|

Climate-related Financial Disclosures: A step toward greater transparency in corporate sustainabilit Janus Henderson Investors August 2025 Liz Harrison, Fixed Interest Strategist - ESG in the Australian Fixed Interest team, discusses the Climate-related Financial Disclosure initiative and how the mandated sustainability reports will be used to enhance transparency and accountability. Sustainability reporting thresholds by group

Source: Janus Henderson, Australian Accounting Standards Board (AASB) Australia has joined many global counterparts by introducing mandatory sustainability reporting for companies and other select legal entities. This initiative, the Climate-related financial disclosure (CRFD), was mandated by the Australian Government in partnership with the key regulator Australian Securities and Investments Commission (ASIC). CRFD began at the start of 2025 and will be implemented over a three-year period. Larger companies are required to comply first, with the following criteria set for mandatory reporting by the end of the third year:

For asset owners, mandatory reporting will apply only to those with at least $5 billion in assets under management (AUM) and that are registered schemes, registrable superannuation entities, or retail corporate collective investment vehicles (CCIV). This requirement for asset owners will commence in Group 2, starting after July 1, 2026. The timing for the release of these reports will be aligned with the start of a company's or asset manager's financial year reporting. The earliest reports from the first group are expected at the beginning of 2026, applicable to those whose reporting period aligns with the calendar year. While this new regulation will become a legal requirement, many companies have already been doing voluntary reporting in their sustainability reports. It has been reported that this is the case for 82% of the ASX2001. For those not familiar with these sustainability reports, they are comprehensive documents, often extending to 100 pages, that ESG professionals spend hours reading through. They provide valuable insights into a company's environmental targets, performance and initiatives, alongside information on employee welfare such as gender pay equality, workplace diversity, staff retention, and charitable contributions. What Information is required in the mandatory sustainability reports?First year requirements include:

Sustainability reports must be included within a company's annual report or linked to a separate sustainability report embedded within the annual report. Second year expansion: From discussions we have had with companies, it is evident that data is still difficult to obtain, with some sectors having no set methodology for reporting of emissions. For example, Rabobank shared how they issue carbon calculators to farmers in their loan book, whereas Nestle are often using Sustainability NGOs to build out their primary data from within their supply chain. Our sense is that it is difficult to have good visibility and confidence in obtaining correct data, but we believe this will evolve. First three years: From 2028, directors will assume full liability for these disclosures. What is climate data useful for and how will practitioners use these reports?As a fixed income investor, data and disclosures in these reports often help steer our questions to an issuer during company engagement. The information helps us home in on the areas where the company might be underperforming against their peers, or is not on track to meet their targets. There are some industries where it is obvious as to what climate risks are - for example, those with high carbon footprints and in 'hard to abate' sectors such as energy, mining and airline companies. For other companies, it's essential to delve deeper into the sources of their emissions, particularly the components of their scope 3 emissions, and assess the measures they are taking to reduce them. We are interested to know whether the company has a credible pathway for decarbonisation, have they set targets, are they on track to meet them, how are they reporting and how are they engaging with their supply chain, amongst other things. Our ESG due diligence starts through analysing the data, reading the company's own sustainability reports and examining third party research reports. This will form the basis of our questions during company engagements and help us assess the ESG risks of a company and the mitigation strategies in play. It all forms part of our ESG integration in the investment portfolios we manage. How do we capture ESG metrics for issuers in our portfolio?

