argonaut Natural Resources Fund has a track record of 4 years and 6 months. The fund has outperformed the S&P/ASX 300 Resources TR benchmark since inception in January 2020, providing investors with an annualised return of 27.27% compared with the benchmark's return of 8.73% over the same period.

|

2 Aug 2024 - Hedge Clippings | 02 August 2024

|

|

|

|

Hedge Clippings | 02 August 2024 Central bankers love to use the term "a narrow path" as they manage their respective economies delicately between manageable growth, and the risk of recession. With the single tool of monetary policy to balance their twin objectives of inflation and employment, there's always the risk they move too quickly - or not quickly enough - and so miss the so called soft landing that the market craves. The US Fed looked as if they were on track to do that, but the market has become impatient. Just a day after Jerome Powell held rates steady but indicated they should be able to start easing in September, the ISM manufacturing index came in lower than expected, and at 46.8% indicating the economy was contracting. Suddenly the market's thinking bye-bye soft landing, hello possible recession. This couldn't come at a worse time for markets, particularly the NASDAQ and the Magnificent Seven, which were already seeing signs of a pull back from nosebleed valuation territory, coupled with concerns over reporting season - or at least missing analysts' estimates. Falls in the US of course lead to falls elsewhere, and Australia is no exception. To make matters worse the RBA has its own problems, although this week's CPI numbers have at least taken the pressure off them to raise rates at next week's meeting. Not that the CPI numbers were particularly good - June quarter up 1% and 3.8% over the past 12 months - they just weren't bad enough for the Board to raise rates on Tuesday as had been feared. One problem for the RBA is that Australia has a two speed economy - or at least two sections of the community that are faring very differently. At one end - say 20-25% - are doing it tough and struggling to make ends meet, and, as we hear continually, the government is doing everything it can to save, or at least support them - tax cuts, wage rises, energy and power support, etc. At the other end of the spectrum are those who have either paid off their mortgage, or at least paid it down to manageable levels, are comfortably retired, or are higher paid, and for whom inflation of 4%, and/or higher interest rates, aren't creating the same issue, partly because they're also beneficiaries of the government's generosity or stage 3 tax cuts. Of course there are those in the middle, and overall the average, who makes up the economy. It's the old conundrum: When your feet are in the freezer, and your head in the oven, your temperature is probably average. The next challenge for investors and fund managers reporting season in the US, and the ASX, where it runs through to the end of August. This is the period when Warren Buffett's famous quote "Only when the tide goes out do you discover who's been swimming naked..." comes into play. Missing market expectations - particularly when valuations are sky high - can result in savage sell offs. Overnight in the US Intel fell 17% after suspending its dividend, Snap also fell 17%, while Amazon fell 6% on disappointing quarterly sales and sales guidance in spite of net sales which are expected to grow by between 8% and 11% compared to Q3, 2023. Local hero, but NASDAQ listed Atlassian, fell 13% after close of trading, as its revenue projection is only for an increase of 16% this FY, having previously advised it would be 20% per year for 3 years. This week's edition of "The Last Word" covers all this and more. The Last Word In Episode 3 of "The Last Word", Chris Gosselin and Manny Anton delves into the latest market trends and economic developments. This episode covers key movements in the US, the impacts of recession fears on the US market, and the upended outlook for the US election following Joe Biden's withdrawal. News & Insights New Funds on FundMonitors.com Manager Insights | Argonaut Trip Insights: The US | 4D Infrastructure July 2024 Performance News Insync Global Capital Aware Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

