Join L1 Capital International's CIO, David Steinthal, for an update on the investment environment, positioning of the L1 Capital International Fund (Managed Fund) and key takeaways from the recent results season.

Last week's Hedge Clippings commentary focused on global politics, particularly the US presidential election. Biden remains in the race despite declining Democratic support, while Trump, bolstered by his MAGA base, continues to dominate.

Read more...

19 Jul 2024 - Hedge Clippings |19 July 2024

By: FundMonitors.com

Hedge Clippings | 19 July 2024

Last week's Hedge Clippings' commentary (and the one before that) dealt almost exclusively with global politics and elections, and inevitably a focus on the US. As much as we'd like to think we were ahead of the curve, we can't claim access to any crystal ball, and the rest, as they say, is history. However, when it comes to US Presidents, a combination of history - 15 attempted assassinations since 1835, four successful - plus the polarising nature of the current campaign, one shouldn't really be surprised. Maybe those statistics give the answer to the question we've frequently asked: "How come in a country of 330 million, the only two candidates they can find are Trump and Biden"? Maybe not many of them like the odds!

As we write, Joe Biden, seemingly one of a dwindling number of Democrats who think he should stand, is still in the race. Trump, rather than being deterred, is emboldened, as are his MAGA supporters as Trump is speaking at his party's nomination. A cynic would suggest he's milking last weekend's event for all it's worth among the Republican faithful, but what else would you expect? You have to give him points for presentation.

Less excited about the potential for Trump's return would be Ukaine's Volodomyr Zelensky, Taiwan's Lai Ching Te, and quite possibly China's Xi Jinping, although the latter may think his task of enveloping Taiwan might now be easier. If nothing else, the next four years will be interesting.

Enough of that! On to the economy...

US inflation has fallen such that Fed Chair Powell has hinted they'll start cutting rates later this year, while at the same time the potential for the RBA to raise Australian rates at their upcoming August meeting is likely to be dependent on CPI data due on 31 July. The RBA's narrow path seems to be getting narrower, as inflation stays high, keeping interest rates high, which in turn have slowed Australia's two speed economy to a crawl. Far from a narrow path, the risk is we reach a tipping point.

19 Jul 2024Performance Report: 4D Global Infrastructure Fund...FundMonitors.com

The 4D Global Infrastructure Fund (Unhedged) since inception in March 2016, has returned +8.4% per annum, a difference of +0.13% relative to the S&P...

Read more

19 Jul 2024 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

The Bennelong Twenty20 Australian Equities Fund rose by +1.06% in June, outperforming the ASX 200 Total Return benchmark by +0.05%. Since inception...

Read more

18 Jul 2024 - Performance Report: Bennelong Twenty20 Australian Equities Fund

By: FundMonitors.com

[Current Manager Report if available]

18 Jul 2024Performance Report: Altor AltFi Income FundFundMonitors.com

The Altor AltFi Income Fund rose by +0.82% in June, outperforming the RBA Cash Rate + 5% benchmark by +0.07%. Since inception in April 2018, the fund...

Read more

18 Jul 2024 - Performance Report: Altor AltFi Income Fund

By: FundMonitors.com

[Current Manager Report if available]

18 Jul 2024Interrogating the bull case for housingChallenger Investment Management

Over the past few months, we've been puzzled by the strength of the bullish tone around house prices. Puzzled because the argument supporting house...

Read more

18 Jul 2024 - Interrogating the bull case for housing

By: Challenger Investment Management

Interrogating the bull case for housing

Challenger Investment Management

June 2024

Over the past few months, we've been puzzled by the strength of the bullish tone around house prices. Puzzled because the argument supporting house prices seems to be hanging on the lack of supply/strong migration creating a supply demand imbalance.