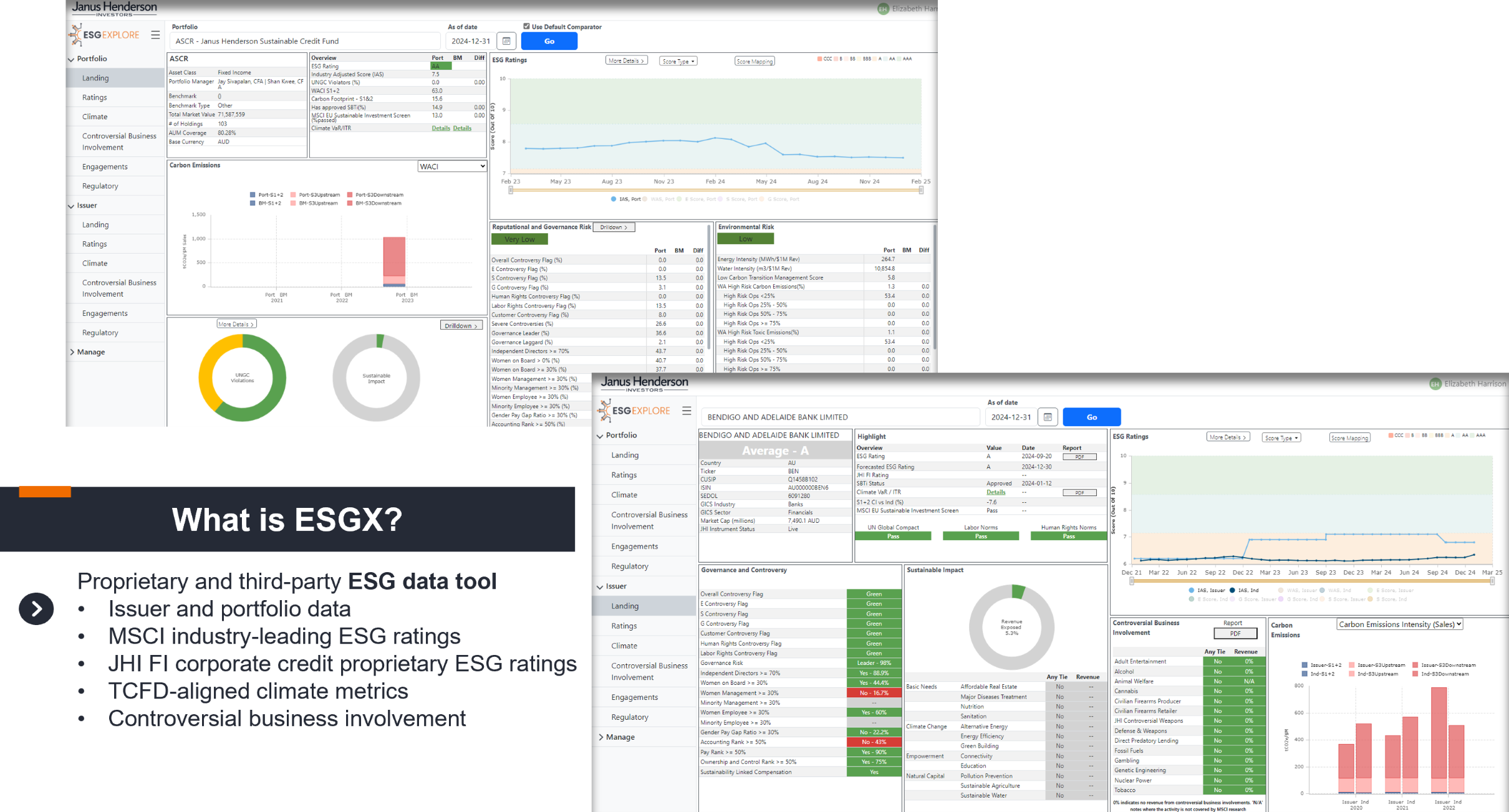

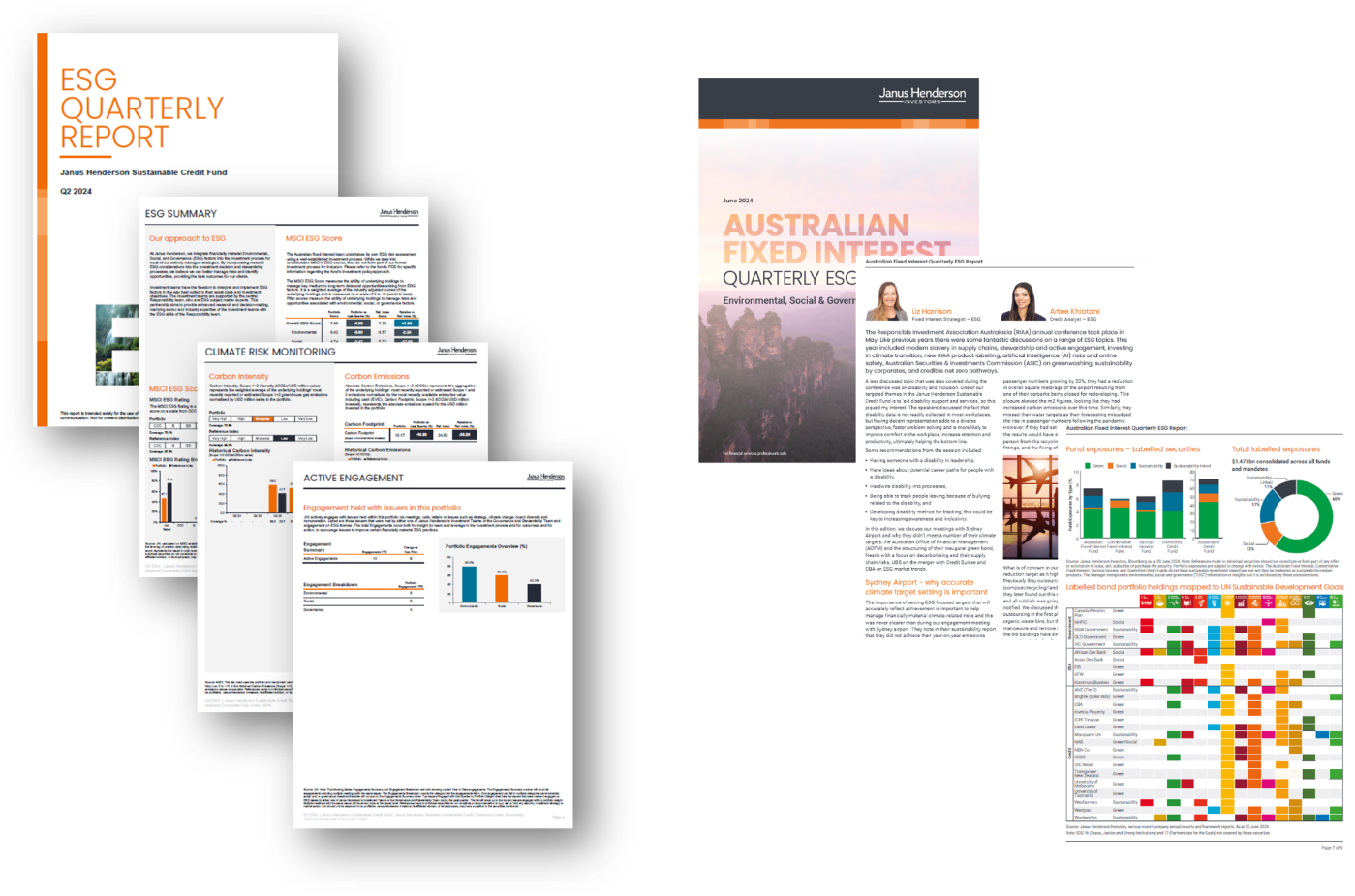

At Janus Henderson, we use MSCI as our preferred data provider. For ease of usage, we have created a proprietary data capture platform called ESG Explore which imports MSCI data. It allows the user to easily search for an issuer and obtain climate data and other ESG metrics such as controversial business involvement, controversies, MSCI risk ratings etc. Further, this same information can be calculated on a portfolio level with the total carbon emissions, weighted average carbon intensity, implied temperature rises of the asset pool and any product involvement all disclosed (where data is available). What reporting do we have available to assist asset owners?

The ESG data of our investment portfolios is then used to create our ESG reporting for the portfolios in which our clients' invest. For asset owners that need to undertake the mandatory sustainability reporting, they will need to report on scope 3 emissions from year 2. Their scope 3 emissions will comprise the scope 1 & 2 emissions of issuers within their investment portfolio. Our ESG reporting details the portfolio's carbon footprint (scope 1+2 tCO2e/USDmn invested), carbon emissions (scope 1+2 tCO2e) and weighted average carbon intensity (scope 1+2 tCO2e/USDmn sales), all reported quarterly. However, as it stands there are limitations with the availability of ESG data, with some issuers still not publishing their emissions or there is no coverage on that company by MSCI. This should improve as all companies are phased into the mandatory climate disclosure reporting. |

||||||||||||||||

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund 1Source: ACSI, Promises, Pathways & Performance, Climate change disclosure in the ASX200, July 2024 All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |