No events currently listed.

Find a Fund

Peer Group Analysis View All»

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

13.11% |

8.94% |

8.41% |

|

3.94% |

4.79% |

2.54% |

|

-17.81% |

19.33% |

6.15% |

|

7.15% |

7.37% |

2.40% |

|

10.94% |

7.63% |

6.05% |

|

22.58% |

12.46% |

9.16% |

|

6.18% |

10.38% |

6.62% |

|

18.67% |

12.22% |

4.89% |

|

5.61% |

6.85% |

6.32% |

|

12.88% |

13.46% |

8.29% |

|

8.85% |

8.32% |

4.17% |

|

21.32% |

15.17% |

7.09% |

|

13.68% |

10.37% |

10.19% |

|

10.93% |

8.05% |

5.65% |

|

7.03% |

8.32% |

7.11% |

|

-0.18% |

-0.64% |

1.23% |

|

8.56% |

8.92% |

7.82% |

Hedge Clippings

4 Jun 2026 - Global smaller companies: When everyone owns the same names, what next?

|

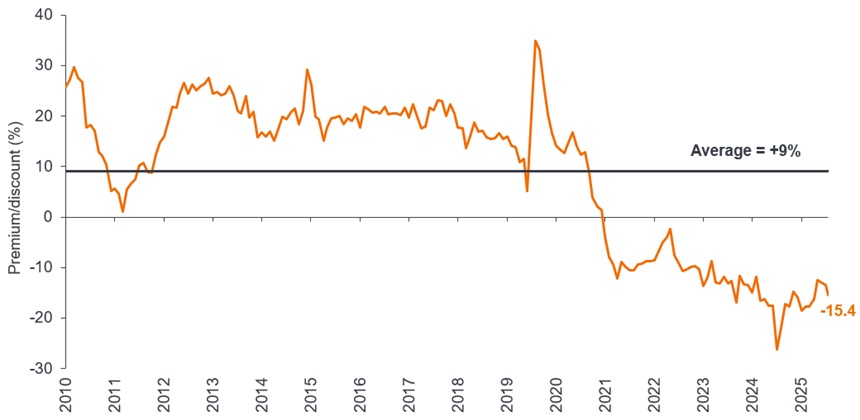

Global smaller companies: When everyone owns the same names, what next? Janus Henderson Investors May 2026 (8-minute read) Portfolio Manager Nick Sheridan explores why shifting market leadership, geopolitical uncertainty, and changing investor behaviour are bringing smaller companies back into focus, offering a broader set of opportunities beyond the most crowded trades. Markets started 2026 on an uncertain footing, pulled in different directions by geopolitical instability. The conflict in the Middle East, which began at the end of February, brought energy markets back into stark focus. Blocked supplies through the Strait of Hormuz pushed oil prices higher and raised fresh concerns about inflation just as central banks were attempting to stabilise growth. For investors, this has created a challenging mix of risks and uncertainties. Risk appetite has weakened as attention has become fixed on the conflict and its implications. Meanwhile, expectations for fiscal and monetary policies have shifted. Higher energy prices have complicated the outlook for interest rates. The uncertainty of government policy announcements via social has led to rapid swings in sentiment. The path to a lasting resolution remains obscured. Despite this backdrop, one notable feature of recent market behaviour has been the resilience of global smaller companies. This is typically the part of the market that struggles when uncertainty is elevated and policy is restrictive. In our view, this reflects modest starting valuations, positive earnings expectations, and a gradual shift in how investors are approaching markets. But even periods of tentative improvement in sentiment have seen investors look beyond the most heavily owned areas, suggesting that attention is no longer as narrowly focused as it once was. A turning point for market concentration Over the past decade, market returns have been dominated by a small group of large-cap technology companies (ie. the 'Magnificent 7' - Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia and Tesla). At the same time, higher interest rates, macro uncertainty, and a preference for liquidity has favoured larger, more resilient businesses. Combined with passive flows, this has created an increasingly concentrated market, turning investor allocations into a tacit call on technology stocks. What appears to be changing is not a sudden reversal but a gradual broadening of leadership. The focus is shifting from owning what has worked to reassessing where future returns may come from. It has been driven by a subtle change in behaviour, with investors showing greater sensitivity to valuation, a more questioning approach to crowded trades, and growing awareness of how concentrated portfolios have become, particularly at a time of heightened geopolitical uncertainty. The dominance of the largest companies has not disappeared, but it is no longer unquestioned. Artificial intelligence remains a powerful structural theme, yet investors are starting to look beyond the most obvious beneficiaries, to smaller companies exposed to adjacent areas of growth. At the same time, the earnings picture for smaller companies is improving. Combined with more modest starting valuations relative to global large caps (Exhibit 1), we believe it supports the conditions for a re-rating, even in an uneven market. Exhibit 1: Attractive valuations of global small caps relative to large caps

Source: Bloomberg, Janus Henderson Investors Analysis, as at 9 April 2026. Shows global small cap premium/discount versus global large caps (forward P/Es). Different regions, different strengths Much like their larger counterparts, global smaller companies provide exposure to a diverse set of local economies and sector opportunities. Unlike large multinationals, however, they tend to be more closely tied to domestic or regional growth, which can be an advantage in a more fragmented geopolitical environment. They also tend to be more entrepreneurial and agile, often driving advances within specialised niches, rather than at scale. Another defining feature is how little attention they receive. Smaller companies are typically under-owned and under-researched, with materially less coverage from stock analysts. A combination of less scrutiny and more varied outcomes creates opportunity for active investors taking a selective approach. Particularly so, given how strong earnings forecasts are for smaller companies relative to their large-cap peers[1]. But there are also important differences across regions, offering built-in diversification within the small-cap category. In the US, deep capital markets and a strong culture of innovation support a broad pipeline of companies across technology, healthcare, and specialised industrials. In Europe, the market is more weighted towards industrials, manufacturing, and niche export-led businesses. Many of these have strong technical expertise and pricing power, alongside tailwinds from defence and infrastructure spending. Japan offers another distinct profile, characterised by high-quality industrial and technology businesses. Improving corporate governance and a greater focus on shareholder returns are helping to unlock value in companies that have historically been overlooked. Market inefficiency equals opportunity for active investors Global smaller companies remain one of the few areas of genuine inefficiency in equity markets. Limited analyst coverage and the diversity of the opportunity set mean there is real scope to add value through detailed research and engagement. This increases the value of information in the small cap space, given that outcomes in smaller companies are driven more by stock-level factors than by broad market movements. Sector and stock dispersion is wide, meaning the gap between winners and losers can be significant. This makes a research-led, data-driven approach essential, with a focus on characteristics such as return on equity, balance sheet strength, and the sustainability of earnings. For investors willing to take a longer-term view, this part of the market offers exposure to businesses earlier in their growth journey. After all, many of today's dominant companies, such as Nvidia, began as small caps. This is not to overlook the risks; smaller companies can be more volatile and more sensitive to economic cycles. Navigating these risks requires a disciplined, structured approach to stock selection. Overall, we believe that global smaller companies continue to offer a compelling opportunity set. In a market long dominated by a narrow group of large-cap stocks, they provide diversification, exposure to innovation, and access to domestic growth trends across regions. The macro environment remains uncertain. However, for investors focused on fundamentals, the breadth of opportunities within global smaller companies remains significant. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. [1] Source: Bloomberg, Janus Henderson Investors, as at 9 April 2026. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns. Active investing: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis, and the investment choices they make. Asset allocation: The allocation of a portfolio between different asset classes, sectors, geographical regions, or types of security to meet specific objectives of risk, performance, or time horizon. Balance sheet: A financial statement that summarises a company's assets, liabilities, and shareholders' equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders. Diversification: A way of spreading risk by mixing different types of assets or asset classes in a portfolio on the assumption that these assets will behave differently in any given scenario. Assets with low correlation should provide the most diversification. Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures. Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving. Liquidity: A measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as 'liquid'. Premium: When the market price of a security is thought to be more than its underlying value, it is said to be 'trading at a premium'. Return on equity (ROE): A company's net income (income minus expenses and taxes) over a specified period, divided by the amount of money its shareholders have invested. It is used as a measurement of a company's profitability compared to its peers. A higher ROE generally indicates that a management team is more efficient at generating a return from investment. Returns/return: The total return of a portfolio over a specified period as opposed to its relative return against a benchmark. It is measured as a gain or a loss and stated as a percentage of a portfolio's total value. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

21 May 2026 - Global Perspectives: Addressing the most essential questions around AI

|

Global Perspectives: Addressing the most essential questions around AI Janus Henderson Investors May 2026 (Duration: 29 minutes) In this episode, Portfolio Manager Denny Fish takes a deep dive into the current state of artificial intelligence (AI), including the latest advancements, its potential to propel economic growth, and the rise of agentic AI and its impact on software business models. He also shares insights from a recent research trip in China. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

2 Apr 2026 - Unravelling the forces driving corporate credit's resilience

|

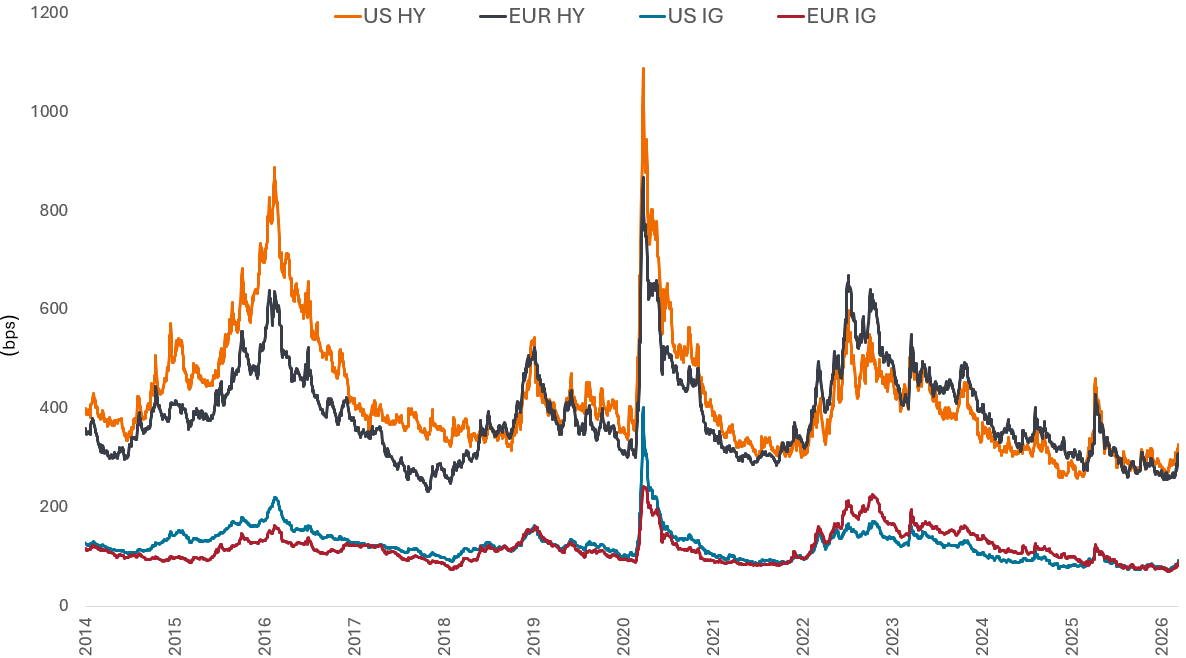

Unravelling the forces driving corporate credit's resilience Janus Henderson Investors March 2026 (8-minute read) Corporate credit has absorbed recent shocks with limited disruption. Head of High Yield Tom Ross and Corporate Credit Portfolio Manager James Briggs examine how fundamentals, market behaviour and dynamics as well as macro context are shaping credit resilience. Credit markets sanguine amid geopolitical riskThe conflict in the Middle East has drawn parallels with the outbreak of the Russia-Ukraine War, with concerns that an oil-induced supply and inflation shock could harm the global economy. So far, credit markets have reacted in a sanguine manner, with changes in credit spreads not dissimilar to the rates impact from rising government bond yields. As the chart below shows, the recent tick-up in credit spreads is muted when compared to last year's Liberation Day sell-off, let alone the 2015 energy sell-off after oil prices collapsed or the Covid spike. For now, the market assumption is that the conflict remains regional, although high oil and gas prices - caused by Iran's choke hold on ships transiting the Strait of Hormuz - could have a material impact on inflation and consumption were they to be sustained beyond the short term. For the time being, geopolitical shocks have not yet translated into a material deterioration in key economic data. So far, we see this as a volatility event rather than an economic event impacting inflation and consumption. Figure 1: Credit spread on high yield and investment grade corporate bonds

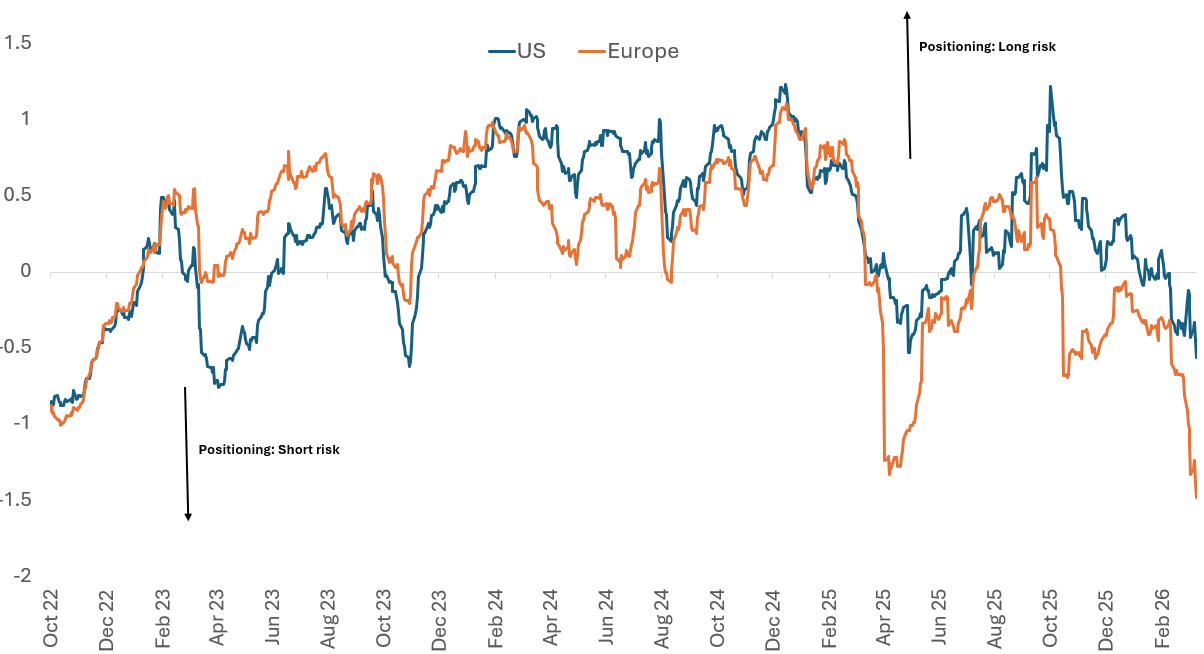

Source: Bloomberg, US HY = US High Yield:ICE BofA US High Yield Index; EUR HY = Euro High Yield: ICE BofA Euro High Yield Index, US IG = US investment grade: ICE BofA US Corporate Index, EUR IG = Euro Investment Grade: ICE BofA Euro Corporate Index, Govt OAS (option adjusted spreads over governments), 01 January 2014 to 13 March 2026. Bps= basis points. Spreads may vary and are not guaranteed. Past performance does not predict future returns. The forces behind corporate credit's resilienceWe believe there are several reasons why the corporate bond markets have responded in such an orderly way. First, investor positioning is light given credit spreads are at the tighter end of historical ranges (Figure 2). Anecdotally, most investors were neutrally positioned heading into this conflict and waiting for more attractive valuations to add risk. Recall that there had been nervousness around artificial intelligence (AI) disruption and private credit fears earlier in the year. Figure 2: Positioning in credit is light, as market trades short

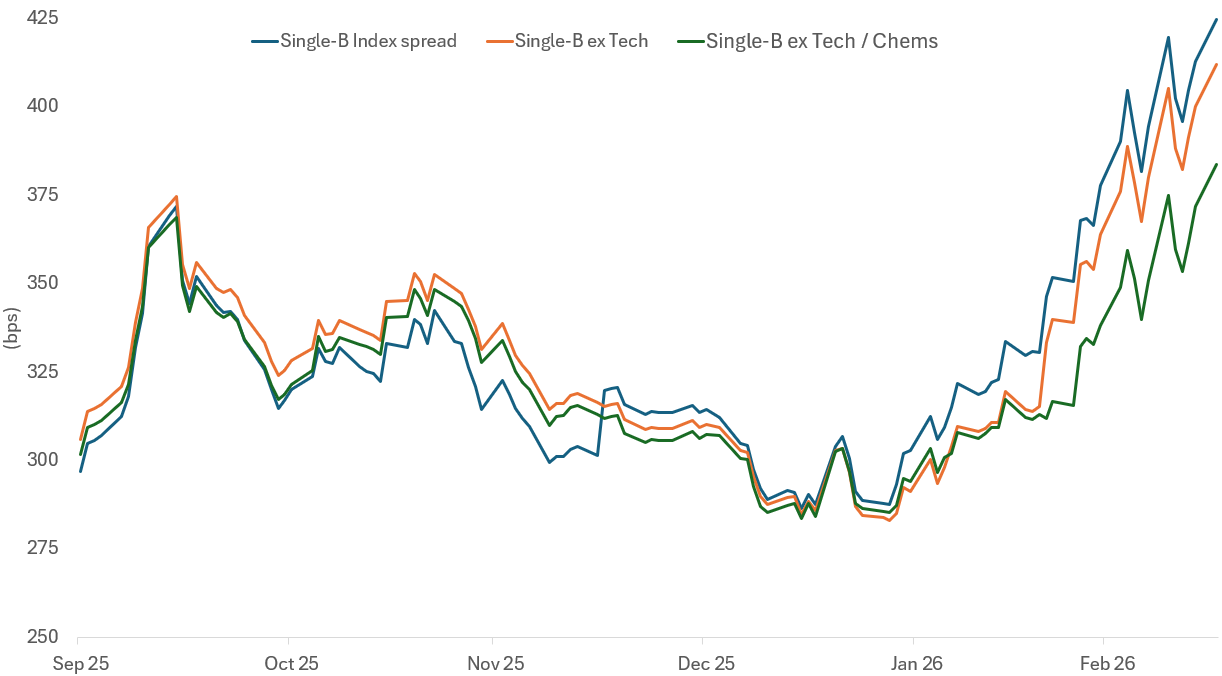

Source: ICI, Bloomberg, DTCC, BNP Paribas. The BNPP Positioning Indicator (BNPPIUS, BNPPIEU) reflects data on dealer inventories, funds' cash balances, Commodity Trading Advisors (CTA) positioning, Credit Default Swap (CDS) market positioning and option hedging, as at 12 March 2026. The BNPP Credit Positioning Indicator shows how long (positive number) or short (negative number) investors are positioned in credit markets, indicating whether exposure to credit risk is extended, neutral or defensive. Second, there has already been a reasonable amount of corporate bond issuance so far this year. US investment grade issuance was US$474 billion in the first 10 weeks of the year, up 6% compared to the same period in 2025, and US high yield and loans (leveraged finance) issuance was US$64 billion, up 34% compared with the same period in 2025. Over the same period European investment grade issuance is €170 billion, down a marginal 3%, but European high yield is €23 billion, up 40% year- on-year.1 A key concern has been the scale of tech-related issuance, particularly for the investment grade market. However, the hyperscalers have made good progress with their capital raising, with Oracle claiming they do not expect to issue any additional bonds for the remainder of the calendar year 2026.2 Taken together, companies have been successful in borrowing earlier in the year which should take some pressure off needing to come to the market in the very near term. The strong technical (market dynamics) picture that has been in place should remain intact. Third, turning to demand, higher yields are already attracting yield sensitive buyers, such as insurance companies stepping in as we have heard anecdotally. Yields on US high yield are back above 7% and are at 5.7% in European high yield. US investment grade is above 5% and European investment grade at 3.5%.3 As explained earlier, a portion of the yield change has been due to the rise in government yields reflecting higher inflation expectations. This has led to a moment of positive correlation between rates and credit spreads, which tends to be temporary. Credit fundamentals resilientAnother backstop to credit spreads is that corporate fundamentals generally remain supportive. Earnings expectations have not rolled over and continue to underpin credit quality. Near�'term earnings face a relatively low hurdle, as Q1 results last year were depressed by tariff speculation, limiting downside risk as we move through the upcoming earnings season. Consensus expectations point to a healthy 20% earnings-per-share growth by Q4 versus Q1, consistent with the typical second�'half earnings catch�'up seen in prior years. Even if those forecasts ultimately prove optimistic, interest rate coverage - earnings covering interest expenses - are broadly stable across investment grade and leveraged finance (high yield and loans). With macro growth still resilient - particularly in the US - credit quality is expected to remain robust enough to absorb market volatility. This provides a supportive macro backdrop for sufficient cashflows to service generally stable and manageable leverage levels. With all�'in yields at attractive levels, fundamentals and earnings serve as the anchor to allow investors to lean into wider spreads where attractive risk-adjusted potential can be captured. This is rather than idiosyncratic risk or geopolitical volatility spooking investors as signalling the start of a more adverse credit cycle. Idiosyncratic stress is rising - but is not systemicTo take a step back then, there is no evidence of a broad earnings downgrade cycle emerging across investment grade or high yield credit. Recent market volatility is increasingly being driven by idiosyncratic rather than broad�'based credit risk, with stress emerging unevenly across sectors and issuers. One area this surfaced in is software, where dispersion widened sharply and price action was severe in specific names as AI-related concerns dominated around revenue displacement. While software is a small component of high-yield indices, the volatility emerged more in the loans market, which has become increasingly bifurcated and private credit. For loans, selective mispriced opportunities have emerged, while CLOs, the main buyer of loans, continue to launch, with many warehouses looking for loans, supporting demand in the near term. This is important as leveraged finance does well in environments where readily available refinancing is present. Private credit, on the other hand, is facing rising redemption pressure. We are seeing headlines around the gating of funds and increased scrutiny of asset values, alongside banks reassessing collateral valuations and pulling back from certain lending relationships. Nevertheless, this adjustment appears to be gradual and uneven, unfolding over time rather than triggering an immediate spillover into public markets. In this context, stress in private markets need not be destabilising for public credit. As capital becomes more cautious it tends to be redeployed conservatively, such as into short-dated bonds or liquid investment grade credit. This may present a modest but constructive technical (demand) for public markets, particularly at a time when yields have become more attractive and markets are sensitive to reward the winners. Rising dispersion from a K-shaped economy

Figure 3: Single Bs are tighter excluding technology and chemicals

Source: Barclays, as 16 March 2026. Spreads may vary and are not guaranteed. Past performance does not predict future returns. For credit investors, this creates an opportunity that is incremental rather than wholesale. Valuations have moved off their tightest levels, but remain far from historic stress points, suggesting scope to add risk selectively. With spreads still tight in aggregate and macro uncertainty elevated, timing and discrimination matter. After all, historical analysis suggests that oil price shocks typically take months to mean-revert once conflicts stabilise. The opportunity therefore lies not in chasing beta, but in leaning into dispersion and adding risk where repricing has been meaningful and fundamentals remain intact, while remaining cautious where valuations have yet to adjust. In that sense, the current environment rewards patience and selectivity, allowing credit investors to engage constructively and with confidence that the forces underpinning resilience remain firmly in place, and in some cases appear to have strengthened. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

20 Mar 2026 - Investment considerations of prolonged uncertainty over Iran

|

Investment considerations of prolonged uncertainty over Iran Janus Henderson Investors March 2026 (8-minute read) The conflict in the Middle East has escalated over the last few days and hopes for a short war have faded. Regional diplomatic efforts to de-escalate appear to be failing and Iran continues to retaliate in response to strikes from the US and Israel. As a result, the Strait of Hormuz - the world's most important gateway for energy commodities - remains effectively closed to all but the most buccaneering of shipping companies. The Strait closure is a result of a lack of insurance, firms not willing to risk the loss of future capacity if ships are sunk, and concerns for the welfare of sailors after several fatalities already. However, there are now risks of more intensive intervention from the US and/or Israel following reports that they are considering putting boots on the ground, either to try and extract Iranian enriched nuclear material or to take Kharg Island, a key sea terminal for Iranian oil exports. At the same time, a new Supreme Leader of Iran has been chosen who is seen as another hardliner. This is unlikely to be taken well by the US, who would have preferred someone more moderate, and the choice appears unlikely to create a path to de-escalation. The desired end point is still uncertainIt is still not immediately clear what the ultimate objectives for the US and Israel are. Various intentions have been publicly stated but it is not clear which of these are red lines and which are just preferences. A further reduction of the potential for Iran to build nuclear weapons appears to be the closest to a requisite. However, given that strikes in 2025 were deemed to have achieved this, defining the outcome is difficult. Similarly, a desire to destroy Iran's long-range missile program has been expressed, but this may similarly be difficult to guarantee. Finally, regime change, either for military or humanitarian reasons, is now touted as a key objective, but it remains unclear how this can be achieved with airstrikes alone. The objective mattersUnderstanding the motivating objectives is important when considering how long the war might last and the subsequent economic impact. We can look to several factors that suggest this could be a more prolonged campaign. Iran has indicated that it can continue with its current rate of response for six months, far longer than the weeks-long engagement that markets appeared to have been pricing. The US has expressed that it wishes to remove the previously enriched uranium that could be used in nuclear weapons, but it has been a long time since the last international inspection and its whereabouts are likely to be very uncertain. Similarly, the continuity of a new hardline leader suggests that Iran is feeling little pressure to change tack yet. However, there are also ways in which the conflict could be wound up sooner. The most obvious is that US President Trump has shown a willingness to abruptly change direction on policy multiple times throughout his leadership, no matter the scale of the impact. With mid-term elections coming up later in the year, the US government is likely to be highly sensitive to anything that pushes up the cost of living. Therefore, finding a way to declare victory and return oil prices to lower levels may ultimately dominate any longer-term military objectives. The length mattersA longer-term conflict raises the danger of greater destabilisation in the region, creates greater potential for more severe damage to key infrastructure and risks longer-lasting impact on energy supplies. While there are some ways to mitigate the impact in the near term, such as sending oil through pipelines to ports less likely to be targeted, or by releasing strategic reserves outside of the Middle East, these are either inherently temporary or lack the potential capacity to offset prolonged restrictions in the Strait of Hormuz. Oil is often seen as the key commodity when considering conflicts in the Middle East, given its relevance to US gasoline prices in particular, but natural gas supplies are crucial for other regions, such as Europe, and other base products feed into areas from chemicals to fertilisers. Last week, markets appeared to be pricing energy commodities in line with a short-term interruption to the ease of supply. Assumptions around this appear to have changed over the weekend, with prices now moving to incorporate greater risk of a prolonged engagement. The lack of clarity around the US/Israeli objectives does nothing to reduce the uncertainty that markets hate. Impact on marketsThe price of oil has spiked above US$100 per barrel as concerns about supplies have intensified. European natural gas prices have almost doubled since the end of February. This is raising the spectre of the inflationary impulse generated by the Russian invasion of Ukraine in early 2022 and the subsequent removal of much of the Russian supply into energy markets. Concerns about a jump in European inflation or simply prolonged stickiness in the US are lifting bond yields. US Treasury yields have moved higher as markets have taken out one of the US Federal Reserve interest rate cuts that were anticipated by the end of the year. Yields on 10-year Treasuries have seen less movement than their European counterparts, as US jobs numbers on Friday served to offset some upward yield pressure from expected inflation. Concerns about inflation have seen surges in German and UK breakeven rates, with market pricing for the European Central Bank interest rates at the end of 2026 now looking at over 1.5 hikes. Since the end of February, expectations for the Bank of England have shifted from two cuts by the end of 2026 to a better than 50:50 chance that there will be an interest rate hike - a marked shift in the outlook. Markets are now pricing in higher oil prices for the foreseeable future, with concerns mounting about a stagflationary outcome, should higher energy costs stall a re-acceleration in economic growth. The uncertainty has provided support for the much-maligned US dollar, given the American economy is looking better set to weather an energy shock than elsewhere. However, higher bond yields and a stronger greenback have dampened gold's ability to rally in the current environment, following strong performance during other recent periods of volatility. Equity markets are seeing something of a reversal of recent performance dynamics. Markets that started the year positively, to the end of February, suddenly look under greater pressure. A stronger dollar and higher oil prices are weighing on Asian stocks that had been surging in the first two months of the year. Gas prices remain Europe's geopolitical Achilles heel and markets are clearly concerned that the region is overly exposed again. In the US, last week saw some signs of a reversal of the recent outperformance of Value stocks over their Growth counterparts. AI-related stocks have struggled in 2026 so far compared to the rest of the market, but the fears that higher oil prices could dent the very rosy economic outlook are leading to something of a reconsideration. The effective closure of the Strait of Hormuz is unprecedented, undoubtedly making for severe impacts on risk assets. However, to put the sell-off in proper context, investors must also recognise that equities entered the conflict trading at a meaningful premium over historical valuation levels. The forward price/earnings ratios (P/Es) of major global equity markets were at top quartile levels versus their 20-year histories[1], roughly a 15%-30% premium compared to median levels. Indeed, the markets experiencing the largest sell-offs are the ones that entered the conflict with the highest returns year to date[2]. Risks of a prolonged war but don't rule out a quick "victory"Situations like this demonstrate the value of well-diversified multi-asset portfolios. Geopolitical events are rarely easy to gain complete clarity on, with the current US administration apparently embracing uncertainty as a negotiation strategy. What we can take away from the events of the last few days is that it is likely the conflict could last longer than many had initially hoped. This means there is the potential for greater economic impact - and markets have moved to price in this change. There is the potential for faster inflation and slower economic growth, with assets focusing on different aspects thus far. However, risks remain two-sided. US political pressures means that a quick "victory" should not be ruled out. Asset prices, driven by energy prices, are likely to swing violently as investors alter their expectations for either outcome. [1] Source: Datastream, 27 February 2026. Past performance does not predict future returns. [2] Source: Bloomberg, 31 December 2025 to 9 March 2026. Past performance does not predict future returns. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

18 Feb 2026 - Australian economic view - February 2026

|

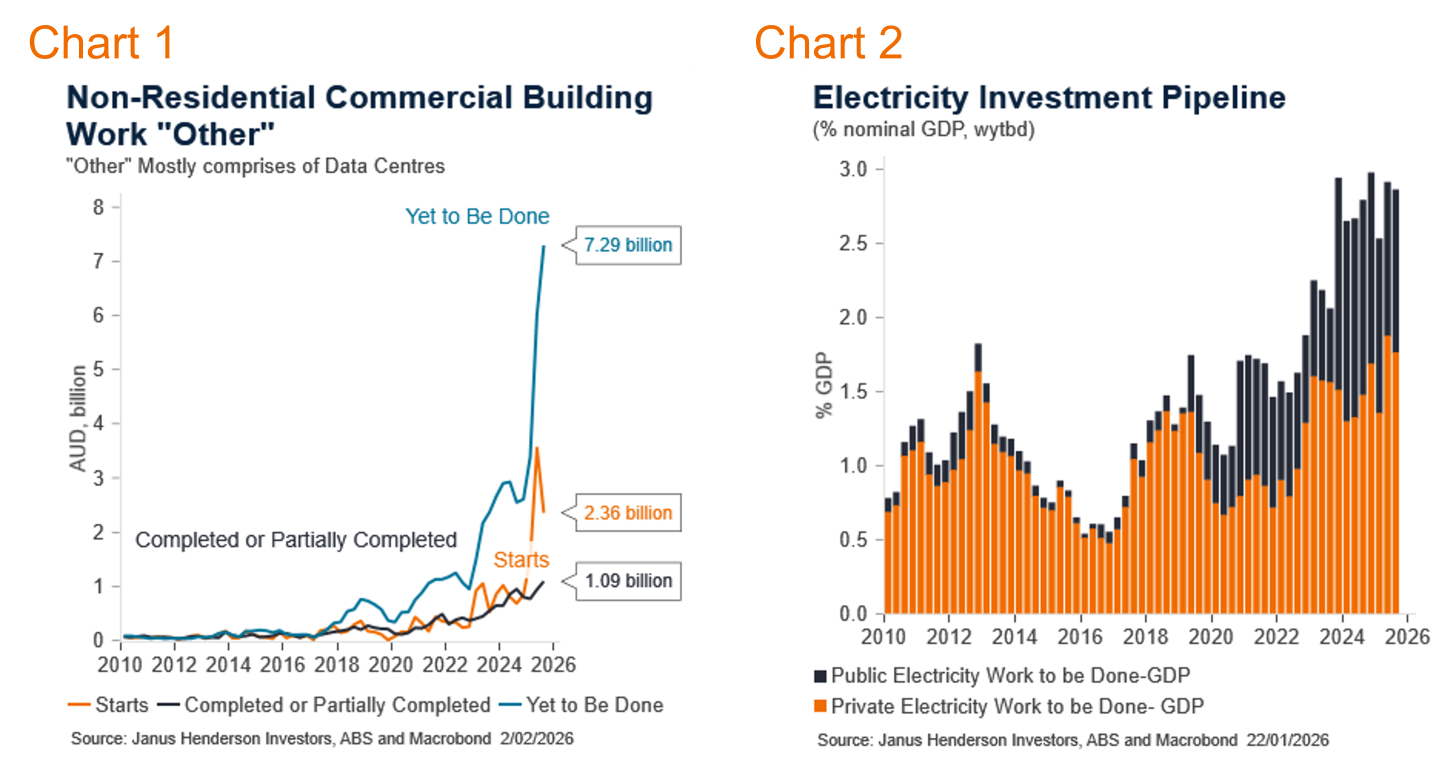

Australian economic view - February 2026 Janus Henderson Investors February 2026 (7-minute read) Market reviewSolid domestic data contributed to reinforcing near term lift in yields. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.21%. The Reserve Bank of Australia (RBA) did not meet in January, therefore the cash rate remained at 3.60%. Three-month bank bills rose 10 basis points (bps) to 3.84% by month end. Six-month bank bill yields fell 3bps to 4.09%. Australia's three-year government bond yields ended the month 13bps higher, at 4.27%, 10-year government bond yields were 7bps higher at 4.81%. January was an extraordinary month in terms of global, geopolitical events and central bank uncertainty. From the US demanding Greenland, to ousting the Venezuelan leader, and instigating a criminal probe into Federal Reserve Chair Powell. What is more remarkable is the market's mostly benign response to the newsflow. Amid a general level of uncertainty, demand for assets continues to outweigh any potential global blowback. Peripheral markets are showing the impacts, volatility in gold and silver prices and a weakening US dollar are key indicators of that unease. While these broad events are ongoing, providing a backdrop to the domestic market, at this point, they are not driving them. The local economy shows elevated inflation, with the RBA's main measure, the trimmed mean quarterly series, at 3.4%yoy. The new monthly headline series remains at 3.8%. A series of administrative prices and one-offs have driven the headlines. Underlying this is steadying energy and rent prices, proving some degree of comfort ahead. The labour market remains highly volatile, with large changes month-to-month. The unemployment rate has dropped to 4.1%, but employment growth is low. Consumer confidence has dropped on the prospect of higher interest rate increases, while major city house prices are similarly subdued. A case for RBA hikes can be made this year. The upcoming artificial intelligence (AI) related capital expenditure cycle is expected to contribute significantly to demand and come up against supply constraints. Much of this comes in H2 and beyond. Initially, the household sector remains sensitive but should stabilise. Risk markets continued their solid momentum into 2026. Domestically, corporate and structured credit primary markets opened strongly with a range of issuers issuing bonds. Against a broadly constructive background for credit, the Australian iTraxx Index closed 2bps wider at 66bps, while the Australian fixed and floating rate credit indices returned +0.32% and +0.46% respectively. Market outlookWe have updated our RBA base case, looking for a series of hikes through 2026, into 2027. While our hikes are later than current market pricing, they move higher than that priced into 2027. Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected in H1 2026, continuing higher through the year and into 2027. This has a 10% weight. Our low case reflects a weaker economic outcome, if global uncertainties are renewed and the labour market deteriorates. We hold a modest long duration position, targeted on the curve, and remain vigilant to take advantage of market mispricing. Monthly focus - Make way for AI InvestmentThe AI investment boom is upon us, we knew it was coming but the third quarter of 2025 showed that its appearance was perhaps sooner than expected. The trajectory is by no means guaranteed. There is a desire by policy makers, and players alike, to facilitate progress but some perspective on quantum, and constraints, provide a useful guideline to the path ahead. The AI sector influence on the economy initially shows up in investment. The productivity enhancements come later. Australia is seen as having a comparative advantage in terms of global geopolitics, economic conditions and availability of renewable energy sources. Given this, it is reported that the build and placement of data centres (DC) in Australia is higher than in comparative countries. Australia will benefit from setting up DC in Australia that service both local and non-Australian clients. The rise in DC building has been dramatic. This captured economist's attention in the third quarter data set, surging ahead. To Q3 2025, per quarter, actual building steadily rose at A$1.1bn, starts have surged to A$2.4bn but all eyes on the work yet to be done (WYTBD) at A$7.3bn. WYTBD are committed, approved developments that are expected to proceed in the next year. While not all will go through, a significant proportion is expected to be developed. The Q3 data for starts is also indicative of the possible pathways. It may not be a smooth process; delays can be expected. These represent a powerful rise in the sector. Mapped against the overall economy though, it may be smaller. The datacentre WYTBD is around 0.25% of nominal GDP at this stage. There have been numerous announcements regarding the pipeline for DC build commitments that will not be in the official ABS data.

If we assume the A$7.6bn increase, then deflate by target inflation, the rise in real private non-residential capital expenditure is an admirable 20%. Assuming it isn't implemented all at once and smooth the spend over multiple years, this would imply an approximate 0.4 percentage point rise in the contribution to real GDP per year. This is not to be ignored, but equally it doesn't suggest another boom period. However, if the media announcements are to be believed, there is a long-term pipeline of around A$150bn. If, and this is a big assumption, this comes about, then there could be a significant contribution to real GDP over a decade. This includes spending on the inputs, such as energy and water, as well as software. There are challenges to the projected implementation of datacentre construction. There has been a crowding out of construction as the public sector utilised available labour and inputs to building, creating roadblocks to rapid build out in the private sector. This will ease as the public build moderates. Energy and Transmission Energy is significant for DC and AI. DC are energy intensive and have huge energy, and thus transmission, needs. Increasingly, DC are saying they will provide their own energy, predominantly through renewables. The electricity building on WYTBD is larger than that of DC, and while AI and DC are a large part of this, the changing needs of the entire energy sector is also behind the ramp up. The WYTBD now equates to just shy of 3% of GDP on a nominal basis. Much of the acceleration since 2024 has been in the public sector, while private plans have been flat, after a sharp rise though 2022-2023. That will need to change if private energy generation is to be used to meet the new AI needs. Given the increasing focus on the social aspect of energy, and water, usage, often referred to as the energy trilemma of reliability, affordability and sustainability, combined with tight supply and rising costs, it should be expected that heavy users such as DC, and others, will meet their energy needs outside of the public provision. This can be represented as a capital expenditure tailwind, or an investment headwind. It is likely there is a bit of both. Some investors will be able to go ahead with private access to their energy, and water, needs. Others will see the costs, delays and social license as too high a barrier. Spending on actual AI itself will likely increasingly factor into the equation. Overall software spend has already surpassed the late 1990's boom and should further increase. As AI becomes cheaper per user, and other versions appear, this growth may slow. The generalised rise in overall spend thus far is also likely to represent the increased digitisation of lives and workforces that was already underway. AI adds to this. We would consider the contribution to growth to maintain on a steady path from here. Views as at 1 February 2025. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

19 Dec 2025 - Capitalizing on volatility in sustainable equities - a strategic approach to uncertainty

|

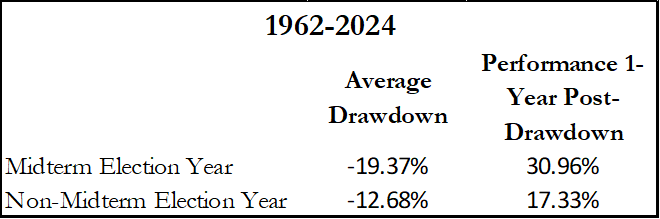

Capitalizing on volatility in sustainable equities - a strategic approach to uncertainty Janus Henderson Investors December 2025 (7-minute read) While we apply a bottom-up stock picking process it is important to have a macro view overlay to guide us on portfolio construction. The rate of change, whether it is societal, geopolitical, or technological continues to increase exponentially and this argues for active management over passive. There are three key macro topics that we are watching particularly closely as we move towards 2026. The first is everyone's favorite topic of artificial intelligence (AI). The second is the overall health of the economy and what we expect to see from the Trump administration. And last but not least is private credit. Why AI is not a bubbleFirst on AI, no, it is not a bubble. Yes, there will be some misallocation of capital and an ensuing market downturn sometime in the next five years just as we have seen with every new technology going back hundreds of years. We acknowledge the non-zero probability that large language models (LLMs) prove to be a dead end to true artificial general intelligence (AGI); however, we are also comforted by our meetings with companies that are citing use cases that are already driving significant costs savings. We do not think AI is currently in a bubble, because ultimately it comes down to supply and demand. Unlike the commercial internet where you just dug a hole and laid some fiber, AI compute is infinitely more physically challenging to incrementally produce. To provide perspective, to produce a one-gigawatt (GW) data center that will run LLMs, it requires six football fields of land along with over 200,000 tons of equipment such as cables, heating, ventilation and air conditioning (HVAC), transformers, etc.1 There are legitimate questions around if we even have enough electricity and skilled tradespeople to address a fraction of the tens of GWs of data centers that have been announced. On the demand side, anecdotes suggest a waiting list of 20 different customers for each newly installed Nvidia graphics processing unit (GPU) at a data center. We will continue to pay close attention to companies addressing key bottlenecks (such as Nvidia, Prysmian, Schneider, ) that are acting as a governor on the adoption of AI. Further, we will continue to remain vigilant to AI exposed companies where valuations may be implying too optimistic of a scenario while also taking advantage of any irrational selloffs in AI exposed names. We feel that we are still early in the AI capital expenditure (capex) cycle and there is still significant outperformance to be had by investing in this space. Running the economy hot: fiscal and monetary support aheadOn the topic of the U.S. and global economy, while there are certainly some wobbles in the consumer spending and confidence (particularly the bottom 80%) we expect significant fiscal and monetary support taking hold over the next five months. Indications are that Trump is going to run the economy hot through the mid-term election a year from now. We should expect significant tax refunds both for individuals and corporations in the first few months of next year due to the One Big Beautiful Bill (OBBB). We should also expect other initiatives from the Trump administration focused on bringing down costs in housing and healthcare along with the possibility of some form of helicopter money (US$2,000 has been floated as a giveaway to those making US$100,000 or less). Finally, we expect the U.S. Federal Reserve and U.S. Treasury to work in coordination and independently in bringing down interest rates and Treasury bill price volatility. All of this should be supportive of the economy and asset prices. For the stock market, in the short term, liquidity is one of the biggest drivers of performance and we should expect other countries to get involved as well. We are starting to see signs that China will implement further initiatives to support the local property market while Japan is proposing the most Federal spending since the pandemic. All of this is probably inflationary and one of the best defenses is to own finite assets like equities. We have a bias toward investing in companies that help to drive efficiencies in society and are thus deflationary. In our view, these companies should do well in an inflationary environment. With all of that said, next year is a mid-term election year which has historically brought about greater equity market volatility. The average peak-to-trough decline within the S&P 500 during an election year has been almost 20% going back to 1962. The good news is that these declines represent great buying opportunities as the 1-year return following these market troughs has averaged 31%. We again look forward to taking advantage of this volatility. Exhibit 1: S&P 500 price return 12-month period following a mid-term election

Source: Strategas, as at 25 November 2025. Why we're steering clear of leverage in an uncertain credit landscapeRegarding the last topic of private credit, this may not be a story specific to 2026, but it is worth noting given the events around the First Brands and TriColor scandals this year. Having gone through a couple of credit cycles in our careers, we have started to get a sense of déjà vu. What is different this time is that it appears that more of the risk has moved to cashflow-driven direct lending private credit and away from the banks (although banks may not be immune as roughly 10% of their U.S. loans are now to non-bank financial institutions). Unfortunately, given not all private credit is transparent, this means that the market will have much less early warning if something is wrong. Private credit is of course not all created equal. Some private credit and private equity houses have historically boasted about their high sharpe ratios and low volatility in underlying asset prices. But in certain instances, this was a function of and not having to worry about marked-to-market valuations. Some private credit houses have also enlisted other questionable strategies such as payment in kind (PIK) and maturity extensions. Banks have never had that privilege and thus we started to see warning signs on credit in 2006 and 2007. What we find concerning in pockets of private credit, along with the above tactics, is the potential conflict of interest as it is estimated that between 70% and 80% private credit loans have the same private equity sponsor. We are starting to see credit risk increase with a recent example of Renovo, a private equity backed home improvement contractor that went bankrupt and reported only US$50,000 in assets versus US$150 million in private credit loans. In 2026 there will be a need to look beneath the bonnet at the robustness of private credit processes, particularly in the diverse direct lending arena. In a scenario where there is a downturn in credit, investors will be well served by avoiding excessive balance sheet leverage and owning companies with mission critical products and services that tend to be more immune to economic downturns. Conclusion: Be prepared to benefit from disruptionIn an environment defined by accelerating change and heightened uncertainty, we believe there will be a clear need for disciplined bottom-up stock selection, combined with a thoughtful macro-overlay. This should be focused on identifying companies that are both resilient and aligned with long-term structural trends. By actively navigating opportunities in AI, remaining vigilant on economic policy shifts, and avoiding any hidden risks in private credit, our aim will be to capitalize on volatility rather than be constrained by it. History shows that periods of disruption create some of the most compelling investment opportunities - and investors should be prepared to seize them. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund Disclaimer: This article reflects the views of the author(s) at the date of publication and does not necessarily represent those of FundMonitors.com. It is provided for general information only and does not constitute investment advice or a recommendation to buy or sell any security. Market data, views, and forward-looking statements were current as at 1 October 2025 and may change without notice. Past performance is not indicative of future results. Readers should consider their own objectives and obtain professional advice before making investment decisions. 1Citrini, 'Stargate: A Citrini Field Trip', (7 November 2025). Active investing: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis, and the investment choices they make. The opposite of passive investing. Artificial General Intelligence (AGI): A form of AI with the ability to understand, learn, and apply knowledge in a way that is indistinguishable from a human. Artificial Intelligence (AI): The simulation of human intelligence in machines that are programmed to think and learn. Balance sheet leverage: The use of borrowed funds in addition to equity to finance the purchase of assets. Bottom-Up stock picking: An investment strategy that focuses on analyzing individual stocks and their fundamentals rather than considering broader economic or market factors. Capital expenditure: Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment, or vehicles in order to maintain or improve operations and foster future growth. Helicopter money: A type of monetary policy that involves printing large sums of money and distributing it to the public to stimulate the economy. Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures; the opposite of deflation. Large Language Models (LLMs): A type of AI model that is trained to understand and generate human language text. Liquidity/Liquid assets: Liquidity is a measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as 'liquid'. Midterm Election: An election that occurs in the middle of a president's term, often leading to changes in the composition of Congress. The One Big Beautiful Bill (OBBB) is a major U.S. federal statute enacted on 4 July 2025. The bill represents the centerpiece of President Donald Trump's second-term legislative agenda and includes sweeping changes across tax policy, social programs, and federal spending priorities. Passive investing: An investment approach that involves tracking a particular market or index. It is called passive because it seeks to mirror an index, either fully or partially replicating it, rather than actively picking or choosing stocks to hold. The primary benefit of passive investing is exposure to a particular market with generally lower fees than you might find on an actively-managed fund, the opposite of active investing. Payment in Kind (PIK): A type of financing where interest payments are made in the form of additional debt rather than cash. Pretend and Extend: A strategy used in credit markets where lenders extend the terms of a loan to delay recognising a problem loan as non-performing. Private credit: Non-bank lending provided by private institutions, often involving loans to small and medium-sized businesses. Sharpe ratio: This measures a portfolio's risk-adjusted performance for the purpose of measuring how far a portfolio's return can be attributed to fund manager skill as opposed to excessive risk taking. A high Sharpe ratio indicates a better risk-adjusted return. Treasuries/US Treasury securities: Debt obligations issued by the US government. With government bonds, the investor is a creditor of the government. Treasury bills and US government bonds are guaranteed by the full faith and credit of the US government. They are generally considered to be free of credit risk and typically carry lower yields than other securities. Valuation metrics: Metrics used to gauge a company's performance, financial health, and expectations for future earnings, e.g. P/E ratio and ROE. Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility, the higher the risk of the investment. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

31 Oct 2025 - Janus Henderson x Berkeley Insight Collective: Evaluating corporate transition plans - from theory t

|

Janus Henderson x Berkeley Insight Collective: Evaluating corporate transition plans - from theory to engagement Janus Henderson Investors October 2025 (7-minute read) Drawing on insights from Dara O'Rourke, Associate Professor at UC Berkeley, we explore why a holistic evaluation of climate transition is important - and how our proprietary Climate Transition Assessment (CTA) -- shaped by key learnings from the Berkeley curriculum -- enables investors to better evaluate corporate climate transition plans. Financial materiality of climate riskAs part of the co-developed Janus Henderson x Berkeley Insight Collective curriculum, our investment teams explored how climate change is not only a sustainability issue for investors -- it's a material financial risk. A company's climate transition plan is a strategic commitment that provides investors with essential insight into how the business intends to allocate capital, manage long-term risks, and seize opportunities in the shift to a low-carbon economy - all of which are critical to sustaining competitiveness and value creation. Companies without credible transition plans face mounting exposure to business disruptions, regulatory pressure, reputational damage, and the risk of stranded assets. Those that fail to align their strategies with climate realities may also risk losing their social license to operate -- not only in the eyes of regulators and investors, but in the markets they serve. The question is no longer whether firms should transition, but how credibly they can do so. From the outside, it's often difficult to tell which companies are truly implementing credible transition plans. We believe leaders in this transition will be those that combine bold ambition with tangible action, and strong governance with measurable progress. Dara O'Rourke, Associate Professor at UC Berkeley's Rausser College of Natural Resources:

Elevating engagements through proprietary dataTransition readiness doesn't just help us evaluate companies -- it shapes how we engage with them. Leveraging our proprietary research and data to understand how companies plan to navigate the transition not only informs our investment evaluation, but also shapes how we engage with them. We can tailor our conversations and engagement strategies to specific gaps we identify - helping ensure that capital is aligned with credible, forward-looking strategies. For example, if a company shows strong ambition and governance but weak investment, we can encourage capital expenditure alignment and clearer implementation plans. If a company's achievements are trailing despite having the right frameworks in place, our focus may shift towards enhancing transparency and setting interim milestones. This data-driven strategy allows us to transcend generic interactions and pose questions that are precise, relevant, and rooted in solid data. Assessing the building blocks of a transition plan -- what we look forTo support deeper analysis of climate-related risks and opportunities, we've developed a proprietary, data-driven Climate Transition Assessment (CTA) tool, leveraging insights from our co-developed curriculum with UC Berkeley. Available to all our investors and analysts, this tool draws on dozens of data points from third party providers and applies our proprietary scoring methodology. The CTA evaluates companies across four strategic dimensions - our '4-As' framework:

Ambition is where a company signals its intent. We assess whether that intent is credible, comprehensive, and aligned with global climate goals. This includes the scope and timelines of emissions reduction targets, reliance on offsets, and whether targets are validated by the Science Based Targets initiative (SBTi). Near-term targets are especially important. We also consider whether ambition is grounded in science -- using third-party metrics like implied temperature rise and peer-relative transition scores -- and whether the company's targets reflect its sectoral carbon budget. Action is where ambition becomes operational. We assess whether companies are investing in the transition through capital allocation, operational changes, and innovation. This includes climate-aligned CapEx (capital expenditure) and OpEx (operational expenditure), green revenues, supply chain engagement, deployment of low-carbon technologies and internal carbon pricing. This helps us determine whether a company is actively aligning its strategy with a low-carbon future. Accountability is arguably the most important dimension - it's what turns ambitions into execution and ensures that climate goals are treated with the same seriousness and financial ones. A company can have high ambitions and even take action toward them, but without governance structures that embed climate into decision-making, progress is fragile. We assess whether climate oversight exists at board level, whether executive compensation is linked to sustainability, and whether disclosure practices are in place. We also look for internal actionable metrics -- such as business unit-level KPIs (key performance indicators) or climate-linked performance reviews -- that translate climate goals into day-to-day operations. Governance risks like pay controversies, shareholder dissent, and leadership concerns also inform our view of credibility. Achievements is the ultimate test: is the company delivering results? We assess emissions trends, absolute emissions and carbon intensity, and performance relative to peers. While results must be interpreted in context, they are a critical indicator of credibility. A company may not be hitting every target-- emissions may even be rising -- but if ambition, action, and accountability are strong, we see a clear and credible path to decarbonisation. Temporary emission increases due to acquisitions or strategic investments -- especially in decarbonising technologies -- may be justifiable, but over time, progress must be evident and consistent with stated goals. Our CTA in actionIn a recent engagement with a transportation equipment manufacturer, our CTA revealed a disconnect between the company's stated ambition and its execution. While the company set a 1.5°C-aligned target for Scope 1 and 2 emissions, the lack of SBTi validation and limited investment in green activities raised questions about credibility. The CTA also flagged gaps in verification and capital allocation, prompting us to dig deeper. We asked targeted questions on executive incentives, scenario analysis, and internal carbon pricing -- all informed by the CTA's findings. The company confirmed that while it does not plan to seek SBTi validation, it conducts scenario analysis, applies carbon pricing in select regions, and links sustainability goals to executive bonuses. Our data-driven engagement didn't just highlight gaps -- it enabled a more focused, informed, and ultimately productive dialogue. Dara O'Rourke, Associate Professor at UC Berkeley's Rausser College of Natural Resources:

Key conclusionsClimate transition plans are no longer optional -- they are a financial imperative. Our proprietary data tools and informed client engagements provide clarity to a fragmented and inconsistent landscape, helping investors distinguish between companies that are genuinely aligned with the transition and those that are not. We believe comprehensive investment insights lead to better-functioning markets by enabling more effective comparison across companies, supporting efficient capital allocation, and reducing the risk of misinformed investment decisions. Our comprehensive research and data tools strengthen our ability to better manage financially material risks for our clients-- from stranded assets and regulatory penalties to reputational damage and long-term value erosion. By evaluating ambition, action, accountability, and achievements in an integrated framework, we can engage with precision -- asking the right question to drive targeted outcomes., In a rapidly evolving landscape, these insights help us manage climate risk, protect portfolios, and support the shift to a more sustainable economy. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund Disclaimer: This article reflects the views of the author(s) at the date of publication and does not necessarily represent those of FundMonitors.com. It is provided for general information only and does not constitute investment advice or a recommendation to buy or sell any security. Market data, views, and forward-looking statements were current as at 1 October 2025 and may change without notice. Past performance is not indicative of future results. Readers should consider their own objectives and obtain professional advice before making investment decisions. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

16 Oct 2025 - Australian economic view - October 2025

|

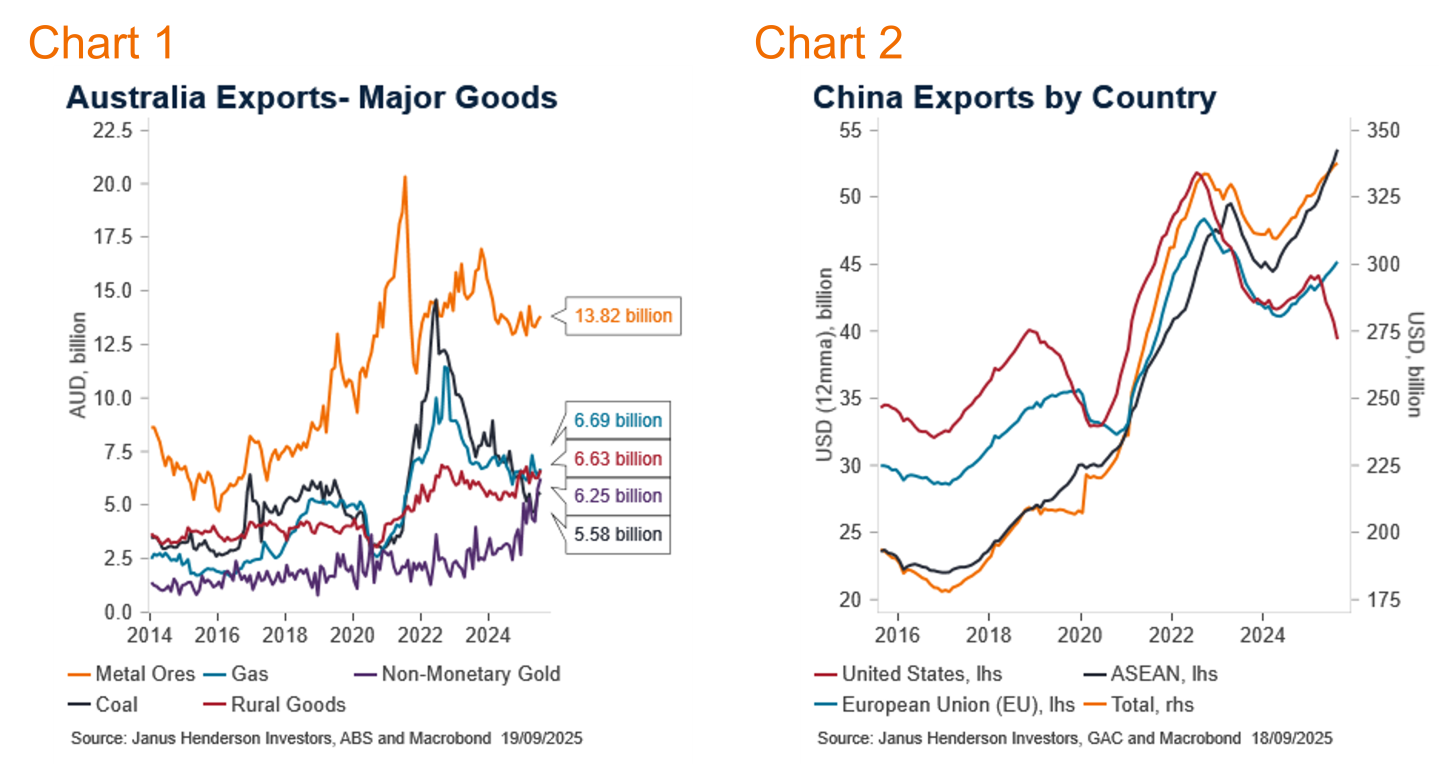

Australian economic view - October 2025 Janus Henderson Investors October 2025 (Originally published by Janus Henderson Investors on 1 October 2025) Emma Lawson, Fixed Interest Strategist - Macroeconomics in the Janus Henderson Australian Fixed Interest team, provides her Australian economic analysis and market outlook. Market reviewAustralian bond markets saw a repricing of the Reserve Bank of Australia (RBA) in September. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.1%. The RBA maintained the cash rate at 3.60%, as was expected. Three-month bank bills were steady at 3.58% by month end. Six-month bank bill yields rose 9 basis points (bps) to 3.66%. Australia's three-year government bond yields ended the month 15bps higher, at 3.55%, while 10-year government bond yields were 2bp higher at 4.30%. While global ructions continued in the background, it was the local data that drove the big moves in local yields. Second quarter GDP was a touch higher than expected, with a pick-up in household consumption. There are continued concerns around the transition between a softer public sector and a better off household sector, so better than expected spending news was welcome. That transition isn't entirely guaranteed, with employment growth dropping again. Although, with the unemployment rate steady, through lower participation, the RBA is less concerned about a softening labour market. The inflation side of the RBA's mandate captured more attention, with the volatile monthly series precipitating renewed inflation concerns. The headline series was higher than expected, at 3%yoy, returning to the top of the RBA's target band. In the details, market services, strongly related to the labour market, was higher and led to the RBA's heightened inflation awareness in their recent press conference. This cloudy picture has the RBA returning to a highly data dependent stance. The global backdrop shows a slowing US economy, countered by the renewed Federal Reserve easing cycle. The Chinese economy remains lacklustre, while global trade continues to be uncertain. High government debt levels remain a concern for bond markets in the UK, parts of Europe and Japan. Market outlookRenewed inflation concerns have seen a repricing of the RBA's expected path higher, with a low in the cash rate at 3.30% in August 2026. This is higher than our base case for the RBA to ease a further 75bps to 2.85%. Our low case reflects a weaker economic outcome and the RBA easing by a total of 250bps. We allocate a modest weight to the low case. We hold a small, long duration position to take advantage of some of the lift in yields, while we remain vigilant through the volatility to take advantage of two-way mispricing. Monthly focus - Global trade still to play outThe US implemented decades high and comprehensive tariffs across the globe throughout the last six months. The global economy has absorbed these thus far, seemingly defying initial concerns. There are increasing signs of a slowing in global trade and adjustments in existing trade relationships. We expect the transition to a new set of trading relationships to slowly continue. Australia's direct tariffs from the US are at the low end of the range, at 10%, and our trade with the US is a small proportion of total trade. As such, the direct impacts from the US' policy were always expected to be limited. Concerns centre on the indirect impact of trade with our largest trading partners including China, Japan, South Korea, Taiwan and India. Thus far, all is well. Australian exports are tracking comfortably. Goods exports have been solid, while services recover from Covid era weakness. However, there are signs that global policies have not yet been fully absorbed by the global economy, and the time to relax, considering these fundamental changes, has not yet arrived. Australian exports are a function of broad global economic growth. The stop-start and uncertain nature of the global tariff implementation has pushed back the expected impact they will have on global economic growth, but not fully eliminated it. The tariff pressure has now started to build, and we see global demand levels easing off. China's GDP is slowing, due to tariff impacts but also domestic factors, and demand for iron ore and coal are slowing along with it. Nominal trade values have picked up as prices have improved, but volumes are lower. This bodes poorly for the future as demand is easing at the point where global competing sources of iron ore are about to rise. One bright export light is non-monetary gold. Gold exports have risen sharply, along with the rise in prices, to make it a major export good, besting coal. Rural goods are also holding well. Services exports have partially recovered from their pandemic slump. Net personal travel remains soft, albeit off its recent lows. Education services exports lifted to above pre-pandemic highs but have now stalled. Changing global education demand and regulation have tempered additional growth. A loosening of domestic policy and reinvigoration of Chinese and Indian student demand are required to elicit a resumption of higher growth from current levels.

Global patterns are showing signs of slowing goods exports, particularly to the US. China, for example, has seen a sharp slowing of exports to the US, but a concomitant pick-up in exports to its Asian neighbours. The sustainability of these redirected flows may be challenged if found to be re-exports and thus attracting even higher tariff rates. For now, the flows are in flux, and yet to find a new equilibrium. History tells us that higher tariff rates will always reduce trade volumes, and in turn global growth. What we have learnt this time, is that the process can take significantly longer to flow through due to the uncertain and inconsistent nature of the implementation. It would be premature to ignore the historical experience of poorer macro-outcomes in the face of higher trade restrictions. We anticipate an easing in iron ore exports over the coming year, and a generalised moderation in broad export growth, based on lower global economic activity. As domestic consumption improves, and the stated defence spending increase is delivered, import growth is expected to rise. As a result, we forecast a deterioration in Australia's net trade position, which will be a net detractor for GDP through 2026 and into 2027. |

|