|

Reduce your risk and pick outstanding companies Emma Fisher, Airlie Funds Management September 2021 Despite the record reporting season past and the major wall of cash returned to investors this year, we at Airlie can't help but feel things in markets are a little gloomy. We believe that this is due to two sources of dismay.

In cutting through this doom and gloom we think it is important to talk about uncertainty and risk. It may seem obvious, but it is worth pointing out that uncertainty and risk are different concepts. We think the market is pretty bad at distinguishing between the two and punishes both evenly. Uncertainty is not knowing what is going to happen in the future. Put this way, you realise uncertainty is a fact of investing and ultimately a fact of life. In our view, uncertainty in markets creates opportunity. We're always looking for the uncertainty that may create a mispriced asset. What we don't like is risk. Risk is the chance of a permanent loss of capital and in our view, often comes down to two reasons:

At Airlie, we use a four-stage investment process tailored specifically to take advantage of uncertainty while minimising risk. #1 Focus on financial strengthStrong balance sheets The first place we always start is with a focus on the balance sheet. Making sure that the financial position of our companies is rock-solid is the first way that we limit the permanent loss of capital. These businesses can weather the storm of whatever markets throw at them and help portfolios perform through all cycles. When we consider the share market as a whole, it's important to note that balance sheet risk is much lower than it has been historically. Over the last few decades, net debt to EBITDA has had a median of 2.5 times. Right now it's much lower at about 1.9 times. This is a good sign. While we believe valuation risk is highly elevated right now, the lowered level of balance sheet risk is in essence telling us to proceed with caution at the moment. Heading into the GFC, both measures of risk were highly elevated. If you were to consider it as two signals - we had both lights showing red. Right now we see one showing orange and one showing green.

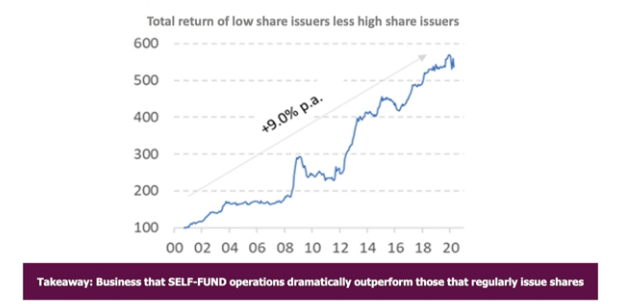

Self-funding businesses The other element of financial strength we like to consider is whether the business is self-funding its operations. This is simply because it has been proven that over the long term that these businesses outperform. They are able to fund their own growth profile through earnings and do not dilute shareholder capital. Alternatively, the businesses that are constantly tapping the market for equity to sell investors the dream and fund the business growth underperform, as seen below. #2 Don't overpayWhen investors reflect on the 2001 tech bubble, it is important to remember that it wasn't only tech stocks caught up in the hype. If you bought Disney, Coca-Cola or Walmart at their peak during that period, you would have had to wait 11 to 16 years to get your money back. Investing during peak periods is a real risk to a permanent loss of capital. Now we don't believe that we are at similar levels in the Australian market but we do see pockets of extremely optimistic valuations. As the risk-free rate falls, the multiples you have to pay for future cash flows increases. Right now markets have never been more expensive since yields have never been this low. In our view, if you're investing in the most expensive parts of the market, you're taking a bet against bond yields. And that's not a risk we are comfortable taking. #3 Buy quality businessesAt Airlie, we see quality businesses as those with a high return on capital. This is because, for every dollar that is earned by a business, a greater portion will be returned to shareholders and not lost in capital expenditures. The issue that unfortunately presents itself here, is that high-quality businesses can often be the most expensive. Therein lies the greatest challenge of this current market and what we look for in our investments - which are the quality businesses available at good prices. We believe there are three main reasons why a high-quality business may not trading at high valuations.

The best example of a past "jewel in the crown" business is Wesfarmers (ASX: WES). It was not until the demerger of Coles that Bunnings was able to shine as one of the best businesses in Australia. Bunnings generates a return on capital of more than 70%, so when Bunnings went from a third of WES' earnings to 70%, Wesfarmers re-rated. We believe a similar unlocking of value is happening with Tabcorp (ASX: TAH). We believe Tabcorp's lottery business deserves a very high valuation. This business has proven to be a resilient growth story over time. Their growth is underpinned by state monopoly licenses that run for decades in most states and an ever-increasing spend on lottery tickets online, meaning they no longer have to pay a commission to the newsagent. The issue is that the wagering division of the business proves to be somewhat of a problem child. The wagering arm doesn't offer the same attractive low cost of capital, and many investors who would be interested in the lotteries business do not want exposure to the gaming division. So the answer the company is pursuing here is a de-merger. We think in about a year's time Tabcorp will be worthy of a significant re-rate. #4 Find good managementThe final factor of focus in reducing risk is finding businesses with good management teams and founder-led businesses. We like these companies because it often means that management tends to focus on the long term, their interests are aligned with shareholders, and they are passionate about the business. An example of one of these businesses we are really excited about is PWR Holdings (ASX: PWH). PWR is also an example of a company we think is currently flying under investor's radar. Most of the company's revenue comes from selling cooling systems to motorsports companies. The founder and CEO, Kees Weel, started his business as a mechanic in the 70s. After a while, he decided he would give making radiators a try. Now, 40 years later, he's making the best radiators in the world and is the radiator supplier of every Formula One team. But it's not only the motorsports arm that excites us. In our view, the most exciting reason to own PWR is the growth happening in the emerging technologies division.

They are currently working on the development of cooling systems for electric vehicles. This is likely to be a huge secular growth area for the company over the next few decades. Additionally, the team is working with a number of exciting companies to develop cooling systems in aerospace and defence applications. The passion their CEO Kees Weel has for the business and his staff is why we love founder-led businesses. Earlier this year we had a chance to visit the PWR headquarters in the Gold Coast and at the first stop of our site tour, Kees presented us all with a copy of the company's yearly cookbook. Kees showed us the on-site cafeteria that had been built so that the welders and engineers could have healthy, freshly cooked meals for free. That sort of passion for the culture and experience of the team is really infectious and something we love to see in the companies we invest in. Summing it all upIn conclusion, we want to highlight the importance of the difference between uncertainty and risk. While we love uncertainty, like the doom and gloom we see in markets, we hate risk. In our view, these four factors are the key to reducing risk and creating long term wealth. Invest where fair value exceeds market price We identify Australian companies based on their financial strength, attractive durable business characteristics and the quality of their management teams. The above article is a summary of the recent webinar hosted by Matt Williams and I. |

|

Funds operated by this manager: Airlie Australian Share Fund |