No events currently listed.

Find a Fund

Peer Group Analysis View All»

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

13.11% |

8.94% |

8.41% |

|

3.94% |

4.79% |

2.54% |

|

-17.81% |

19.33% |

6.15% |

|

7.15% |

7.37% |

2.40% |

|

10.94% |

7.63% |

6.05% |

|

22.58% |

12.46% |

9.16% |

|

6.18% |

10.38% |

6.62% |

|

18.67% |

12.22% |

4.89% |

|

5.61% |

6.85% |

6.32% |

|

12.88% |

13.46% |

8.29% |

|

8.85% |

8.32% |

4.17% |

|

21.32% |

15.17% |

7.09% |

|

13.68% |

10.37% |

10.19% |

|

10.93% |

8.05% |

5.65% |

|

7.03% |

8.32% |

7.11% |

|

-0.18% |

-0.64% |

1.23% |

|

8.56% |

8.92% |

7.82% |

Hedge Clippings

29 Nov 2024 - Hedge Clippings | 29 November 2024

|

|

|

|

Hedge Clippings | 29 November 2024 RBA Governor Michele Bullock recently spoke at the Committee for Economic Development of Australia (CEDA) Annual Dinner, and her message was clear that the RBA isn't rushing to cut interest rates like some of its international counterparts. That won't please the Treasurer Jim Chalmers, who likes to quote the fact that annual inflation has now fallen from 3.8% in June, to the October rate released this week of 2.1%, the lowest rate since July 2021. Dr. Chalmers is facing an election in the first few months of the new year, and he would dearly love the RBA to start cutting rates to help his cause. The RBA's issue is that much of the reduction since June has been thanks to the Treasurer's generosity in reducing electricity and power prices via government handouts - also we suspect with an eye on the upcoming election. Electricity prices have fallen 35.6% in the past 12 months, the largest fall ever recorded. Unfortunately (for Dr. Jim) the RBA looks beyond the headline rate, preferring the "Trimmed Mean" which cuts out extremes like electricity and fuel (-11.5%), and which sits uncomfortably at 3.4%, up from 3.2% in September, due in part to rises in food and non-alcoholic beverages (+3.3%), recreation and culture ( +4.3%) and alcohol and tobacco (+6.0%). At the CEDA event, Bullock stressed the bank's focus on sustainable falls to inflation, and that the Board can clearly see through the current drop in electricity prices as being temporary. In fact, in her speech she mentioned sustainably or sustainable no less than 13 times, just in case the Treasurer didn't get the point (which we're sure he did, he probably just didn't like it). So while she conceded that other central banks are starting to ease rates as inflation drops, Bullock was clear that Australia isn't there yet. Core inflation is still too high to consider rate cuts in the near term and according to Bullock, forecasts show a sustainable (there's that word again) return of underlying inflation to target won't occur until 2026. Meanwhile, PinPoint Macro Analytics has shared their insights on the broader economic landscape, particularly around the uncertainty following President Trump's return to the White House. In their piece, "Trump & Uncertainty," (see below for a link to the full article) they pointed out how unpredictable things are right now, from trade policies to fiscal and monetary directions. Markets are holding their breath, waiting to see what happens with potential tariffs, tax cuts, and any shifts in Federal Reserve policy. While some areas like infrastructure and defence spending seem relatively stable, the takeaway from PinPoint is that investors need to stay nimble given the ongoing geopolitical and fiscal unpredictability. All these recent developments reflect a bigger theme: Uncertainty is the name of the game, both at home and globally. The RBA's cautious stance makes a lot of sense in this context—it's about maintaining stability in an unpredictable world, especially with international pressures adding more layers of complexity. Whether it's changing U.S. policies or shifting global trade dynamics, everyone—from investors to businesses to policymakers—is having to adapt on the fly. Bullock's emphasis on a steady hand is a reminder that sometimes, the smartest move is knowing when not to make a move. Chalmers and Albo have no such leeway. May is not far away. News & Insights How Co-Investments are Transforming Affordable Housing | Webinar | HOPE Housing Fund Management Global Matters: The data centre opportunity for infrastructure investors | 4D Infrastructure 10k Words | Equitable Investors Market Commentary - October | Glenmore Asset Management October 2024 Performance News Bennelong Twenty20 Australian Equities Fund Insync Global Quality Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

12 Dec 2024 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

12 Dec 2024 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

12 Dec 2024 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

12 Dec 2024 - AI - Is the juice worth the squeeze?

|

AI - Is the juice worth the squeeze? Janus Henderson Investors November 2024 Power availability is the biggest challenge for AI growth. Portfolio Manager Hamish Chamberlayne discusses how innovation seeks to meet AI's energy needs but highlights unresolved issues regarding its energy sources and the technology's potential impact on climate.

