No events currently listed.

June 2026

RBA - Monetary Policy Decision

Find a Fund

Peer Group Analysis »

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

13.11% |

8.94% |

8.41% |

|

3.94% |

4.79% |

2.54% |

|

-17.81% |

19.33% |

6.15% |

|

7.15% |

7.37% |

2.40% |

|

10.94% |

7.63% |

6.05% |

|

22.58% |

12.46% |

9.16% |

|

6.18% |

10.38% |

6.62% |

|

18.67% |

12.22% |

4.89% |

|

5.61% |

6.85% |

6.32% |

|

12.88% |

13.46% |

8.29% |

|

8.85% |

8.32% |

4.17% |

|

21.32% |

15.17% |

7.09% |

|

13.68% |

10.37% |

10.19% |

|

10.93% |

8.05% |

5.65% |

|

7.03% |

8.32% |

7.11% |

|

-0.18% |

-0.64% |

1.23% |

|

8.56% |

8.92% |

7.82% |

Hedge Clippings

Hedge Clippings | 06 December 2024

As we approach the end of the year it's normal to reach for the crystal ball and peer into the future. This is particularly the case as there's so much at stake, and so much that might - or in the case of the RBA's stance on interest rates...

Read more...

17 Dec 2024

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by +3.41% in November, an outperformance of +2.09% compared with the ASX Small Ordinaries Total Return benchmark which rose by +1.32%. Top contributors...

17 Dec 2024

Performance Report: Glenmore Australian Equities...

The Glenmore Australian Equities Fund rose by +5.14% in November, outperforming the ASX 200 Total Return benchmark by +1.35%. Since inception in June 2017, the fund has...

17 Dec 2024

Proprietary Data - Strategic AI Advantage

Proprietary data sets provide businesses with competitive advantages due to their uniqueness, quality and relevance. They are often more specific, accurate, and tailored to a...

16 Dec 2024

Performance Report: Bennelong Emerging Companies...

The Bennelong Emerging Companies Fund rose by +6.43% in November, outperforming the ASX 200 Total Return benchmark by +2.64%. Since inception in November 2017, the fund has...

16 Dec 2024

Investment Perspectives: Why a Trump presidency...

Last month, US voters re-elected Donald Trump for a second term as US president. As a result, market enthusiasm and expectations are high. An immediate rally in US equities...

13 Dec 2024

Performance Report: 4D Global Infrastructure Fund...

The 4D Global Infrastructure Fund (Unhedged) rose by +8.1% over the past 12 months. Since inception in March 2016, the fund has returned +9.03% per annum, a difference of...

13 Dec 2024

Performance Report: Argonaut Natural Resources...

The Argonaut Natural Resources Fund returned -2.7% in November, outperforming the S&P/ASX 300 Resources TR benchmark by +0.71%. Since inception in January 2020, the fund has...

13 Dec 2024

Performance Report: Bennelong Twenty20 Australian...

The Bennelong Twenty20 Australian Equities Fund rose by +4.49% in November, outperforming the ASX 200 Total Return benchmark by +0.7%. Since inception in November 2009, the...

13 Dec 2024

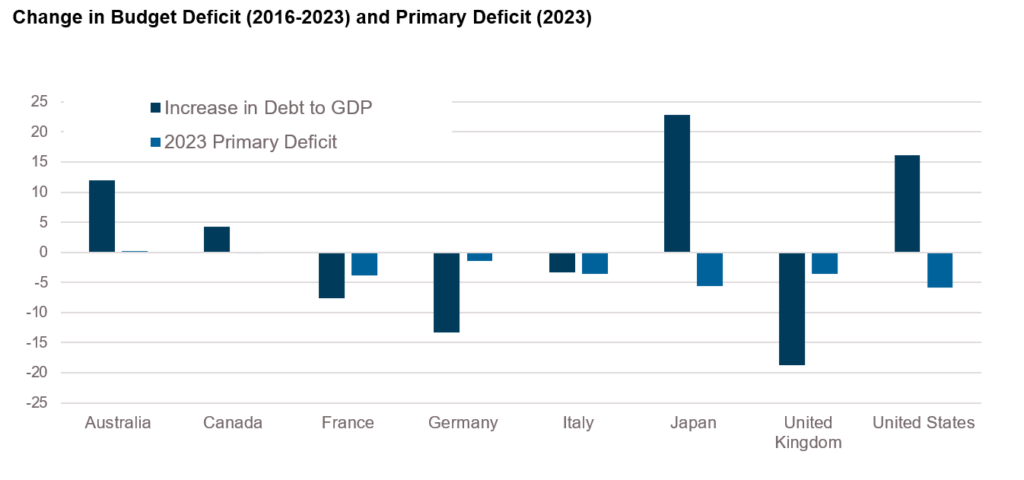

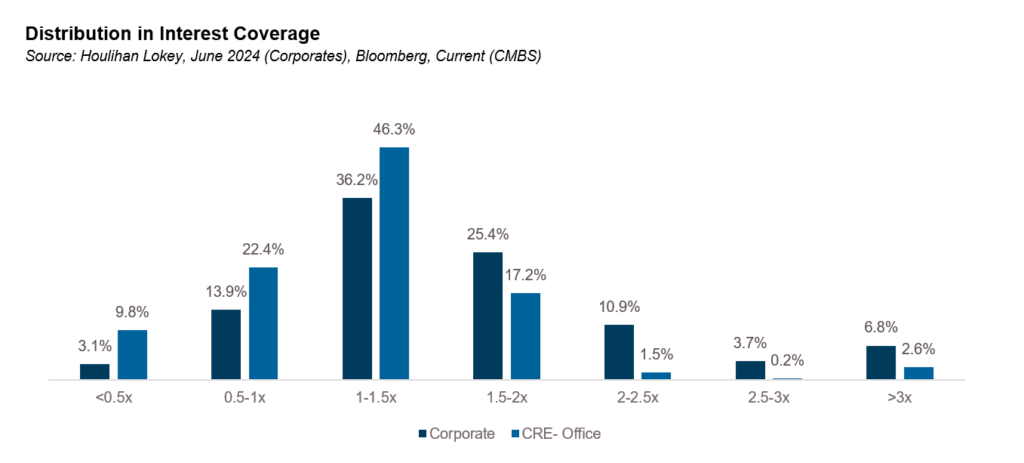

Risks & Issues in 2025 - Part 2

Part 2 of Risks & Issues in 2025 considers the implications of the global backdrop discussed in Part 1 for Australia - as well as some home-grown influences.

13 Dec 2024

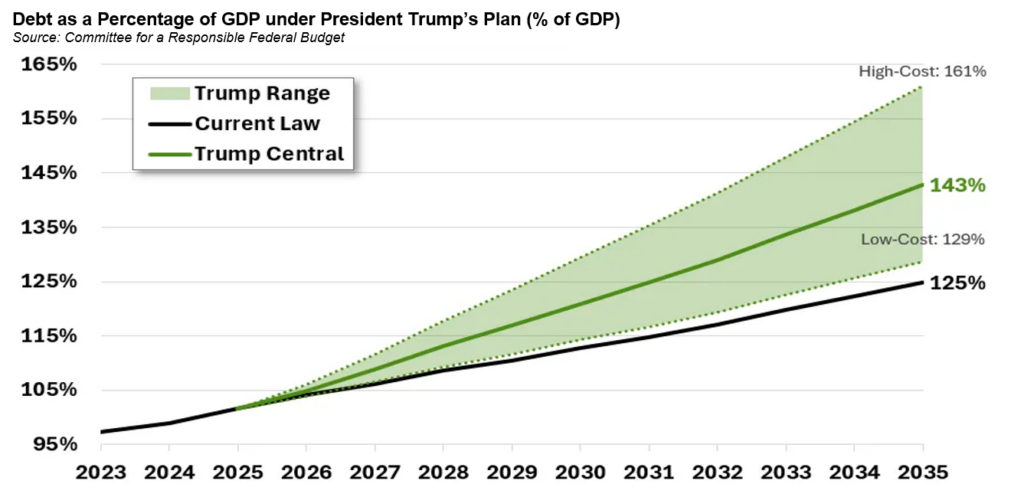

Trump trade 2.0 - Who is going to buy all this...

In 2016 the election of Donald Trump as president of the United States caused an initial panic in markets with S&P500 futures plunging over 5% as his shock win became more...

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.