Most other factors seem to be flashing warning signals. Consider:

House price valuations relative to incomes are at record high levels in Australia, around 11 times and higher even than Canada and Sweden according to Morgan Stanley;

Negative sentiment with Westpac survey data indicating that less than 10% believe real estate is the wisest place for their savings down from close to 30% in the mid 2010s;

Rental yields relative to cash rates are negative despite strong rental inflation;

Increasing mortgage arrears rates (albeit from a low starting point);

Share of housing finance extended to investors is at the highest share since 2017;

Tighter credit standards; less interest only, increased serviceability buffer combining with higher interest rates. Barrenjoey estimates that from 2017 maximum borrowing capacity from CBA has declined by 30-40%; and

Over 20% of borrowers with loan servicing ratios more than 30%, up from 5% of borrowers back in April 2022.

With all these negative indicators we are heavily reliant on the housing supply/demand argument holding up house price valuations. So how confident are we in the supply/demand imbalance?

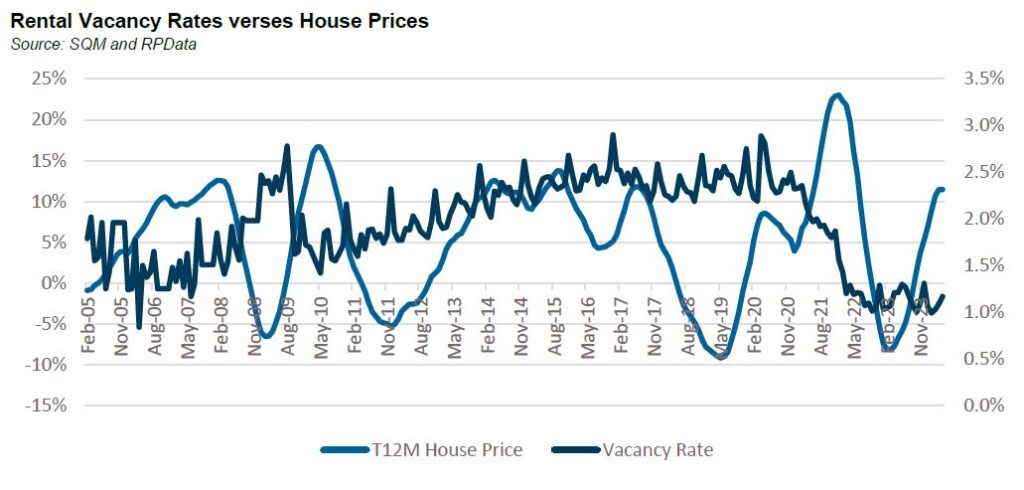

The first indicator for low supply seems to be the lack of vacant rental housing. Pre-COVID vacancy rates were around 2.5%, close to 20 year peaks. When COVID hit, vacancy rates spiked then declined sharply as household formation rates plummeted.

However, the relationship between vacancy rates and house prices does not appear to be as strong as the headlines suggest[1]. Coming out of the GFC, house prices rose strongly even as vacancy rates increased. For much of the 2010s vacancy rates were rangebound between 2-3% but in the second half of the decade prices began to decline. In fact, the last time vacancy rates were this low, it was prior to the GFC.

When a vacancy rate of 1% is quoted, it's calculated as a percentage of total rental stock, not total housing stock. Total housing stock is c. 11 million units compared to rental stock of 3 million. To put in context the decline in the vacancy rate from March 2020 to current is equivalent a reduction of around 30,000 dwellings.

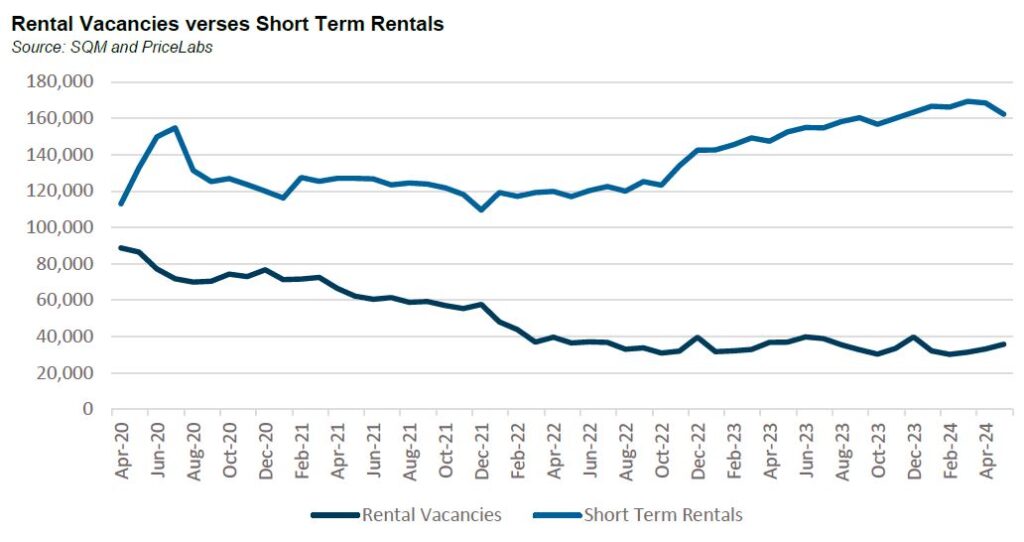

Contrast this figure with the amount of unoccupied houses which was over 1 million on the night of the 2021 census of which 10,000 dwellings were completely vacant, 100,000 were secondary dwellings with the remaining 890,000 being primary dwellings which were empty. Historically there has always been around 10% of total housing stock that is unoccupied at any point in time.

Related to this are short term rentals. These do not show up in the rental vacancy statistics mentioned above but according to PriceLabs, a site which tracks short term rentals, listings are up by close to 50,000 since the start of COVID. It's not unreasonable to assume that some of the rental stock taken out of the market has moved into the short term rental market.

The question is, could it come back?

Having rebounded strongly post COVID RevPAR[2] is down slightly on a year over year basis. With interest rates higher, the economics of short term rentals (and for that matter, long term rentals) is under pressure. Add to this, increases in land taxes for investors in Victoria plus an upcoming levy of 7.5% to be charged for short term rentals which is to be charged from 2025.

It's not inconceivable that as financial conditions tighten, supply could come out of existing stock, either via second houses or short term rentals.

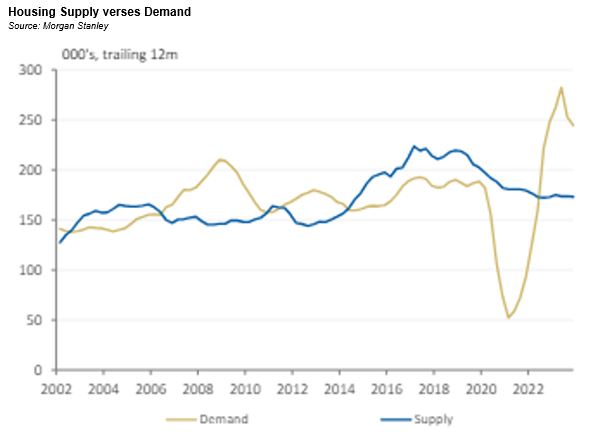

On the supply side, it is clear that the government's target of building 1.2 million homes in 5 years is not happening. The National Housing Supply and Affordability Council estimated in May that around 903,000 dwellings would be built with a further 40,000 social and affordable dwellings built, figures that appear to be far more achievable. But they also expect demand to stabilise with around 871,000 new households forming as migration normalises. So, looking forward we don't seem to have a major housing supply issue.

The question is whether we are grossly under supplied now. The below chart from Morgan Stanley attempts to answer this. It shows that we were undersupplying during the GFC and early 2010s and oversupplying from around 2015 until 2022 from which point the housing market became historically undersupplied. In fact, it is arguable that we are undersupplied right now; our view is that the market is extrapolating incremental demand exceeding incremental supply into a more significant and permanent imbalance than likely exists[3].

So, what does this all mean?

We think the supply-demand argument is overbaked. The state of the housing market has much more to do with the amount of stimulus and lagged effect of interest rate increases than migration and construction. As the economy goes so too does the housing market.

Already house prices in New Zealand and the United Kingdom, two markets with very tight supply demand characteristics, are declining. House prices in Canada are flat and slowing in the United States. House prices have had a strong run in Australia, but we expect some normalisation over the second half of 2024.

[1] Academic research has shown there is a relationship between rental vacancy rates and rents and then a relationship between rents and house prices. Our view is simply that there are much more important factors at play driving house prices such as real incomes, interest rates, sentiment and asset prices.

[2] RevPAR refers to Revenue Per Available Room. It is a standard acronym within the hotel sector and is used within the short term rental market.

[3] We haven't discussed migration in this piece and instead relied on the NHSAC estimates for new household formation. Suffice to say migration is a highly politicised issue and risks are likely to the downside given the rhetoric from both sides of the aisle.

17 Jul 2024Performance Report: Skerryvore Global Emerging...FundMonitors.com

The Skerryvore Global Emerging Markets All-Cap Equity Fund returned -0.36% in June. Since inception in August 2021, the fund has returned +3.88% per...

Read more

17 Jul 2024 - Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

By: FundMonitors.com

[Current Manager Report if available]

17 Jul 2024Performance Report: Quay Global Real Estate Fund...FundMonitors.com

The Quay Global Real Estate Fund (Unhedged) returned -0.75% in June. Since inception in January 2016, the fund has returned +6.47% per annum, an...

Read more

17 Jul 2024 - Performance Report: Quay Global Real Estate Fund (Unhedged)

By: FundMonitors.com

[Current Manager Report if available]

17 Jul 2024Research in Focus: Fast food companies down, but...Janus Henderson Investors

Portfolio Manager and Research Analyst Joshua Cummings, from the Global Research Team, says that while inflation-weary consumers are pushing back...

Read more

17 Jul 2024 - Research in Focus: Fast food companies down, but not out

By: Janus Henderson Investors

Research in Focus: Fast food companies down, but not out

Janus Henderson Investors

July 2024

Portfolio Manager and Research Analyst Joshua Cummings, from the Global Research Team, says that while inflation-weary consumers are pushing back against the price of fast food today, the industry's long-term prospects still appear strong.

In a time of elevated inflation, anyone might reasonably think the fast-food industry would thrive as consumers seek out low-cost dining options. But judging by recent headlines and viral social media posts, these days, even fast food is getting pushback from cash-strapped consumers. "Americans are choking on surging fast-food prices," said one news report in May. "$18 Big Mac meals," exclaimed another headline, followed by social media posts purporting the famous hamburger deal now costs 100% more than it did five years ago.

The furor became so deafening that in late May, Joe Erlinger, president of McDonald's USA, felt compelled to write a "Myth vs. Facts" blog post, defending the fast food chain's price increases. (Fact: the average Big Mac Meal is now $9.29, up only 27% from 2019.1)

Even so, the damage has been done: During the latest quarterly reporting period, many fast-food chains reported a decline in year-over-year same-store sales growth. Their stocks have also lagged the broader equity market in 2024. And to win back customers, many companies are rolling out new value deals and adopting a "street-fighting mentality to win."

Investor takeaway

In our view, the fast-food saga signals that more households are beginning to feel the cumulative impact of nearly three years of above-average inflation. Whether $5 value deals and other promotions will be enough to win them back in the short term remains to be seen.

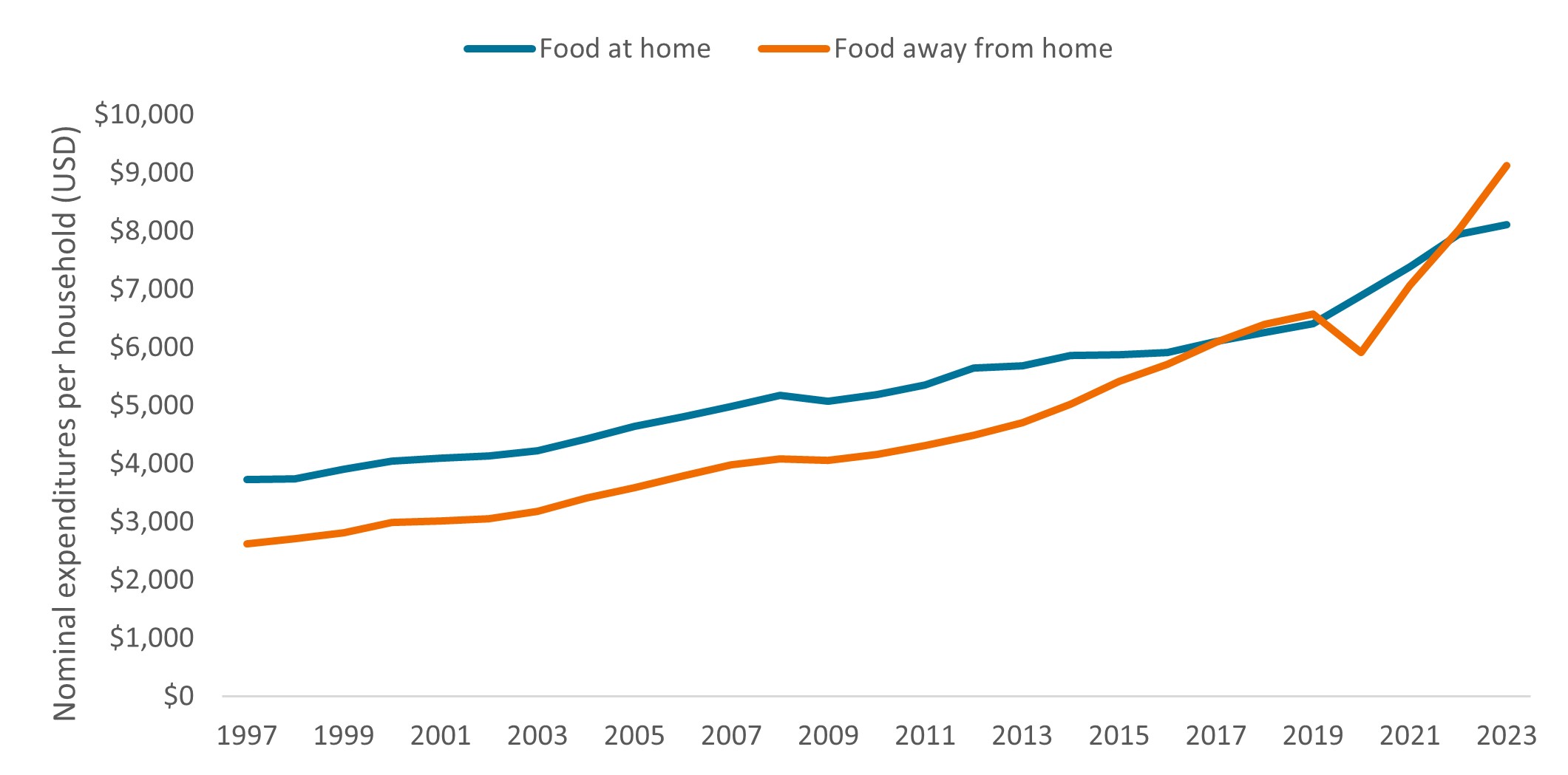

But we'd encourage investors to also consider longer-term trends and remember that business fundamentals - not headlines - tend to matter more to companies' long-term prospects. Over the last few months, the annual rate of inflation in the U.S. for food away from home (FAFH) has exceeded that of food at home (FAH), but since the pandemic, price increases in the two categories have largely kept pace (albeit with exceptions in some regions due to factors such as local minimum wage laws).2 And eating out has always been more expensive than FAH regardless of the inflation backdrop.

Furthermore, data show that when looking at long-term patterns, consumers are increasingly choosing to dine out. The average household spent more on FAFH as a portion of their overall food budget for the first time starting in 2018. And that percentage - with the exception of 2020, during pandemic lockdowns - has continued to climb since (See "By the numbers"). To that end, while growth has recently slowed for some companies, sales are still well above where they were before the pandemic, allowing firms to boast double-digit operating margins.

Will inflation reverse this trend? In a recent survey, nearly 80% of Americans said fast food is now a luxury because of price increases. But three-quarters of respondents also said they eat fast food at least once a week, and nearly half said they use store apps to unlock deals.3 In our view, these data points suggest fast food enterprises that are perceived to offer "value" - whether through loyalty programs, new menu items, quick service, and so on - have room for further growth.

Geography could also come into play: One popular fast-casual restaurant serving up burritos still has 99% of its stores in the U.S. It is among the most popular fast food options with Americans, and while management has plans to nearly double the domestic footprint, they are also eyeing non-U.S. expansion. In our view, that suggests opportunity for significantly more - not less - growth ahead.

By the numbers - U.S. household spending on food at home vs. away from home

Source: Calculated by U.S. Department of Agriculture, Economic Research Service from various sources. As of 3 June 2024.

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

The Bennelong Emerging Companies Fund rose by +1.9% in June, outperforming the ASX 200 Total Return benchmark by +0.89%. Since inception in November...

Read more

16 Jul 2024 - Performance Report: Bennelong Emerging Companies Fund

By: FundMonitors.com

[Current Manager Report if available]

16 Jul 2024Performance Report: ASCF High Yield FundFundMonitors.com

The ASCF High Yield Fund rose by +0.61% in June. Since inception in March 2017, the fund has returned +8.16% per annum, an outperformance of +6.7%...

Read more

16 Jul 2024 - Performance Report: ASCF High Yield Fund

By: FundMonitors.com

[Current Manager Report if available]

16 Jul 2024Why Anchoring is Sabotaging Your Stock Market...Marcus Today

A landscape image representing the stock market and stock market analysis. The background features a digital chart with rising and falling stock...

Read more

16 Jul 2024 - Why Anchoring is Sabotaging Your Stock Market Success

By: Marcus Today

Why Anchoring is Sabotaging Your Stock Market Success

Marcus Today

July 2024

A landscape image representing the stock market and stock market analysis. The background features a digital chart with rising and falling stock prices, candlestick graphs, and financial data overlays. On the side of the image, a large anchor is more apparent and appears submerged into the stock market scene, symbolizing stability amidst the market fluctuations. The overall color scheme includes shades of blue, green, and red to reflect the dynamic nature of the stock market. No ocean or people are present in the image.

Understanding Anchoring and Its Impact on Stock Market Investments

What is Anchoring in Financial Markets?

We all have a lot of trouble buying stocks that have gone up a lot and selling stocks that have gone down a lot. If that's you then I regret to inform you that you are being affected by a well-established financial concept that only affects soft brained investors. It is called "Anchoring". Anchoring, also known as a 'focusing bias', is the use of a reference point against which to judge value.

You hear the issue every day in a broking office, it's when someone says "I can't buy that because the share price is up XYZ%" or "You can't sell that the price is down XYZ%". An even more soft brained development on the theme is when you find yourself saying "It's down XYZ% so it's cheap" or "It's up XYZ% so it's expensive".

But making money in shares is all about where the share price is going. In that equation, where the share price has been is pretty much irrelevant and the fact that we don't buy or sell a stock because it is up X percent or down X percent, because of where the share price 'was', is unscientific. What you paid for a stock, what price it was in the past, in fact, any reference to the share price history, ignores the only relevant consideration which is what the share price is going to do tomorrow. BHP five years ago was priced on a different set of facts to BHP now, so what relevance is that old high or old low. It's irrelevant.

Despite that it is common practice to reference how much a stock has moved from the lowest low or highest high and it is commonplace to take those past prices (laughably - the extreme highs or lows) as an anchor point from which to judge the current price as being expensive or cheap based on how far it is up or down since then.

But past prices are simply a statement of where a price was. The more important consideration is what the company is worth now coupled with an understanding that the market's appreciation of what the company was worth at some point in the past has almost certainly changed. As soon as the value of a company changes, which arguably it does every day, you have to move your thinking along.

If your decision making starts with a reference point from the past (It's up XYZ% from the low") you have proven yourself a bit amateur. To make a stock judgement past prices are the most unscientific of starting points.

Another amateur manifestation of anchoring is buying stocks because they have fallen a lot. This is technically wrong to do (you should sell stocks going down not buy them). Buying bombed-out stocks (catching the knife) because they have fallen a lot, ignores the fact that the market's assessment of the company's value has changed, a lot, for the worse, so the 'attraction' of a big fall is irrelevant.

The other very widespread use of anchoring is when traders use their purchase price as a reference point. "I'll sell it if it goes up 10%" or "I'll sell if it goes below my purchase price". All very nice but not rational, although, in its defence, anything, even unscientific anchoring, is better than nothing when it comes to having some trading discipline.

An extension of anchoring is 'lazy jargon'. Saying that a stock is "cheap" or "undervalued" because it has fallen a lot. Or "expensive" or overvalued" if it's gone up a lot. A stock can only be valued with reference to what it is worth, not with reference to what the share price used to be.

The best way to avoid anchoring is to forget the past price as a reference point and simply assess 'cheap or expensive' on some other criteria. PE history perhaps, or price relative to an intrinsic value calculation would be more useful.

Meanwhile you can amuse yourself by listening out for anyone, you perhaps, making comments or decisions on the basis that a stock is up X% or down X% because your sole focus should be whether a stock is going up or not. The fact that it's gone up or not, that, is irrelevant.

Anchoring - Another reason humans aren't wired to trade successfully.

21 Mar 2024ESG in 10: Episode 15 - The disproportionate...Fidante Partners

In this episode, we delve deep into this crucial topic with Melissa Stewart, a member of the Alphinity Sustainable Share Fund and Alphinity Global...

Read more

21 Mar 2024 - ESG in 10: Episode 15 - The disproportionate impact of modern slavery on women and girls

By: Fidante Partners

ESG in 10: Episode 15 - The disproportionate

impact of modern slavery on women and girls

Fidante Partners

March 2024

According to a Walk Free Report, one in every 130 females globally is living in modern slavery. Women and girls account for nearly three-quarters (71%) of all victims. This stark reality sheds light on the disproportionate impact of modern slavery on women and girls, highlighting the urgent need for action.

In this episode, we delve deep into this crucial topic with Melissa Stewart, a member of the Alphinity Sustainable Share Fund and Alphinity Global Sustainable Equity Fund (Managed Fund) compliance committees.

Tune in as we discuss the impact of gender inequality on modern slavery prevalence and explore how investors can play a pivotal role in addressing this issue.

19 Mar 2024Fund Monitors | Peer GroupsFundMonitors.com

If you are interested in how a particular fund has performed compared to its competitors or how different sectors have performed against each other,...

Read more

19 Mar 2024 - Fund Monitors | Peer Groups

By: FundMonitors.com

Peer Groups

FundMonitors.com

If you are interested in how a particular fund has performed compared to its competitors or how different sectors have performed against each other, you can use FundMonitors.com to access and compare peer groups.

7 Mar 2024Fund Monitors | Custom StatisticsFundMonitors.com

Custom statistics allows you to designate the information you want to see and compare funds, indices and even your own portfolios. It generates a...

Read more

7 Mar 2024 - Fund Monitors | Custom Statistics

By: FundMonitors.com

Custom Statistics

FundMonitors.com

Custom statistics allows you to designate the information you want to see and compare funds, indices and even your own portfolios. It generates a simple comparison report that is updated to the last available date each time you access a report.

13 Feb 2024Fund Monitors | Watch ListFundMonitors.com

Using a watchlist gives you access to the most up to date information on the funds that you're most interested in. By adding funds to your watchlist...

Read more

13 Feb 2024 - Fund Monitors | Watch List

By: FundMonitors.com

Using a Watch List

FundMonitors.com

Using a watchlist gives you access to the most up to date information on the funds that you're most interested in. By adding funds to your watchlist you can access information quickly and easily and compare both recent and longer term performance.

7 Feb 2024Fund Monitors | Fund Selector ToolFundMonitors.com

FundMonitor.com's Fund Selector also allows you to filter your search by individual criteria. You can filter by strategy, fund structure, fund size,...

Read more

7 Feb 2024 - Fund Monitors | Fund Selector Tool

By: FundMonitors.com

Fund Selector Tool

FundMonitors.com

FundMonitor.com's Fund Selector also allows you to filter your search by individual criteria. You can filter by strategy, fund structure, fund size, and a range of other metrics.

6 Feb 2024Magellan Global Quarterly UpdateMagellan Asset Management

Arvid Streimann discusses investment attributes that led the market in 2023 and key thematics to watch out for in the year ahead, while Nikki Thomas...

Read more

6 Feb 2024 - Magellan Global Quarterly Update

By: Magellan Asset Management

Magellan Global Quarterly Update

Magellan Asset Management

January 2024

Arvid Streimann discusses investment attributes that led the market in 2023 and key thematics to watch out for in the year ahead, while Nikki Thomas shares her insight on how the portfolio is positioned and the strategy behind investment decisions in the portfolio.

This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.

30 Jan 2024Airlie Quarterly Update - January 2024Airlie Funds Management

Emma Fisher provides her perspective on how the Australian equity market played out in 2023 and the outlook for the year ahead. Emma also discusses...

Read more

30 Jan 2024 - Airlie Quarterly Update - January 2024

By: Airlie Funds Management

Airlie Quarterly Update - January 2024

Airlie Funds Management

January 2024

Emma Fisher provides her perspective on how the Australian equity market played out in 2023 and the outlook for the year ahead. Emma also discusses movements within the portfolio and the approach to position sizing.

Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie.

8 Dec 2023The weight loss drug shaping-up as a gamechangerMagellan Asset Management

The world is awash with news that a drug designed to treat type 2 diabetes has also been approved to help achieve weight loss. Glucagon-like peptide...

Read more

8 Dec 2023 - The weight loss drug shaping-up as a gamechanger

By: Magellan Asset Management

The weight loss drug shaping-up as a gamechanger

Magellan Asset Management

November 2023

The world is awash with news that a drug designed to treat type 2 diabetes has also been approved to help achieve weight loss. Glucagon-like peptide 1 -- or GLP-1 -- is considered by some as a wonder drug and a new weapon in the public health battle against obesity. But what are the wider implications for the investment world? In this episode of Magellan In The Know, Portfolio Manager Nikki Thomas is joined by three Magellan Investment Analysts: Emma Henderson, Wilson Nghe and Tracey Wahlberg. Together they discuss the investment landscape surrounding GLP-1, looking at the pitfalls and potential financial benefits for sectors from healthcare, food retailing and restaurants to fashion, exploring which parts of the consumption landscape could be winners or losers.

This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material.

Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.

1 Dec 2023What is AMR and why is it important for Investors?Fidante Partners

In this episode, Charlotte is joined by Moana Nottage from Alphinity Investment Management to discuss her research into Antimicrobial Resistance...

Read more

1 Dec 2023 - What is AMR and why is it important for Investors?

By: Fidante Partners

ESG in 10: Episode 12 -

What is AMR and why is it important for Investors?

Fidante Partners

November 2023

In this episode, Charlotte is joined by Moana Nottage from Alphinity Investment Management to discuss her research into Antimicrobial Resistance (AMR) and the importance of integrating AMR as a factor into the investment and stewardship process.

When used correctly, antimicrobials play a key role in treating human and animal health. Antibiotics in particular have saved millions of lives since the 1940s and have contributed significantly to the life expectancy we see today. But microorganisms are becoming more resistant to contemporary medicine. Without responsible antimicrobial use, disease prevention and research into alternatives, the systemic risk posed by antimicrobial resistance (AMR) could be extremely disruptive.

2 Nov 2023Airlie Quarterly UpdateAirlie Funds Management

Emma Fisher, Portfolio Manager, chats to Airlie's Analysts Joe Wright and Jack McNally about their recent US trip and findings from their discussions...

Read more

2 Nov 2023 - Airlie Quarterly Update

By: Airlie Funds Management

Airlie Quarterly Update

Airlie Funds Management

October 2023

Emma Fisher, Portfolio Manager, chats to Airlie's Analysts Joe Wright and Jack McNally about their recent US trip and findings from their discussions with companies, Aristocrat, QBE and SANTOS which are holdings in the Airlie Australian Share Fund.

Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon.

Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie.

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.

"I've been subscribing to AFM for over two years and love it. The ability to compare funds, do in-depth research and gain data-driven insights into performance metrics and performance rankings in a highly visual way is second to none. Highly recommended."

~ James Waggett,

Managing Director of Waggett Wealth Advice Ltd