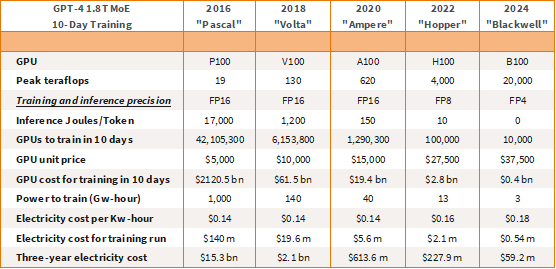

The power demands of artificial intelligence (AI), combined with the impacts of reindustrialisation, (EVs), and the transition to renewable energy, sees the technology represent a significant investment opportunity across the entire value chain, including data centre and grid infrastructure, as well as electrification end markets. However, it is important to always consider and question potential risks, particularly the physical limitations on AI's growth, where its insatiable thirst for energy will come from, and how its associated emissions may fuel new climate concerns. What is enabling AI?The advancement of AI is primarily enabled by US-based chipmaker Nvidia's increasingly efficient graphic processing units (GPUs). Figure 1 illustrates the evolution of its GPUs, showcasing the efficiency gains, depicted in terms of teraflops per GPU, per watt, across models from Pascal (2016) to its latest iteration Blackwell (2024). Currently, to train OpenAI's ChatGPT-4 in just ten days, one would need 10,000 Blackwell GPUs costing roughly US$400 million. In contrast, as little as six years ago, training such a large language model (LLM) would have required millions of the older type of GPUs to do the same job. In fact, it would have required over six million Volta GPUs at a cost of US$61.5 billion - making it prohibitively expensive. This differential underscores not only the substantial cost associated with Blackwell's predecessors but also the enormous energy requirements for training LLMs like ChatGPT-4. Figure 1: The cost curve

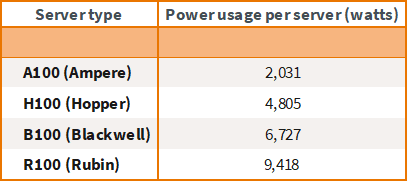

Source: NVIDIA, nextplatform, epochai.org Previously, the energy cost alone for training such an LLM could reach as much as US$140 million, rendering the process economically unviable. The significant leap in the computing efficiency of these chips, particularly in terms of power efficiency, however; has now made it economically feasible to train LLMs. This point is illustrated in Figure 1 under the metric 'inference joules/token', which is used to measure the energy efficiency of processing natural language tasks, particularly in the context of LLMs like those used for generating or understanding text (e.g., chatbots, translation systems). Here we can see a 25x improvement in efficiency from Nvidia's Hopper (10) to its Blackwell (0.4) successor. The sting in the tailNvidia's innovations in the power efficiency of its chips have indeed enabled advancements in AI. However, there is a significant caveat to consider. Although we often assess the cost-effectiveness of these chips in terms of computing power per unit of energy - Floating Point Operations Per Second (FLOPS) per watt - it's important to note that the newer chips come with a higher power rating (Figure 2). This means that, in absolute terms, these new chips consume more power than their predecessors. Figure 2: Nvidia GPU power ratings

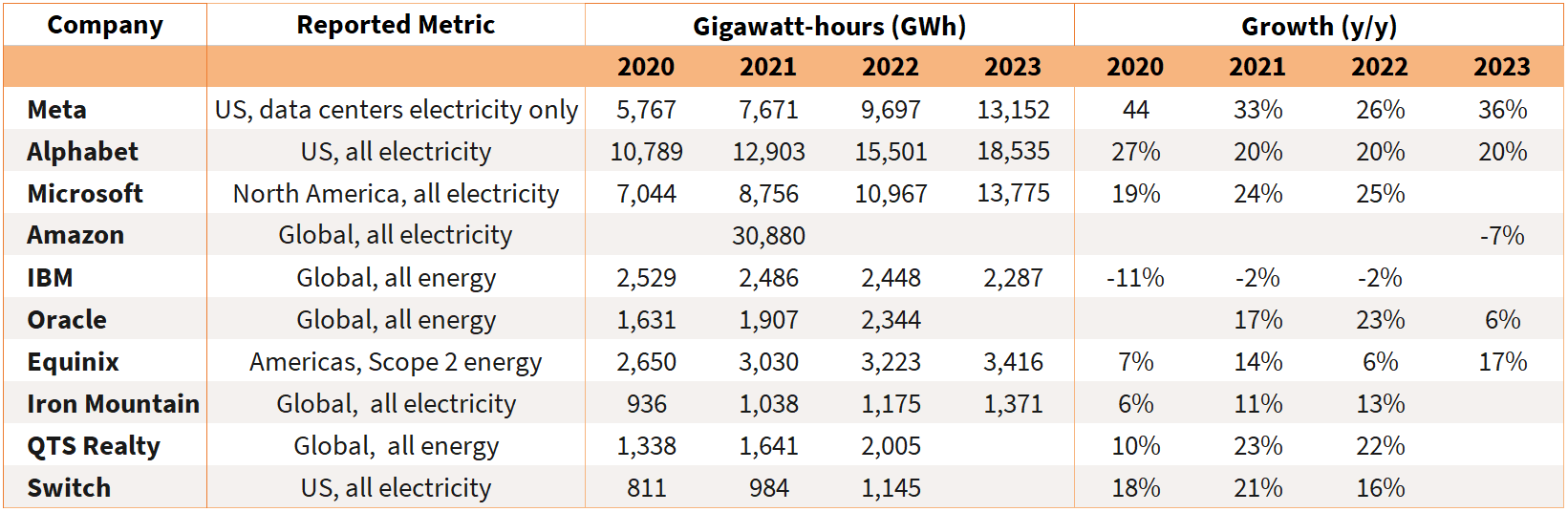

Source: Morgan Stanley research Note: Power usage per server (assuming four chips per server). Couple this with Nvidia's strong sales growth, indicating an incredible demand for computing power from companies like Alphabet (Google), OpenAI, Microsoft and Meta, driven by the ever-increasing size of datasets to develop AI technologies, the power implications of AI's rapid expansion have begun to raise eyebrows. Interestingly, thanks to efficiency improvements, global data centre power consumption has remained relatively constant over the past decade, despite a massive twelvefold increase in internet traffic and an eightfold rise in datacentre workloads.1 An International Energy Agency (IEA) report highlighted how data centres consumed an estimated 460 terawatt-hours (TWh) in 2022, representing roughly 2% of global energy demand,2 which was largely the same level as it was in 2010. But, with the advent of AI and its thirst for energy, data centre energy consumption is set to surge. In fact, the IEA estimates that data centres' total electricity consumption could more than double to reach over 1,000 TWh in 2026 - roughly equivalent to the electricity consumption of Japan.3 This highlights how demand for AI is creating a paradigm shift in power demand growth. Since the Global Financial Crisis (GFC), demand for electricity in the US has witnessed a flat 1% bump annually - until recently.4 Driven by AI, increasing manufacturing/industrial production and broader electrification trends, US electricity demand is expected to grow 2.4% annually.5 Further, based on analysis of available disclosures from technology companies, public data centre providers and utilities, and data from the Environmental Investigation Agency, Barclays Research estimates that data centres account for 3.5% of US electricity consumption today, and data centre electricity use could be above 5.5% in 2027 and more than 9% by 2030.6 The innovation, efficiency, and sustainability paradoxThis paradigm shift introduces the concept of the Jevons Paradox, which has implications for energy consumption and environmental sustainability. It suggests that simply improving the efficiency of resource use is not enough to reduce total resource consumption. The paradox is named after William Stanley Jevons, an English economist who first noted this phenomenon in the 19th century during the Industrial Revolution. In his 1865 book "The Coal Question," Jevons observed that technological improvements in steam engines made them more efficient in using coal. However, instead of leading to a reduction in the amount of coal used, these efficiencies led to a broader range of applications for steam power. As a result, the overall consumption of coal increased dramatically. This paradox appears to be equally applicable today as we stand at the threshold of a new AI powered industrial revolution. As innovation by chipmakers drives a rapid rise in the computational power and efficiency of chips, the potential productivity benefits of AI across various industries is resulting in even greater demand for the technology, which in turn is leading to an increase in energy consumption despite these efficiency improvements. To put this into context, in theory, transitioning from a Hopper to a Blackwell-powered data centre should result in a fourfold reduction in power consumption. However, as depicted by the data in Figure 3, the opposite is true, because large AI companies and hyperscalers are instead maximising the use of these more powerful, efficient chips. This has resulted in the number of GPUs within a data centre increasing, underscoring the essence of the Jevons Paradox whereby increased efficiency leads to greater overall consumption due to expanded use. Figure 3: Data centre provider energy and electricity use

Source: Company reports and Barclays Research Critical questionsA historical barrier to AI development has been energy costs. Considering prevailing trends and their power implications, a crucial question arises: Where is this additional power going to come from and what are the implications for emissions? In exploring this issue, three key areas emerge as focal points:

The power demands of AI, combined with the impacts of reindustrialisation, EVs, and the shift to renewable energy, is creating strong market conditions for companies exposed to electrification. This is exemplified by power companies Vistra and Constellation Energy, which were among the best-performing US stocks year-to-date, rising more than 282% and 105% respectively at the time of publication.7

The potential physical constraints to AI's growth must also be examined. This encompasses not only the limitations of current technology and infrastructure but also the availability of resources needed to sustain the rapidly rising power demands of the technology.