2 Aug 2024 - Rage against the AI machine?

1 Aug 2024 - China Autos: Finding the fast lane

|

China Autos: Finding the fast lane Ox Capital (Fidante Partners) July 2024 BYD starting in pole position!The rise of the Chinese auto industry is nothing short of remarkable. Thirty years ago, China did not have an auto industry of any scale. China produced only 5,000 passenger cars in 1985! One of the earliest joint ventures (JV) between a foreign car maker and a Chinese company was the Volkswagen JV in Shanghai. Its signature car was the Santana which quickly became a best seller given its superior technology and reliability to competitive offerings at the time.  Fast forward to 2000, China had fewer than 20 million cars on the road, a very low rate of car ownership given its billion plus population. This started to change post the joining of the WTO. With the economy taking off, many other foreign car companies joined in the fray forming JVs in China. These plants were run by foreign management, and were generally highly profitable, as demand was strong, car prices were high and labour costs were low. The blossoming of the domestic auto industry enabled the development of the automotive supply chain. As the Chinese car market grew in scale, manufacturing of key components, for example engines and gear boxes, moved to China  Foreign joint venture partners were typically state-owned companies, with standout successes including Shanghai Auto and Guangzhou Auto. Both companies were able to develop their own car brands, effectively competing in the market. For instance, Shanghai Auto acquired the MG brand and has successfully exported it to other countries. The more enterprising, privately-owned auto manufacturing upstarts have proven to be tougher competitors. After a decade of intense competition, hundreds of private automakers have been whittled down to a handful of survivors. These operators have gained scale and technological knowhow, are extremely cost-conscious and innovative. Notably, the fast iterative product cycles meant the improvement in quality was rapid. Geely Auto (in Chinese Geely means prosperity) quickly accumulated technological knowhow. This was achieved through mergers and acquisition, rigorous investment in research, and sheer hard work. For example, they acquired several companies that have fallen into difficult times - including Volvo, Lotus, London Electric Vehicle Company (London cabs), Renault drivetrain JV amongst others. Now they have developed brands of their own, such as Lynk&Co, Polestar, Zeekr, the Smart Car JV with Mercedes. The Polstar 5, needs no introduction, is in fact ultimately owned by Geely.  One of the highly automated auto plants in China

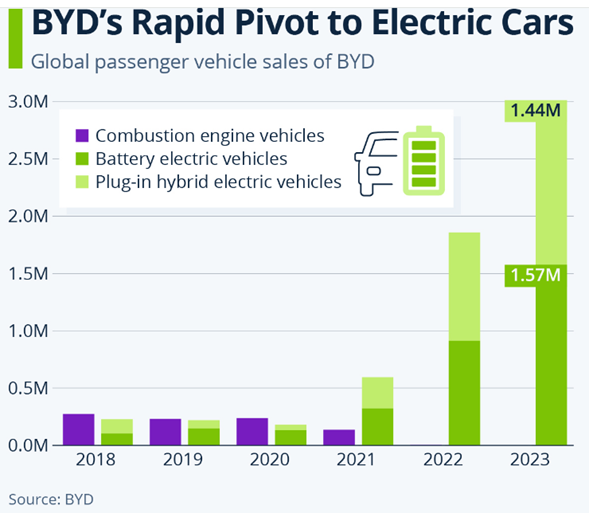

Apart from Geely, another surprising success story is BYD. What's remarkable is that BYD started out as a manufacturer of lithium batteries for PCs and smartphones. The company then chose to transition into electric vehicle production and has now become the largest EV maker in both China and the world!  BYD is early in its growth trajectoryFirstly, BYD spends around USD8 billion a year on research and development. Its product quality and technological leadership is unparalleled. BYD's latest plug-in hybrids have superb fuel efficiency of around 2.9L per 100km. Fully charged and a full tank of fuel, these BYDs can travel in excess of 2000km according to online bloggers! Second, BYD is only getting started in its ambition to conquer the auto market in China and abroad. Despite its success, BYD has only a 10% market share in China's passenger car market. With cost and quality leadership, its domestic Chinese sales is likely to be resilient in coming years. Further, export momentum is strong, with BYD only exporting around 300,000 cars a year, growing at 150% year over year in the month of June. To achieve long term success in global markets, BYD is not standing still, and it is building manufacturing plants in Hungary to supply Europe, along with Thailand and Mexico for ASEAN and Latin America, respectively. Third, prices of BYDs sold outside of China are typically at significant premium to the domestic market. While this higher price tag may partially be a result of transportation cost and tariffs in some cases, profitability per car is likely to be significantly superior in the export market. This is an interesting insight that will drive growth in profitability for BYD going forward. An older BYD rendition.  Twenty years after its first car, BYD is now gaining significant tractions in the global market through a few of its model. For example, BYD Seal 06, the current best-selling sedan, is growing rapidly overseas. Starting price tag in China USD25,000!  Funds operated by this manager: Ox Capital Dynamic Emerging Markets Fund Important Information: This material has been prepared by Ox Capital Management Pty Ltd (Ox Cap) (ABN 60 648 887 914) Ox Cap is the holder of an Australian financial services license AFSL 533828 and is regulated under the laws of Australia. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriaten |

31 Jul 2024 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]