To address these issues big hyperscalers have restated their commitments to decarbonisation pathways and some have turned towards nuclear energy as a solution, but this brings its own environmental considerations. We must consider the emissions profile of AI and the broader environmental impact of increased power consumption. This includes not just the immediate emissions from power generation but also its long-term sustainability. The emissions profiles of big tech companies have barely declined over the last several years, with the rise of AI creating even larger energy demands. According to research by AI startup Hugging Face and Carnegie Mellon University, using generative AI to create a single image takes as much energy as full charging a smartphone.8 Nuclear energy to fuel AI power demandTo illustrate the real-world implications of AI's increasing power demands, Microsoft recently announced a deal with Constellation Energy concerning the recommissioning of an 835 megawatt (MW) nuclear reactor at the Three Mile Island site in Pennyslyvania.9 This deal highlights the sheer scale of efforts being made to meet the growing power needs of AI. The move is part of Microsoft's broader commitment to its decarbonisation path, demonstrating how corporate power demands are intersecting with sustainable energy solutions. The cost of recommissioning the nuclear reactor is estimated at US$1.6 billion, with a projected timeline of three years for the reactor to become operational, with Microsoft targeting a 2028 completion date. In October, Alphabet finalised an order for seven small modular reactors (SMRs) from California-based Kairos Power to provide a low-carbon solution to power its data centres amid rising demand growth for AI and cloud storage. The first of these SMRs is due to be completed by 2030 with the remainder scheduled to go live by 2035.10 Amazon also announced that it has signed three new agreements to support the development of nuclear energy projects - including the construction of several new SMRs to address growing energy demands.11 These initiatives underscore the significant investments and timeframes involved in securing the additional power capacities required to support the escalating energy demands of modern computing and AI technologies. Further initiatives are expected given the incremental demand for data centre capacity in the US market is projected to grow by 10% per year for the next five years.12 This growth could result in data centres potentially representing up to 10% of the total US energy supply by 2030, which is significant given that Rystad Energy forecasts that total US power demand will grow by 175 TWh between 2023 and 2030, bringing the country's demand close to 4,500 TWh.13 While Microsoft is committing to nuclear power, a carbon-free source of electricity as part of its decarbonisation efforts, we remain cautious and concerned about how the energy gap required to support this growth in AI and data centres will be filled. Powering the futureEarlier this year, we engaged with Microsoft on its increase in emissions and commitment to renewable energy sourcing for data centres. In August, we were pleased to see Microsoft address concerns regarding the increasing energy requirements of AI and the resulting shift towards sustainable practices across the industry during its presentation to the Australian Senate Select Committee on Adopting AI.14 The hyperscaler acknowledged that AI models and related services require a lot more power than traditional cloud services and was a key issue the industry needed to address. Microsoft also stated that it remained on course to achieve its 2030 net zero and water-positive targets in its sustainability strategy. While the increased power demands were unknown in 2020 when the targets were set, the use of renewable and nuclear energy should enable the commitment to be sustainably met. Microsoft Founder Bill Gates has urged global policymakers to refrain from going "overboard" with regards their concerns about AI's energy footprint, noting that the technology will likely play a decisive role in achieving net zero ambitions by reducing global demand. AI and the energy transitionAdvancements in AI, when paired with innovations in renewables, may hold the key to sustainably meeting rising energy demand. The IEA reported that power sector investment in solar photovoltaic (PV) technology is projected to exceed US$500 billion in 2024, surpassing all other generation sources combined.15 By integrating AI into various solar energy applications, such as using technology to analyse meteorological data to produce more accurate weather forecasts, intermittent energy supply can be mitigated.16 Researchers are also relying on AI to accelerate innovation in energy storage systems, given existing conventional lithium batteries are unable to fulfil efficiency and capacity requirements.17 While AI will create additional demand for energy, it also has the potential to solve challenges related to the net zero transition. In April, the US Department of Energy (DoE) released a report outlining how AI will likely play a vital role in accelerating the development of a 100% clean electricity system.18 Significant opportunities in the following areas were outlined:

Beyond the grid, AI has the potential to play a significant role in supporting a variety of applications that can contribute to the development of a fair, clean energy economy, the DoE noted. Achieving a net zero greenhouse gas (GHG) emissions target throughout the economy involves overcoming distinct challenges in various sectors, such as transportation, buildings, industry, and agriculture. We are witnessing signs of growing demand for AI across various sectors including healthcare, transportation, finance, and industry, and we anticipate this to be a sustained, long-term trend. As a team we have benefited from involvement in AI and the wider movements towards electrification and re-industrialisation. However, we are conscious of the potential increase in carbon emissions due to AI's expansion and are closely monitoring the decarbonisation pledges of companies like Nvidia and Microsoft. While we anticipate a short-term rise in emissions, we are optimistic that AI will ultimately contribute positively to decarbonisation efforts through innovation and productivity enhancements and are confident that the heightened demand for power will be addressed by increased investment in clean energy. Despite this being a year marked by significant political changes worldwide, our outlook for investing in sustainable equities remains positive. Inflationary pressures are easing, and monetary policy appears to be taking a more supportive direction. Regardless of the political landscape, the fundamental trends we are focused on are continuing to advance and develop. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund, Janus Henderson Australian Fixed Interest Fund - Institutional, Janus Henderson Cash Fund - Institutional, Janus Henderson Conservative Fixed Interest Fund, Janus Henderson Conservative Fixed Interest Fund - Institutional, Janus Henderson Diversified Credit Fund, Janus Henderson Global Equity Income Fund, Janus Henderson Global Multi-Strategy Fund, Janus Henderson Global Natural Resources Fund, Janus Henderson Tactical Income Fund

IMPORTANT INFORMATION References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns. Sustainable or Environmental, Social and Governance (ESG) investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than the broader market. Footnotes and definitions 1International Energy Agency, 'Global trends in internet traffic, data centre workloads and data centre energy use, 2010-2019 (last updated 3 June 2020) 2International Energy Agency, 'Electricity 2024: Analysis and forecast to 2026' 3International Energy Agency, 'Electricity 2024: Analysis and forecast to 2026' 4University of Wisconsin-Madison, 'The Hidden Cost of AI' by Aaron R. Conklin (21 August 2024) 5Goldman Sachs, 'Generational growth: AI, data centres and the coming US power demand surge' (28 April 2024) 6Barclays Research, 'Artificial Intelligence is hungry for power' (28 August 2024) 7Google Finance, Market summary for Vistra, Constellation Energy (12 November 2024) 8MIT Technology Review, 'AI's carbon footprint is bigger than you think' (5 December 2023) 9Constellation Energy, press release (20 September 2024) 10Kairos Power, Press release (14 October 2024) 11Amazon, press release (16 October 2024) 12McKinsey, 'Investing in the rising data centre economy' (17 January 2023) 13Rystad Energy, 'Data centers and EV expansion create around 300 TWh increase in US electricity demand by 2030' (25 June 2024) 14ARNnet, 'Microsoft A/NZ acknowledges local energy usage increase due to AI' (August 2024) 15International Energy Agency, World Energy Investment 2024 Report 16World Economic Forum, 'Sun, sensors and silicon: How AI is revolutionizing solar farms' (2 August 2024)15Source: ERGO Group, 'How AI is helping with battery development' (20 August 2024) 17Dean H. Barrett and Aderemi Haruna, Molecular Sciences Institute, School of Chemistry, University of the Witwatersrand, 'Artificial intelligence and machine learning for targeted energy storage solutions' 18Source: US Department of Energy, AI for Energy: Opportunities for a Modern Grid and Clean Energy Economy (April 2024) FLOPS: Stands for Floating Point Operations Per Second (FLOPS), and it's a measure of a computer's performance, especially in fields that require a large number of floating-point calculations. Higher FLOPS indicate more calculations can be done per second, which is particularly relevant for training and running complex machine learning models. FLOPS/Watt is a measure of computational efficiency, indicating how many floating-point operations a system can perform per unit of power consumed. The higher the FLOPS/Watt, the more energy-efficient the system is. Inference: Within the context of this article, this refers to the process of using a trained model to make predictions or decisions based on new, unseen data. In the context of language models, inference would involve tasks like generating text responses, translating languages, or answering questions. Joule: A unit of energy in the International System of Units. It's a measure of the amount of work done, or energy transferred, when applying one newton of force over a displacement of one meter, or one second of passing an electric current of one ampere through a resistance of one ohm. Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. Monetary policy tools include setting interest rates and controlling the supply of money. Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money. See also fiscal policy. Net zero: A state in which greenhouse gases, such as Carbon Dioxide (C02) that contribute to global warming, going into the atmosphere are balanced by their removal out of the atmosphere. Per token: In natural language processing (NLP), a "token" typically refers to a piece of text, which could be a word, part of a word, or even a character, depending on the granularity of the model. Thus, "per token" means that the energy usage is being measured with respect to each individual piece of text processed by the model. Watt: A unit of power in the International System of Units, representing the rate of energy transfer of one joule per second. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

11 Dec 2024 - Performance Report: Seed Funds Management Hybrid Income Fund

[Current Manager Report if available]

11 Dec 2024 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

[Current Manager Report if available]

11 Dec 2024 -

|

"A is for Ambition": Apple and Amazon Bet Big on the Future Alphinity Investment Management December 2024 |

|

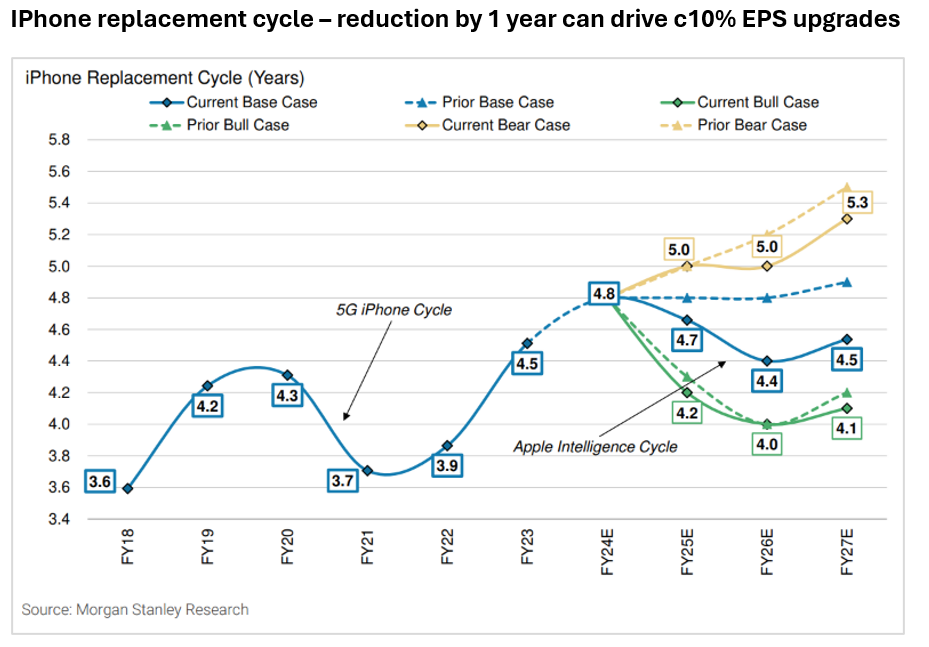

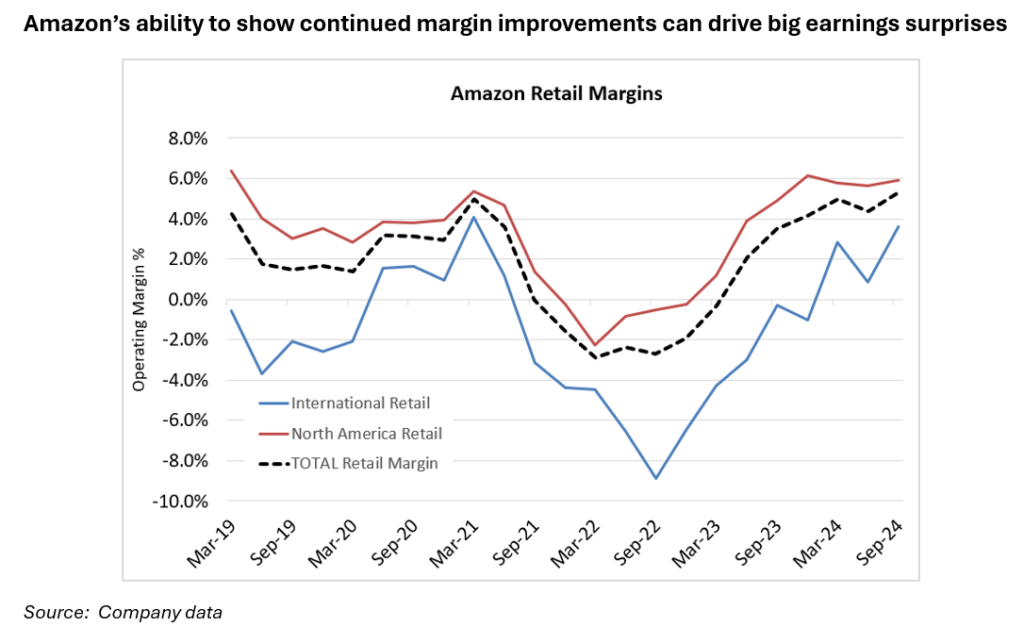

The recent Apple and Amazon third quarter 2024 results revealed further details around the critical leg of their strategies, with these tech giants continuing to lay down markers for how they see the next stage of tech evolution unfolding and staking out positions to profit from it. Looming large in this evolution is AI, with Apple looking to leverage capabilities across what is an enormous ecosystem of 2.2bn active devices while Amazon is focusing on pushing AI applications across their Cloud and consumer business. The recent results also provided key insights into shorter term business performance.  Key takeaway from the result? The key takeaway from the Apple result is that while the gains from the release of "Apple Intelligence" will be significant, they will take time. This was evidenced by the fact that despite this recent result coming in ahead of expectations, it was coupled with a guide for the coming quarter that was mildly below what the market was looking for (Apple guided to revenue growth of low to mid-single digits vs a market that was expecting +7%). This makes sense as "Apple Intelligence" has only just rolled out in the US in recent weeks, and will not become available in the UK, Australia, Canada, and New Zealand until December 2024. Other geographies will follow over the course of 2025. Most importantly, it is also December 2024 before we see a meaningful expansion of the AI features including the long-awaited Chat GPT integration. As such, the powerful iPhone upgrade cycle that we expect to come with "Apple Intelligence" is likely to be a slow burn, with momentum building through 2025 and into 2026. What impressed? The ability of Apple to turn a benign demand environment into double digit EPS growth is impressive. Products growth has been tepid but the higher growth Services business, margin expansion and a buy-back continues to drive EPS growth above 10%. What disappointed? While we appreciate that Apple Intelligence will take time, the pace of the roll-out driving the weaker than expected outlook for 4Q (which is their biggest quarter of the year) was mildly disappointing. However, Apple tend to focus on quality rather than speed, so we do think that their ability to monetise AI across an installed base of 2.2bn active devices is a compelling, multi-year opportunity. Interesting chart? The next phase for Apple is all about an iPhone replacement cycle coupled with an expansion of associated Services revenue. The chart below shows what happened the last time a compelling technology shift occurred, with 5G driving a compression in this replacement cycle. Since the most recent trough in FY21, replacement cycles have shifted out by more than 12 months. A compression of this replacement cycle back towards 4yrs will drive circa 10% EPS upgrades.  What are the key risks? There are a few key risks facing Apple in the coming years. Key among these are:

In summary, Apple's ability to monetise their enormous consumer ecosystem is almost unrivalled. They will find a structure through which to monetise Ai, both through device sales but more importantly through an expansion of Ai related Services offerings. There is no company better placed to be the window into Ai for the average consumer.  Key takeaway from the result? Margins, margins, margins. Given the scale of the Amazon business, a mild shift in margin outcomes can drive enormous gains in operating income and EPS. Amazon spooked the market during their 2Q24 results which showed margins for their core retail business to be weaker than expected, which was blamed on everything from mix (lower priced "everyday essentials" in baskets) to building extra satellites for their broadband business. However, come the 3Q24 result last week, all was forgotten as Amazon blew those margin expectations (that they ironically had guided to themselves) out of the water. So, the question becomes, will this margin expansion continue? What impressed? The margin outcome in the core retail business was impressive, particularly in the international segment. Despite pressures from mix and what appears to be heightened competition from legacy retailers (eg Walmart) and Chinese players (Temu, Shein), Amazon generated solid topline growth and exceptional margins. The Amazon cloud business AWS also showed a continuing reacceleration driven in part by AI. A combination of the "law of large numbers" plus optimisations had driven compression in cloud growth rates across Amazon (AWS), Microsoft (Azure) and Google (GCP). However, the advent of AI has driven a reacceleration in cloud growth, which is impressive given the base of business is significantly larger. What disappointed? While it may seem unusual to have any source of disappointment in an exceptionally strong result, the variability of the margin outcomes compared to what management expected could indicate a lack of visibility. While a "miss vs expectations" is very happily received when it is an upside surprise, it does raise some concerns that perhaps next time the "surprise" could be the other way. Interesting chart? Given the scale of the retail business, a shift in margin expectations has a material impact on earnings. A circa 100bps improvement in Retail margins vs current expectations for CY25 would drive a 7% beat in Amazon operating income.  What are the key risks? For Amazon, risks are on a couple of key fronts:

In summary, Amazon's 3Q24 earnings report highlighted the significant earnings potential of the business and underscored the company's strong market position and attractive consumer offerings. However, it is crucial to closely monitor Amazon's ability to sustain margin improvements and effectively navigate ongoing consumer pressures in the future. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund |

10 Dec 2024 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

10 Dec 2024 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

10 Dec 2024 - Mixed market sentiment for 2025 driven by global geopolitics and central bank easing cycles

|

Mixed market sentiment for 2025 driven by global geopolitics and central bank easing cycles Bennelong Funds Management November 2024 The incoming Trump administration has raised uncertainty about the outlook for global markets in 2025, particularly around the implementation of Trump's protectionist policies, according to Bennelong and its boutique partners Canopy Investors, 4D Infrastructure and Quay Global Investors.

The new US administration's activities and policy changes will be very important in driving market sentiment in 2025, and will create both opportunities and risks, according to Canopy Investors' portfolio manager, Kris Webster. "There remains significant uncertainty about the actual policies that will be introduced, and their ultimate impact, making the outlook for 2025 very uncertain. "However, based on Trump's stated policy positions, several domestic US sectors appear well positioned to benefit from his presidency. These include manufacturers, energy companies, and industries targeted for deregulation, for example financials. "Conversely, certain sectors may face headwinds including global exporters to the US, US importers, and companies with substantial China exposure. "Markets have already priced in some of these policy expectations, as evidenced by US dollar strength against major currencies. This dynamic has created increasingly attractive valuations for many high-quality stocks in markets outside the US, particularly those with limited exposure to US policy changes. Mr Webster says a critical uncertainty centres on how these policies might affect inflation and, by extension, interest rates - both of which significantly influence asset prices and highly leveraged companies. "It's possible the US government will moderate its policies around taxation, tariffs, and immigration, if inflation picks up again. "While we don't make short-term macro or market predictions, it is likely that the policy uncertainty anticipated in 2025 will drive increased market volatility. This environment should create opportunities for active investing, particularly in global small and mid-cap companies, where market inefficiencies tend to be more pronounced," he says. For global listed infrastructure, there is likely to be heightened policy noise in the US on what policies are prioritised for actual implementation, according to 4D Infrastructure CIO, Sarah Shaw. "Most notably, these include the 60 per cent tariff on Chinese goods and a universal 10 to 20 per cent tariff on all other countries. These could have an impact on infrastructure assets, in particular port and rail volumes in both export and import countries, with some volumes pulled forward ahead of the anticipated tariff increases, whilst some export markets will be substituted with other destination markets away from the US. "Trump is also looking to repeal some aspects of the Inflation Reduction Act (IRA), which may impact the growth outlook of some heavily US renewable focused developers and utilities. This could lead to an ongoing overhang till we see what is exactly implemented. "This pivot away from renewables and preferring traditional fossil fuels may be positive for north American pipelines if more federal lands are permitted for exploration. An undoing of Biden's pause of new LNG Export terminals will also help the long-term capital plans of those businesses," she says. "Lastly, the proposed policies are inflationary and a reversal in trend of interest rates could be a headwind for US nominal rate utilities which have had an incredibly strong year in 2024" Elsewhere in the world, Ms Shaw says there are divergent economic outlooks. "In Europe demand remains soft with interest rate trajectory down. China continues to struggle with a dormant economic outlook, increasing stimulus. In Brazil, growth continues to surprise to the upside with a reversal in the interest rate trajectory." Ms Shaw says that this macro uncertainty and geopolitical tensions will create volatility and noise, however by separating the attractive fundamentals of infrastructure from this noise and continuing to invest against the inefficiency of markets, investors can capture future earnings and growth in this asset class. "Infrastructure offers a unique combination of defensive characteristics and earnings resilience but with significant long-term growth thematics as well as an ability to capture economic cycles. "The need for global infrastructure investment over the coming decades is clear with five globally relevant and necessary thematics under pinning a multi decade growth story. With governments unable to wholly fund the infrastructure need, there's a significant opportunity for private investors to tap into this growth story. We can think of no more compelling or enduring global investment thematic for the coming 50 years," says Ms Shaw. Chris Bedingfield, portfolio manager at Quay Global Investors, sees a similar mixed story for global real estate assets. "Investors continue to make the mistake of thinking real estate is interest rate driven but the value in real estate can be found by focusing on thematics not influenced by macros factors or politics. "The aging population is a thematic we are focused on and 2025 marks the 80-year anniversary of the end of the second world war, meaning that next year, the first of the Baby Boomers will turn 80, an age where many turn to some type of assisted living. "Retail also continues to look very attractive. The recovery of in-store retail sales since COVID remains well above the prior pandemic trend. We expect good financial results from the best malls in 2025 as landlords continue to mark rents back to economic reality." Mr Bedingfield says there are signs that suggest a positive outlook for global REITs. "Timing the markets is hard. Miss a few good days and long-term total returns can alter significantly. This is especially so for listed real estate. "History suggests listed REITs run in anticipation of US Fed rate cuts and continue to perform for some time after, and we've seen this materialise after the first rate cut in September. "Moreover, higher building costs is already resulting in a shortage of global real estate, as the development equation does not work. This will simply squeeze future tenants, all the more to the benefit of landlords and investors of REITs," he says. The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.